An unsettling time

It is well known that the financial markets do not like uncertainty and unfortunately in 2022, there has been much to trouble the financial world not least the continuing war in Ukraine and the rapid emergence of a cost of living crisis with British households facing severe pressure from rising costs. Inflation as measured by the Consumer Prices Index is now standing at a level unseen since February 1982.

In a real ‘annus horribilis’ the market reaction to the new Chancellors growth plan has only added to this overall concern with the pound reaching record low levels against the dollar. Last week, we also had an intervention by the Bank of England to purportedly support Government Gilts.

In light of all this, it has been a challenging time for investors and whilst we know investments can go down as well as up, this will be of little comfort when markets are volatile. As we have said on many previous occasions, risk is part and parcel of the investment experience for it is this risk that ultimately drives the prospect of higher returns over time.

6th October 2022

-

Gavin Jones See profile

Gavin Jones See profile

Since the end of last year in the face of higher inflation and interest rates, bond yields have risen and this has caused bond prices to fall. A bond’s yield is calculated using the bond’s current market price compared to the fixed interest rate it pays. For example, a bond that pays a fixed interest rate of 3p and has a price of £1 has a yield of 3%.

In the last few years, yields on bonds generally have been at historic lows and consequently the yields we were achieving from bonds held in the defensive part of portfolios was meagre. In September 2020 as we emerged from the first COVID lockdown, the Bank of England base interest rate was 0.1% and the UK Ten-Year Gilt had a yield at the same level. Today the Bank of England’s base rate has risen to 2.25%, but in anticipation of rising interest rates, the Ten-Year Gilt yield reached 4.5% last week before falling back to just over 4% at the time of writing.

By historic standards, these yields are not extraordinary. In the late 1970’s, the base rate reached 17% and gilt yields were at similar levels. Today however, the world is a different place with economies and individuals having adapted to a long period of low interest rates.

We have seen the implications of the volatility in the gilt market in the mortgage market as lenders were forced to withdraw many fixed rate mortgages from sale as it is difficult for them to know what level to set them at.

All in the price

It is expected that interest rates will continue to rise through this year and the beginning of next and we are asked why we remain in bonds if we know this is going to happen. As the gilt (and overseas bond markets) anticipate the path of future interest rate rises, the current forecast of future interest rates will already be ‘in the price’ of bonds. If expectations stay the same there should not be further falls in price and if expectations get better then there could be capital appreciation as well as much higher expected oncome returns.

As we wrote earlier in the year, rapidly increasing inflation and interest rates present particular challenges for the assets making up the defensive element of investment portfolios.

It has always been Old Mill’s investment philosophy to hold bonds for their defensive characteristics as insurance against the stock market falls we see from time to time. Retaining the lower risk characteristics of our bond investments is a cornerstone of our investment philosophy and without this, there is a risk that portfolios become more volatile creating a very different investment experience. We prefer our low risk investments to be just that and therefore we take more risk with equities where there are the prospects of greater returns.

Investments are not just in the UK

In our bond fund employed in the defensive assets of portfolios, the bonds you hold are short-dated, high-quality bonds in a number of major markets such as the US, UK and Europe. The press coverage of bonds has been focused on the UK, but the majority of your bond exposure will be held internationally to diversify against the risk of being overly exposed to the UK. The expected return for this fund is now in the region of 4% per annum so has risen dramatically over the last year, as markets reflect the risks of higher-for-longer inflation.

There is a short-term cost of transitioning to these higher yields that have led to the capital losses seen in portfolios. For a longer-term investor this should be seen as a price worth paying for higher future returns.

It is also worth noting that the yield rise impact has been materially less severe in high quality, shorter-dated bonds that form the majority of exposure in our defensive assets than for longer-dated and lower quality bonds. The Old Mill Investment Committee has always avoided the temptation to chase the higher yields that have been available from longer dated and poorer quality bonds to avoid taking excessive risks. As recent events have shown, this sensible strategy has been vindicated.

The future

The future direction for bond yields which are inextricably linked to interest rates remains uncertain. Remember that if there was any certainty in which direction yields should move, they would already have moved! If they do rise again, owners of bonds could see some additional falls in value, but they will end up in a better place with yet higher expected future yields. Patience and a long-term view are required.

Away from this short-term negative sentiment belies some relatively positive news that has not been so widely reported on.

