Autumn Budget 2025 – Budget changes and financial planning

The financial planning process is ongoing and continually needs to be reviewed to not only take account of Budget changes to tax legislation, but more importantly, to ensure plans are adjusted if necessary to take account of any changes in taxation.

4th December 2025

-

Gavin Jones See profile

Gavin Jones See profile

Regular Review

Successive governments have made constant tax adjustments to suit their political and economic agendas, and we all have to deal with the financial implications of this. As was so apparent in the run-up to this year’s Budget, it is impossible to second-guess any future changes or tax rises, which makes it all the more important to maximise the allowances and tax relief available to you now, as they may be changed at future Budgets.

While the Government had been publicly honouring its manifesto promise of not increasing taxes on working people, Income Tax, National Insurance or VAT, Rachel Reeves called an unusual pre-Budget speech, that pointed to a downgrade of growth by the Office for Budget Responsibility (OBR) which was taken as an indication that one or more of these taxes would increase in the face of worse than expected economic forecasts.

We now know the downgrade was not as bad as feared and the Government has been very keen to point out that they have not had to break their Manifesto promise. This raises the interesting question of when is an increase in tax not an increase in tax?

Labour’s 2024 General Election manifesto wording on tax rises was very narrow and specific.

‘Keep taxes on working people as low as possible. We will not increase National Insurance, the basic, higher or additional rates of Income Tax or VAT.’

This wording, however, left scope to make changes to tax thresholds and allowances, which is exactly what we have seen. Whilst technically tax rates may remain unchanged, the amount of tax being paid has definitely not stayed the same. It can also be argued that Income Tax rates are also increasing, albeit in relation to dividends and savings, but these also affect working people. Not wishing to get political, but it would be nice if our politicians were a little more honest with us.

Planning for the future

While the recent changes may not have an immediate impact on you, there are going to be higher taxes in the future, and we have set out some of the implications for you in this Insight.

One of the big topics will be the Inheritance Tax treatment of pensions from April 2027. While pensions have been a major part of passing wealth down to beneficiaries in the last ten years, these rule changes will necessitate a major rethink for some and possibly the need for a different plan. We have written a separate article about this – Pensions Breakdown.

We also know some of our clients will be seriously impacted by the changes to Agricultural and Business Property Relief (APR and BPR), which take effect from April 2026. Specialist advice is recommended if you are in this position, and we have included links to articles looking at this from our colleagues in our Rural and Small Business teams here Inheritance Tax Breakdown.

Keeping more of your wealth

Reducing tax liabilities is a key financial planning objective. Many of you will have investments wrapped in pensions and Individual Savings Accounts (ISAs) where gains can be made and income earned without giving rise to a tax charge.

As well as the continued freezing of tax thresholds, this Budget introduced changes to the basic and higher rates of Income Tax on dividend income from 6 April 2026 by 2% to 10.75% and 35.75% respectively; and the basic, higher and additional rates of Income Tax on savings income increasing on 6 April 2027 to 22%, 42% and 47% respectively.

There will be no change in the dividend additional rate, which will remain at 39.35%.

People who wish to invest should aim to use their dividend and personal savings allowances in full. Spouses/civil partners should also try to arrange their investment holdings in such a way to ensure they fully use both personal allowances, personal savings allowances, dividend allowances and starting/basic rate tax bands.

Individuals should continue to maximise contributions to ISAs, particularly where dividends from investments are likely to exceed the dividend tax allowance and/or the higher rate tax threshold.

Maximising ISA allowances

Cash ISA allowance reduced from 2027

With effect from 6 April 2027, the maximum amount that can be invested in a Cash ISA per individual will be reduced to £12,000 (within the overall annual ISA limit of £20,000) unless the individual is aged over 65 in the tax year of subscription. For over 65s, the annual subscription limit for Cash ISAs will remain at £20,000.

The annual subscription limits will remain at £20,000 for Stocks and Shares ISAs, £4,000 for Lifetime ISAs and £9,000 for Junior ISAs and Child Trust Funds. These allowances are frozen until 5th April 2031.

The Government is set to publish a consultation in early 2026 on the implementation of a new, simpler ISA product to support first-time buyers to buy a home. Once available, this new product will be offered in place of the Lifetime ISA.

Aim to use your ISA allowance in full to shelter savings and investments from the current tax levels and the proposed increases. Whether you should use a Cash or Stocks and Shares ISA will be dependent on your individual circumstances, but the ability for investments to keep pace with inflation over the longer term means that for most, a Stocks and Shares ISA is likely to be more appropriate.

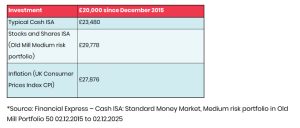

In her speech, the Chancellor made reference to the lower returns available from Cash ISAs held long term, and this appears to be partly behind the decision to reduce the Cash ISA allowance.

The table below looks at the last ten years and shows the difference between holding money in a Cash ISA against the return from an Old Mill medium risk portfolio and inflation over that period.

