The growth plan

The Government insist that the Chancellor’s statement on Friday 23 September was not actually a Budget but a Growth Plan. Because it was not a Budget, the Office for Budget Responsibility (OBR) was not required to carry out its normal detailed assessments and projections which, considering the market reaction to the announcements in the week or so since, may have been deliberate. The next scheduled Budget will be in Spring 2023, accompanied by a fresh OBR forecast. That makes 2022 a year with three Chancellors but no Budget.

Many of the changes announced were well trailed. Aside from the important and separately announced direct cap on unit price energy costs for individuals and businesses, the Prime Minister (PM) had been very vocal throughout her leadership campaign about her aspiration to reverse the April 2022 National Insurance (NIC) increases and to stop the proposed 2023 Corporation Tax increase.

The NIC increase reversal from 6 November this year, together with a reversal of the 1.25% increase to the rates of dividend taxation, were effectively announced in a Treasury Publication on 22 September, ahead of the Growth Plan.

When the Chancellor delivered his 30 minute statement, it became clear that, for something that was not a Budget, we got some pretty radical (and costly) changes proposed. Arguably, tax changes that are far more material than many that have been announced in previous ‘full Budgets’.

So, what did we get?

6th October 2022

-

Gavin Jones See profile

Gavin Jones See profile

A clearly stated aspiration to reignite growth in the economy at a rate of 2.5% per annum.

The Government had previously announced that there would be a cut in the basic rate of Income Tax, from 20% to 19%, from April 2024. This is now being brought forward to take effect from April 2023. The Government states that this reduction is worth over £5 billion for workers, savers and pensioners and that 31 million taxpayers will benefit in 2023/24, with an average gain of £170.

In an example of the speed of political change, the Government have already U turned on the intention to abolish the 45% additional rate of income tax from April 2023. Not hugely unexpected given the almost universal condemnation of this particular proposal.

There are a number of tax consequences which stem from these changes. One of them is the amount of tax relief given at source on pension contributions and Gift Aid donations. This is currently given at the basic rate of 20%. The Government has stated that there will be a four-year transition period for Gift Aid relief to maintain the Income Tax basic rate relief at 20% until April 2027. This will support almost 70,000 charities and is worth over £300 million. However, there was little comment on pension contributions other than that there will also be a one-year transitional period for Relief at Source pension schemes to permit them to continue to claim tax relief at 20%.

The 1.25% increase in dividend taxation will be reversed from 6 April 2023.

From April 2023:

- the dividend ordinary rate of 8.75% will reduce to 7.5%

- the dividend upper rate of 33.75% will reduce to 32.5% and

- the dividend additional rate of 39.5% will reduce to 38.1%

As the reduction in the dividend rates of tax do not take effect until 6 April 2023, there is time to plan ahead. Director/shareholders may want to consider delaying any further extraction of retained profits as dividends until the 2023/24 tax year. This will enable advantage to be taken of the lower rates of dividend tax that will apply from 6 April 2023.

In September 2021, the Government published its proposals for new investment in health and social care in England.

The Health and Social Care Levy Act provided for a temporary 1.25% increase to both the main and additional rates of most classes of National Insurance Contributions (NICs) for 2022/23. From April 2023 onwards, the NIC rates were intended to revert back to 2021/22 levels and be replaced by a new 1.25% Health and Social Care Levy.

However, the new Chancellor has decided to:

reverse the temporary increase in NICs from November and

cancel the Health and Social Care Levy completely.

The Chancellor has confirmed that funding will be maintained at the same level as if the Levy was in place, funded from general taxation.

According to the Government, not proceeding with the Levy will reduce tax for 920,000 businesses by nearly £10,000 on average next year.

In addition, it will help almost 28 million people across the UK save £330 on average in 2023/24, with an additional saving of around £135 on average this year.

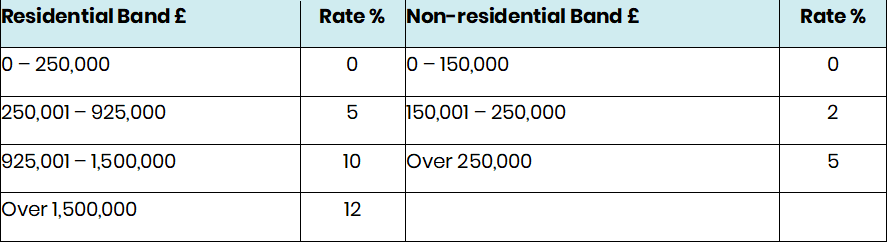

A number of changes are made to the Stamp Duty Land Tax (SDLT) regime. Generally, the changes increase the amount that a purchaser can pay for residential property before they become liable for SDLT.

The residential nil rate tax threshold is increased from £125,000 to £250,000.

The nil rate threshold for First Time Buyers’ Relief is increased from £300,000 to £425,000.

The changes apply to transactions with effective dates on and after 23 September 2022 in England and Northern Ireland. These changes do not apply to Scotland or Wales which operate their own land transactions taxes.

There are no changes in relation to purchases of non-residential property.

Residential rates may be increased by 3% where further residential properties are acquired in addition to the principal residence.

There have been no announcements in relation to trusts. However, the income tax changes announced and coming into force from 6 April 2023 will have a positive impact on trusts, although to a lessor degree now that the additional rate cut has been withdrawn. Full details of the changes to income tax are covered in “Income Tax”.

For trustees, the following are the key points:

Basic rate of Income Tax cut from 20% to 19%

This is the rate currently paid by trustees on income other than dividend income within the standard rate band as well as the maximum rate paid on such income by trustees of interest in possession trusts (where the income is received by the trustees before being passed to the income beneficiary).

Reversing the 1.25% increase to the rate of Income Tax on dividends which took effect on 6 April 2022

Last April, the dividend trust rate went up from 38.1% to 39.35%. The basic dividend rate paid by trustees of interest in possession trusts receiving dividend income went up from 7.5% to 8.75%. From next April these increases are to be reversed.

The planned increases to Corporation Tax scrapped with the single rate staying at 19%. The Bank surcharge, which is an additional amount in excess of corporation tax charged to banks remains at 8%.

A brief summary of some of the additional parts of the plan are included on our website Mini-Budget – The detail and what it means for you – Old Mill (om.uk)

Perhaps lost in the political turmoil has been a number of announcements to promote growth in the economy including:

- Continuing the Annual Investment Allowance and making the current £1m cap permanent.

- Designating up to 40 new Investment Zones around the country with material commercial and tax benefits to encourage regional investment.

The Prime Minister and the Chancellor appear committed to continuing to reduce taxes through this Parliament, primarily to kick start growth, although the prospects of this seem reduced after the u turns this week.

Two weeks on from the growth plan announcement, it stands as a case study in what not to do when changing economic course. With the Chancellor and the Bank of England forced to produce don’t-panic statements on the first working day after his ‘fiscal event’, a u turn on the 45% tax rate cut and the bringing forward of economic forecasts to stabilise the pound and investment markets, this does not instil a great deal of confidence in the Governments fiscal and monetary policies.

The new Prime Minister’s speech at the Conservative conference this week continued with her ‘Getting Britain Moving’ agenda but she is likely to face an uphill battle and the future of her growth plan is far from certain.

The conference itself was notable for division on topics such as future benefit increases and environmental protection.