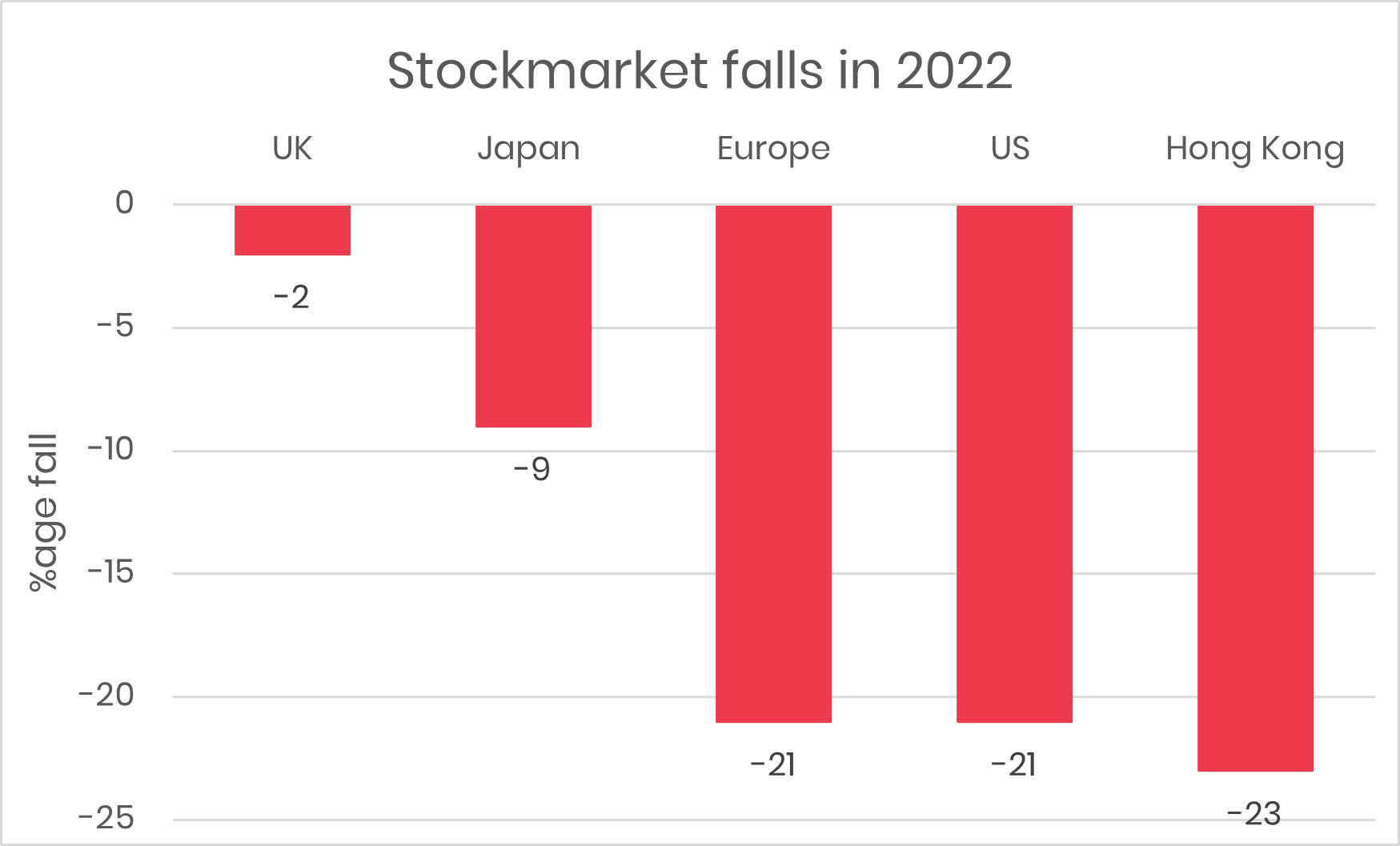

Global stock markets have been volatile this year with major falls in many overseas markets as shown in the chart below.

While the fall in Europe is easier to understand with conflict in Ukraine and Gas supply issues there have also been significant falls in the US and Hong Kong (as a proxy for China).