Cash vs Investing of £20,000 in an ISA over last 10 years

Paying more into your pension

Despite persistent rumours of changes to pension taxation, there were no announcements in this Budget. We have written before that while IHT on pensions has made their use as an estate planning vehicle much less attractive, they are still a tax-efficient way to save for your retirement income.

Changes could still be made in the future, but as we see below, pensions have the ability for high levels of tax relief, which can make pension contributions worthwhile.

While the rules remain the same, you can pay up to the level of your earned income, to a maximum of £60,000 into a pension each tax year. There is also currently the ability to carry forward unused pension allowances from previous years, which could potentially permit contributions to be paid of up to £220,000 and receive full tax relief.

Retaining personal allowances

There are also instances when the level of tax relief can be higher than the marginal rate of tax.

When your income (adjusted net income) is greater than £100,000, your personal Income Tax allowance is withdrawn by £1 for every £2 above this limit until there’s no personal allowance at all once income is over £125,140. A pension contribution can help bring income back down below £100,000 to retain the personal Income Tax allowance.

Someone with a total income of £125,140 could get effective tax relief of 60% on a pension contribution of £25,140. This would be just enough to retain their personal allowance. That’s 40% tax relief on the £25,140 going into their pension and a further 20% by getting their personal allowance back.

Avoiding the High Income Child Benefit Charge

For those with younger children and a salary above £60,000, if you or your partner are receiving Child Benefit, there is the High Income Child Benefit Charge (HICBC), which starts to offset the benefit, with the tax charge at the rate of 1% of the benefit for every £200 over this threshold equalling the benefit once income reaches £80,000.

By making personal pension contributions, it is possible to effectively reduce your income for child benefit purposes and reduce the charge.

This is, however, a complex area and depending upon your level of income, there are set rules as to how much you can contribute during a tax year and obtain tax relief, so do be careful and seek advice before making a pension contribution.

Company pension contributions

For many, pension contributions are made by their companies/employers. Tax relief on employer contributions to a registered pension scheme is given by allowing contributions to be deducted as an expense in computing the profits of a trade, profession or investment business, and so reducing the amount of an employer’s taxable profits.

Any change to tax relief on personal contributions may not impact this, but the wider changes to how benefits are taken and IHT on the fund will be applicable.

Changes to Salary Sacrifice

The Government is capping the National Insurance (NI) benefits of pension contributions made by salary sacrifice to £2,000 from April 2029. Contributions above this level will still benefit from tax relief in the normal way, but will be subject to both employer and employee NI.

The NI charges should be implemented automatically via payroll and there will be no need for employees to declare anything to HMRC.

All employee contributions made via salary sacrifice will continue to reduce adjusted net income, which can help restore benefits and allowances such as child benefit and the personal allowance as described above.

The change will cover both existing arrangements and any new arrangements.

If you are already benefitting from salary sacrifice schemes, you will need to wait to see how your employer reacts to the changes but in the meantime will continue to benefit from the NI saving for existing and new sacrificed amounts. It is unlikely that there will be any immediate changes given the timescales. However, if your employer is offering an enhancement to their contributions, you are likely to see this removed by April 2029.

Property

There were several rumours of additional property tax, with potential reform discussed for Stamp Duty, perhaps replacing the one-off charge with an ongoing amount, and correctly highlighting the announced additional Council Tax for higher value property.

The Chancellor announced the introduction of a High Value Council Tax Surcharge (HVCTS) – an annual charge which will be payable from April 2028 in addition to Council Tax by owners of residential property in England worth £2 million or more. Properties above the £2 million threshold will be placed into bands based on their property value. The surcharge is expected to start at £2,500 for properties valued between £2 million and £2.5 million, rising to £7,500 for properties valued in excess of £5 million.

Charges will increase in line with CPI inflation each year from 2029/30 onwards. The Government will consult on the implementation of HVCTS in the new year.

Landlords

Landlords have also been facing change over the last few years with increased regulation, watering down of mortgage interest relief and changing legislation with reform of tenancy rights. Additional taxes on landlords had been rumoured, including a potential National Insurance (NI) charge that could be imposed on rental income.

We now know the basic, higher and additional rates of Income Tax on property income will increase on 6 April 2027 to 22%, 42% and 47% respectively.

Other tax wrappers

Where investments are held outside of pensions and ISAs, it is increasingly difficult to avoid incurring additional tax. As a result, and depending on your circumstances and size of investment, we may consider other tax wrappers and, in particular, onshore and offshore bonds.

These can defer some or all taxes over time, with a potential tax payment only falling due when you make withdrawals above a certain level or once the bond is encashed. The tax considerations of such bond wrappers also have to be balanced with their increased complexity and cost.

Your planner will be able to determine whether the use of a bond wrapper may have a role to play in your financial planning.

Get in touch

If you have any questions or want to discuss your individual circumstances, an Old Mill financial expert will be pleased to hear from you.