Autumn Budget 2024 – Pensions

8th November 2024

-

Gavin Jones See profile

Gavin Jones See profile

On retirement 20 years ago, most people with personal pensions chose to secure their income by purchasing an annuity thereby swapping their pension fund for a guaranteed income for the rest of their life. This was in part due to the penal taxes applied at the time to residual pension funds on death with a tax rate of up to 55%. In 2014, the pension world changed when George Osborne announced pension freedoms and the removal of the need to purchase an annuity for many from April 2015.

This move by the then Coalition Government was significant as the link between pensions and providing retirement income was lost, or at least loosened significantly. The Treasury used to have a phrase that the sole or primary purpose of pensions was to provide an income in retirement and tax relief was given to incentivise these savings. In 2015, Steve Webb, the then Pensions Minister stated that HMRC would look unfavourably on anyone using pensions for Inheritance Tax (IHT) planning. In the years since however, it became attractive to save into a pension with the benefit of tax relief and to take advantage of the rules that allowed for any unused funds to be passed down to beneficiaries with no IHT. This has led many people to leave pension funds untouched and instead spend other (taxable) assets first.

This was all turned on its head last week with the announcement that from April 2027, pension funds will be included in estates for Inheritance Tax purposes.

Consultation

Alongside the budget documents, a government consultation was launched explaining how the changes proposed would ensure that tax reliefs on pensions are being used for their intended primary purpose – to encourage saving for retirement and later life.

Until the legislation is published, we cannot be certain how the final rules will look and until then the current rules will continue to apply. It is difficult to give specific advice at this early stage but below we have given more detail in simple terms of what we believe will be the tax treatment of your pension fund on death post-April 2027. We will be able to give specific advice for your individual circumstances once the final details are known.

IHT

IHT will be payable on the value of your pension fund immediately before death. The IHT charge will need to be calculated by the pension scheme administrators and held back before funds are distributed or designated to beneficiaries. The scheme administrators will pay any IHT due directly to HMRC.

The process will require the personal representatives and the pension scheme administrator/trustee having to work together to establish the IHT charge and the proportion of the charge the pension scheme must pay.

As an example, consider an estate of £2 million which includes a pension fund of £1 million for an individual with no spouse and no children. They have an IHT nil rate band of £325,000 which will be shared equally between the free estate and the pension fund. The personal representatives contact the pension scheme administrators and agree that the IHT nil rate band will be split equally between the free estate and the pension fund.

The pension administrators ignore the half share of the nil rate band (£162,500) and apply 40% IHT to the remainder. £1 million – £162,500 = £837,500 x 40% = £335,000 IHT for the pension scheme to pay to HMRC.

This leaves £665,000 in the pension fund to be distributed according to the deceased’s wishes.

Spousal Exemption

Spousal exemption will work in the normal way so if your spouse or civil partner is nominated for the entire pension benefit, there should not be an IHT charge on the first death at least.

In the example above, if there was a surviving spouse or civil partner there would be no charge to IHT.

Existing pension tax charges

Although pension funds currently are not subject to Inheritance Tax, they can be subject to other pension charges which we believe may continue to apply post-April 2027 in addition to any IHT charge.

At the present time, we understand IHT will be calculated and charged before any existing tax charges are applied. Broadly this means there will be a difference depending on whether you die before or after age 75 and who your death benefit goes to. Put simply, unless your pension is nominated to your spouse, the fund available to be distributed could be reduced by up to 40%.

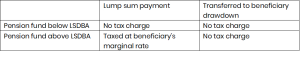

If you die before your 75th birthday

Existing tax charges will continue to apply so there could be additional tax due for those below 75 who elect to take a lump sum death benefit above the Lump Sum and Death Benefits Allowance (LSDBA). The standard LSDBA is £1,073,100 but higher figures may be possible if pension protection is in place. There should be no additional tax charges where benefits are taken in the form of a beneficiary’s drawdown plan.

The table below isn’t exhaustive but covers the tax charge for most scenarios.

After your 75th birthday

For deaths occurring after age 75, where benefits are transferred to a beneficiary drawdown plan, any funds subsequently withdrawn will suffer Income Tax in the hands of the beneficiary at their own marginal rate of Income Tax. Where a lump sum payment is made there is a marginal rate tax charge on the recipient – so up to 45%, which including the IHT can mean a total tax charge of up to 67%.

What next?

There has been much talk in the media of the unfairness of ‘double’ taxation of IHT and possible pension charges on top for those with large funds above the LSDBA who die before 75 and for those who die after 75.

