2024 – Performance of the Old Mill Portfolios

15th January 2025

-

Gavin Jones See profile

Gavin Jones See profile

Performance over the last year (up to Tuesday 31 December 2024)

Over the year, despite the pullback in December, we are pleased to report that all portfolios are higher. For those prepared to take on more investment risk the rewards have been a double digit increase in the last twelve months but for those more cautious there has also been a good return, ahead of inflation. This return was driven by the growth part of the portfolio, with the prospect of falling interest rates and the pro-business policies of Donald Trump driving growth in the second half of the year.

The final quarter was positive for most portfolios but the US Federal reserve signalling that US interest rates may fall more slowly than previously forecast, saw global stockmarkets fall and fixed interest yields rise in December.

Longer term performance over the last 10 years (up to Tuesday 31 December 2024)

The ten-year returns illustrate the value of investing over the longer term. It also highlights that in pursuing higher returns, there will be periods of volatility that call for patience and trust in the investment process. Nowhere did we see this more than in the early days of the covid pandemic in spring 2020 as the chart above aptly illustrates.

Performance over the last year (up to Tuesday 31 December 2024)

Performance over the last year for values portfolios has been slightly higher when compared to the original portfolios as the ESG screened global equity fund has shown strong performance.

Longer term performance over 10 years (up to Tuesday 31 December 2024)

The values portfolios have only been available to our investors for the last five years, but the graph below shows the longer time frame of ten years showing the potential upside over longer periods.

Longer term performance of the values portfolios shows robust growth. The last ten years has seen strong performance from growth assets, especially US equities, even taking into account the Covid pandemic five years ago and the return of inflation after the invasion of Ukraine by Russia at the beginning of 2022.

The table below shows the performance of a number of asset classes in 2024 and the annualised return over the last five years as at close of play on Tuesday 31 December.

The picture overall for growth assets has been strong with the one year return showing good performance across equities and a positive picture over five years, especially international equities.

Bonds in the news

Defensive assets have been more mixed as the impact of inflation is less positive for these assets. Gilts have been in the news over the last few weeks as yields have been rising to levels not seen since before the Great Financial Crisis in 2008.

This will be down to a number of factors but the media has been concentrating on the rising cost of borrowing for the government, citing changes in the budget last year where higher levels of borrowing were made possible by a change in budget rules.

While this will be one of the reasons – borrowing costs has been rising for much of the developed market economies as the economic policies of Donald Trump, once he is inaugurated as US president are expected to be inflationary which will mean higher interest rates. In the UK higher interest rates and a weaker pound may be inflationary and with the government having higher borrowing costs there are fears of cuts to public spending and further tax increases.

Growth assets may avoid some of these impacts as we do not hedge currency exposure, so the value of overseas assets will rise as the pound weakens. And UK companies will benefit from this as their overseas earnings will be higher in Sterling terms.

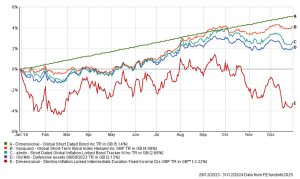

Most of your defensive assets are invested on a global short dated, high quality basis. Their short-dated nature, i.e. the amount of time until the bond matures and capital is repaid, leads to lower interest rate sensitivity than longer-dated bonds, especially when the expectation of interest rates and bond yields are higher. We also avoid a concentrated exposure to any one countries bonds by diversifying across a number of developed market countries. Yields on these bonds are just under 5%.

We do have exposure to inflation linked bonds – short dated global bonds, but with a higher duration for UK Index Linked Gilts. The chart below shows the capital values of the longer dated assets have been falling as inflation expectation rises but the overall contribution for defensive assets, despite this negative return on the Dimensional Inflation Linked fund, has been positive over the year.

Defensive assets performance over the last year (up to Tuesday 31 December 2024)

The investment committee will monitor these assets closely but we do not currently think any changes are necessary.