US Dollar Strength

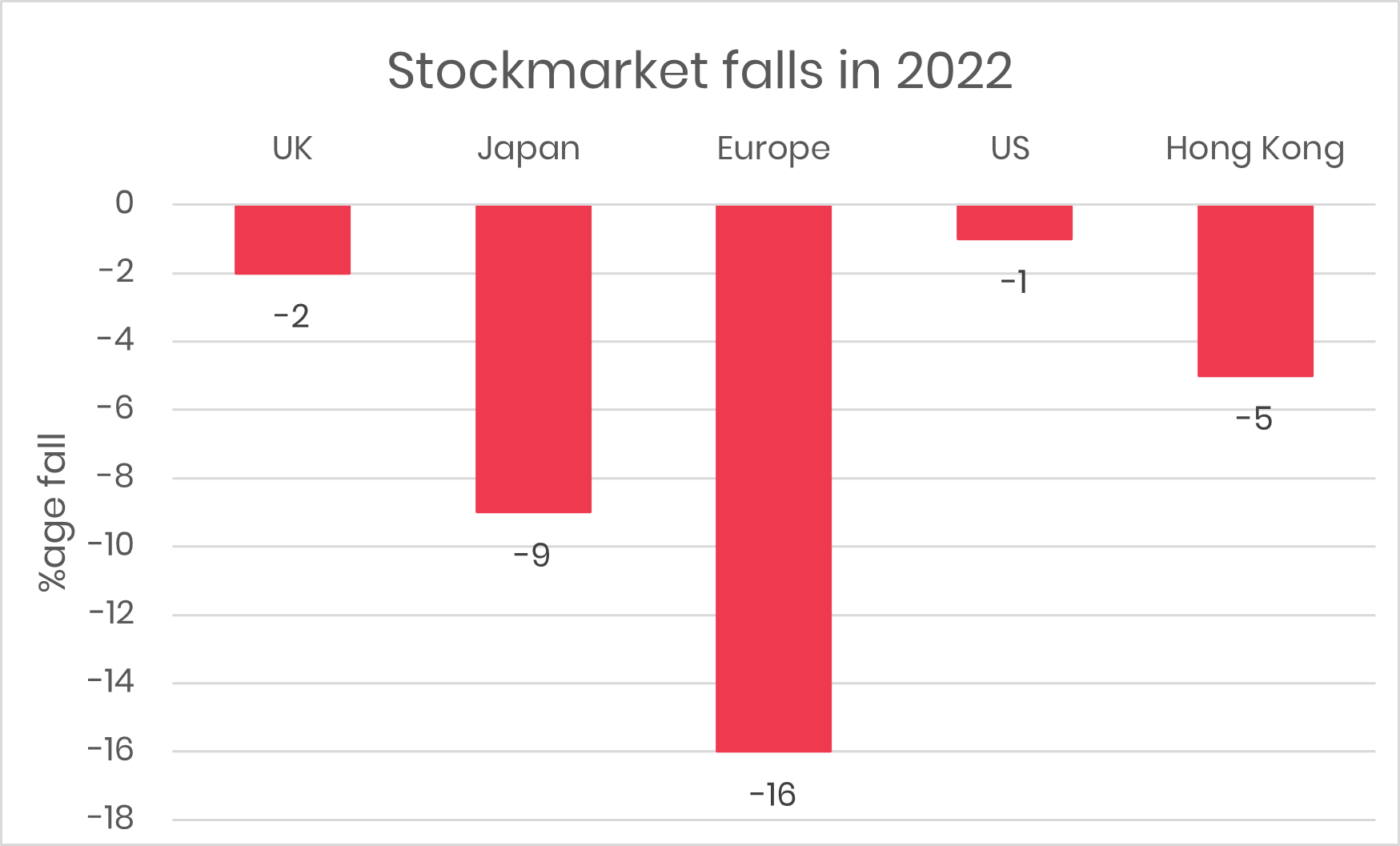

The chart above reflects falls in local currency, but it is important to take account of the positive impact on share values from the weakening of sterling along with many other global currencies over the course of the year as the US Dollar has strengthened.

To give an indication of the impact of this, the bar chart below shows the returns since the beginning of the year in sterling terms. For example, the return in dollar terms for the US stock market of -21% becomes -1% for a UK investor due to the strength of the dollar this year. Our portfolio equity investments have benefitted from the weakness in sterling.

Although there have been sharp falls in stock markets around the world, the growth part of your portfolio has fared reasonably well in relative terms.

Building a robust investment portfolio and having the discipline to stick with it requires fortitude and confidence in the evidence that underpins it.

We structure portfolios with a long-term view in mind. We accept that the relationship between risk and return usually holds true. We also accept that markets are hard to beat, and that most investors aiming to pick tomorrow’s winners fail to do so. We are guided by the evidence to put in place a solution that strikes a balance between the expected upside whilst limiting the expected downside.