Until final details are known, we are not able to provide specific advice. While the current rules remain in place until April 2027, you may not want to disturb your current arrangements for dealing with your pension fund on death. For those who are likely to draw on their funds significantly to support their retirement income requirements, these changes are likely to have less impact. For those who do not require their pension funds to generate their income, these changes are potentially very significant and how this can be managed will require very careful consideration once the rules have been published. In all cases, the implications of this change will need to be factored into your planning.

Starting to draw upon your pension

If you are over the age of 55 (rising to 57 from April 2028) you can start drawing on your pension fund, with a tax-free lump sum of usually 25% of the fund value (within limits) and any income received is simply taxed at your marginal rate of Income Tax.

For anyone who is a non-taxpayer or pays tax at the basic rate and, especially those over the age of 75, it may now be beneficial to start drawing income ahead of the changes in April 2027 provided it remains taxable still at the basic rate. This income could potentially be free of IHT if gifted whereas leaving the funds to accumulate in the pension could mean they will become taxable if the estate is liable to IHT.

If you have reached the age of 75 and not yet drawn your tax-free cash sum, then it is likely to be sensible to take this before the changes in 2027. Whilst the lump sum may be liable to IHT at 40% in your estate, it will avoid additionally incurring pension charges as well which would see an overall effective tax rate of 67%. Your financial planner will be able to advise on the merits of doing this in your circumstances.

Gifting

While there were some big changes to IHT, the normal rules of gifting were left unchanged.

- Potentially exempt transfers (PETs): are gifts to individuals to remove money from your estate. PETs allow you to gift an unlimited amount during your lifetime direct to anyone you wish. If you live for 7 years after the gift, it will be outside of your estate for IHT purposes.

- Chargeable lifetime transfers: occur when you are gifting money indirectly to people, via a trust. This may give you greater control over the money but there are lifetime IHT charges that may be due for larger transfers, or if you have already made certain gifts. Again, you will need to live for 7 years for the gift to become fully outside your estate.

- Normal expenditure out of income exemption: allows you to gift income that is surplus to your requirements, and which is potentially outside of your estate immediately. Such regular gifts can be made directly to an individual, or it may be more desirable to make regular contributions indirectly to a beneficiary’s pension, for instance, or even a Trust.

There are certain rules that will need to be followed to ensure a successful claim for gifts to be treated as being regarded as normal expenditure out of income during your lifetime. HMRC states that a gift:

- Formed part of the transferor’s normal expenditure: HMRC will look for evidence that there is a regular pattern to the gift, perhaps by setting up a direct debit.

- Was made from income: The gift cannot be made from capital, or capital assets like jewellery.

- Left the transferor with enough income for them to maintain their normal standard of living: Your personal representatives will have to provide calculations to HMRC of income and expenditure for each tax year considered to determine the surplus income amount. The income amount may not be the figure used for an Income Tax calculation, i.e. income from an Individual Savings Account (ISA) can be included.

Pension nominations

It is likely all pensions and death benefit nominations will need to be reviewed over time but especially for those who have earmarked their pensions for estate planning purposes.

For those with a spouse or civil partner, it is likely to become the default that they are nominated to avoid an IHT charge on the first to die. This will avoid unnecessarily using nil rate bands that may otherwise be used by the survivor on the second death.

Certain situations are going to be more difficult to manage, particularly where pensions have been used to plan for complex families – perhaps where a second spouse is gifted assets, but pension funds are earmarked for children from a first marriage or farming families where one child has been gifted the farm and the pension nominated for other non-farming children by way of compensation.

Death in service schemes

There has been speculation in the press about the taxation of life assurance schemes designed to pay out a multiple of an employee’s salary if they die before retirement. These are often set up within a pension wrapper and currently the benefit payable is not subject to IHT. There is a possibility that such schemes may be included in these changes.

The technical consultation on the changes did state ‘All life policy products purchased with pension funds or alongside them as part of a pension package offered by an employer are not in scope of the changes in this consultation document.’ We hope this means that these schemes will not be taxed but clarification will be needed.

Summary

There has long been an argument for a set of consistent rules for pension schemes as this gives people confidence to plan for the future. While some of the proposed changes are understandable from a tax point of view, the cliff-edge implementation in 2027 will have serious consequences for some who had planned within the existing rules.

The inclusion of pension funds within estates for IHT purposes is potentially very complex and as a consequence, it also seems that the job of personal representatives will get more onerous with the need to deal with pension companies and arrange for them to settle tax liabilities. We have an estate administration service to make this job a little easier for your loved ones on your death and we will be writing about the benefits of this service in a future Insight.

Once we have the final legislation, we will be setting out the steps that people may wish to consider when minimising the impact of the changes on their financial planning.

If you have any questions, or want to discuss your individual circumstances with an Old Mill financial expert, please do get in touch by clicking here…