Bubble fears – tilt, don’t tinker

The financial media and market commentators persist with scaremongering and speculation. An AI ‘bubble’, the future of cryptocurrency and Bitcoin, Government debt levels, ongoing trade wars and other geopolitical tensions dominate headlines. In general, this is nothing new. It is a feature of capital markets and the noise that surrounds them.

5th November 2025

-

Gavin Jones See profile

Gavin Jones See profile

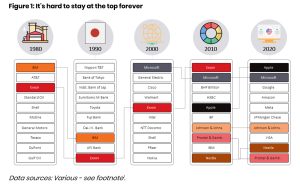

One such story connected to several of these themes is the US stock market and some of the big tech companies. The U.S. allocation in global indices is high at around65%, technology looms large at around30%, and the biggest companies feel all-important – the top ten largest stocks now account for around 25% of the global market. It can feel like the same story on repeat.

Recent decades remind us that market leadership changes over time. These episodes have come and gone across sectors, styles and countries – energy and autos in the early 1980s, Japan in the 90s, ‘dot-com’ stocks at the turn of the millennium, and so on. Today’s concentration is notable, but not unprecedented.

That won’t stop the headlines. Narratives about ‘overpriced tech’, ‘bloated US markets’ and ‘inevitable decline’ are everywhere. The diagnosis is often similar, the prescriptions, wildly different. Should you underweight the US or tech? Bias towards home markets? Add gold, private equity – or even Bitcoin? Or is it time to head for cash? It is worth remembering that every decision to exit an asset class requires a subsequent decision on when to re-enter.

As John C. Bogle, founder of Vanguard, famously said:

“The idea that a bell rings to signal when investors should get into or out of the stock market is simply not credible… I don’t even know anybody who knows anybody who has done it successfully and consistently.”

The cost of getting it wrong – whether through emotional decisions or misplaced confidence in a ‘system’ – can be high. The world may well be in ‘bubble’ territory. Equally, it may not. Only with hindsight will any investor know with any degree of confidence.

The lack of consensus is telling, as these views are already reflected in today’s market prices, just as those betting that U.S. tech will keep leading the charge are too. While it is right to feel nervous about some of the valuations we are now seeing, we have been looking at this issue for a number of years, and despite a US stock correction in 2022, companies are holding onto high stock valuations. In terms of the risk that this poses for your portfolio, this is one of the reasons we diversify widely. We have these stocks, and in the last ten years or so, they have driven a large part of the growth we have seen.

Part of constructing an evidence-based portfolio means accepting that markets work well and are thus extremely difficult to second-guess consistently. That does not mean that your portfolio is not suitably diversified if one or more of the above narratives come to pass. Rather than relying on what any speculator might suggest, your portfolio uses markets to deliberately ‘tilt’ towards stocks from emerging markets, those that are ‘undervalued’ or whose smaller size suggests they exhibit higher risks than those large companies that dominate the market.

The benefits of this approach are twofold: firstly, if markets work, then the flip side of higher risk is higher returns, which ought to be enjoyed over time. Secondly, these riskier stocks tend to behave differently from the market, meaning a diversification benefit is on offer, which should mitigate worst-case scenarios. If one part of the portfolio is zigging, the other might be zagging.

To manage the risk this can present, we include smaller companies, undervalued companies, emerging market companies and property companies, as well as the defensive assets you hold to reduce the concentration of risk. Looking at a medium risk portfolio 50, the big names – Nvidia, Microsoft and Apple have around a 1% allocation. Technology as a whole is about 12% of the assets in the portfolio.

Asset class diversification for this portfolio is shown below.

No one knows what the future holds, and owning a highly diversified portfolio spread widely across asset classes (bonds, equities, and property, for example) and across global markets, industry sectors and companies, helps make sure that we are prepared for whatever the markets throw at us over time. We think that generating good inflation plus long-term returns takes time, patience, and belief in the markets.

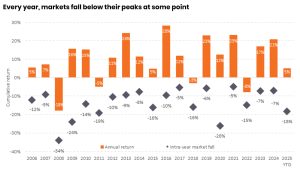

Investment volatility caused by events is a feature of stock markets. Trying to second-guess when to disinvest and then reinvest is as likely to result in a lower return than holding on to companies and high-quality assets through any extreme market volatility. We have written before about the lost returns by missing the best days in the market, and that every year markets fall, so whilst selling and getting back in a later date works in theory, it is very difficult to do in reality.

The chart shows the annual return in each year, indicated by the orange bar and the biggest fall during the year as a blue diamond. So in 2020, during the Covid crisis, at one point the market was down 26% but finished the year with an annual return of 12%.

While headlines will always focus on what’s happened recently and what’s next, our approach remains grounded in evidence and process. By letting market prices lead and tilting sensibly, we aim to deliver resilient outcomes, whatever the future holds. Tilt, don’t tinker.

[1] 1980 & 2000: City Index (2023). 1990: Research Affiliates. 2010 & 2020: Vanguard Global Stock Index.

If you would like to discuss your portfolio, please contact your financial planner.