The future returns of markets, performance of economies and release of new information are all phenomena outside of our (and anyone else’s) control, though with sensible diversification we can mitigate the impacts of unanticipated downturns.

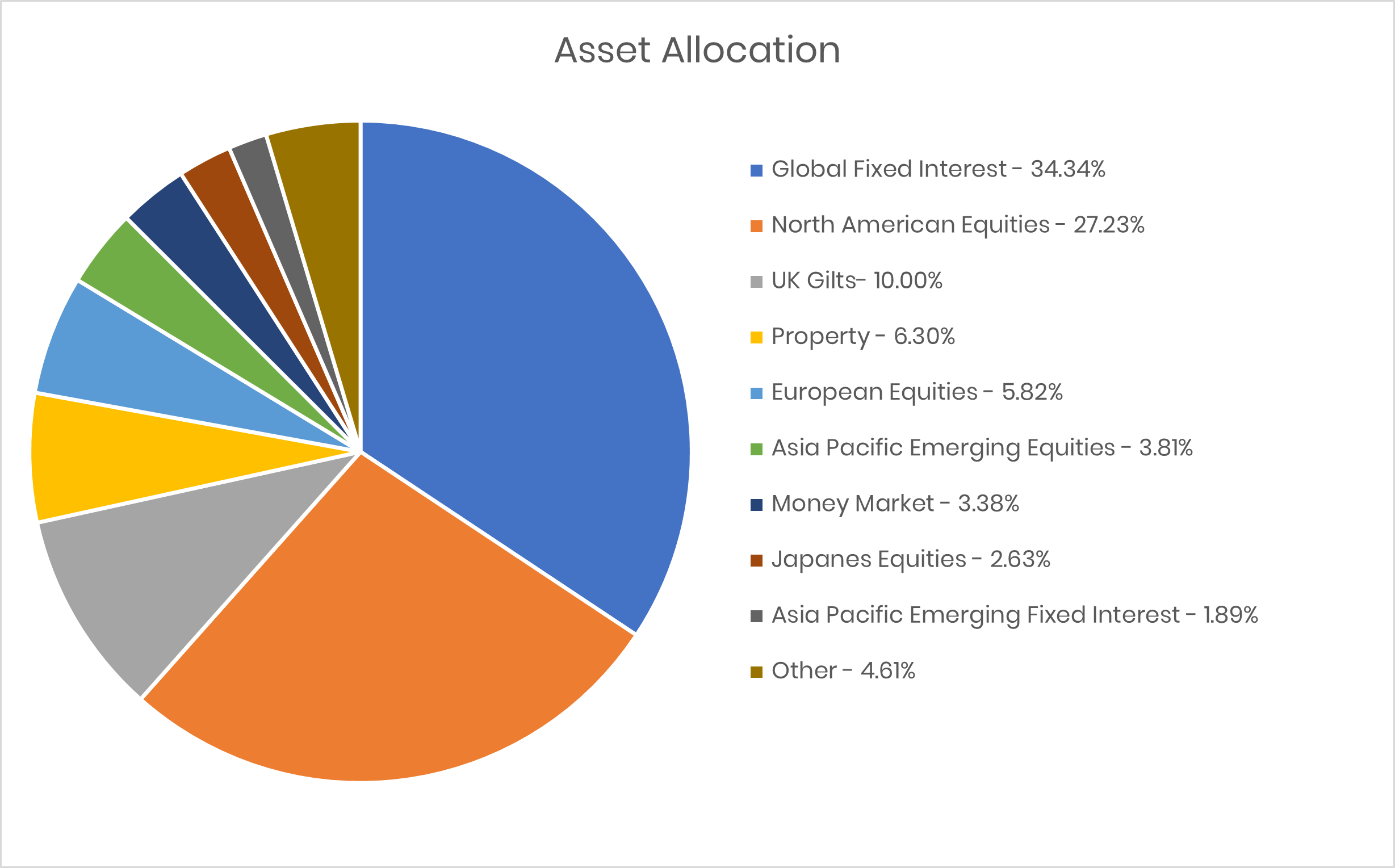

Diversification features comprehensively throughout your portfolio. Your portfolio benefits from the exposure to thousands of stocks, across tens of countries and a wide array of sectors. We also ‘tilt’ to smaller and value (cheaper) companies. Decades of evidence supports the view that a sensible exposure to these ‘risk factors’ rewards investors in the form of higher returns. An incidental – and positive – result is a further increase in diversification.

Diversification in a medium risk portfolio