Care home pressures and why this matters to your future

The ability to pay for care will determine how much control someone has over their future should care be needed. This article examines some of those pressures and highlights some issues as part of your financial plan.

26th February 2025

-

Chris Tweedie See profile

Chris Tweedie See profile

The UK’s population is aging; the International Longevity Centre (ILC) predict that the number of people over age 65 in the UK will increase by 53%, from 11.2 million in November 2022 to 17.2 million in 2040.

The Government’s ‘Operational guidance to implement a lifetime cap on care costs’ (published in September 2021 and updated in January 2023) states that:

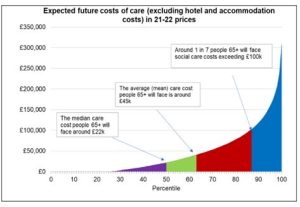

‘Care and support needs are unpredictable. Many of us will need some form of care and support over the course of our lives. Around three out of four adults over the age of 65 will face care costs in their lifetime. However, the amount we will be expected to spend will depend on the level of our needs. Some of us will be fortunate and spend a minimal amount, but one in seven people will face care costs of more than £100,000, excluding hotel and accommodation costs (see figure 1 data from Department of Health and Social Care analysis based on Care Policy and Evaluation Centre modelling). Roughly one in ten individuals will face care costs above £120,000 over their lifetime’.

For readers, the most alarming point in the government statement above is that hotel and accommodation costs (including food and personal requirements) are additional to the £100,000 care costs that people will face. These hotel costs can be significantly greater than the care costs.

Carehome.co.uk in their article ‘Care Home Fees and Costs: How Much Do You Pay?’ (14 January 2025) reports that average weekly residential care costs are £1,410 per week across the UK. This type of care does not include any nursing component, it’s mostly hotel and accommodation costs. In the South West of England, the fees can be considerably higher.

The care home industry is under huge financial pressure and the position could well worsen. Under 50% of care residents are self-funders, meaning the majority are supported by the Local Authority to meet their care needs, which brings ongoing profitability challenges for care homes.

Furthermore, care homes face quality standards assessments according to The Lancet (Lancet Healthy Longev 2024;5e297-302) the Care Quality Commission (CQC) forced involuntary closures of 816 care homes (representing 19,918 registered beds) from January 2011 to September 2023.

Independent corporate finance company, CIearwater International, reported that the UK care industry faces employee retention and recruitment challenges, including wage inflation, loss of staff due to Brexit and the pandemic, and the impact of vaccination status on staffing, are shown to be ongoing problems across the sector, with workforce solutions key to delivering services.

With rising costs, the only option to remain profitable is for care homes to raise their fees. If care homes cut costs too much then they risk poor care delivery outcomes and possible censuring and even closure by the CQC. Both of these points are not good news for the consumer who already consider care fees to be extortionate, and the provision of care home beds insufficient to meet demand.

Care cap / Higher means test threshold

The proposed measures for a cap on the cost of care of £86,000 in a person’s lifetime, and an increase in the means test threshold from £23,250 up to £100,000, were abolished by Rachel Reeves on 29 July 2024. Local authorities had previously petitioned central government to abandon the proposals on the grounds that they would cause local authorities to go bankrupt, many of whom were already deep into the red on their care funding budgets. The incoming Labour government saw this and the black hole as insurmountable and abolished the measures.

Improved profitability for the care industry is the solution

With costs difficult to control, the next step that care homes can take is to only accommodate clients who are self-funders and can pay the full rate of fees for the duration of their stay. More and more care homes are doing this and building it into contracts.

So, in order to have the maximum choice and control over future care provisions, it’s crucial that people have enough resources to pay for care indefinitely, however expensive it becomes, for the rest of their lives.

How Old Mill can help

- Plan ahead to check how much future care might cost you. Your financial planner can run cash flow forecasts to estimate in advance how well provided for you are.

- If planning on making gifts, undertake a future care adequacy check first. Only gift away what you are certain you will never need yourself in the future.

- If care is likely to be needed, take advice on how best to pay for it. Most people’s income is well short of the care fees they may face. Our Society of Later Life Advisers experts (SOLLA) at Old Mill can advise you on how to reduce the care fees shortfall (see below; Steps to take if you need care now) and optimise the use of your finances.

- Don’t leave care planning and funding issues too late so it becomes a crisis management issue. Clearly, you can’t be sure if a sudden illness (e.g. a stroke) will occur, but after the age of 60, the likelihood of such an event increases almost exponentially.

Take advice to ensure optimal use of financial resources and improve the chances of positive financial outcomes.

Steps to take if you need care now

There are numerous steps that a qualified (Society of Later Life Adviser) care funding planner will go through to optimise the use of financial resources, which are:

- Ensure a Continuing Health Care (CHC) assessment is undertaken if there is a likely primary care need.

- Ensure a Funded Nursing Care (FNC) assessment is undertaken (if there is no eligibility for CHC) to check for eligibility for this benefit.

- Ensure Attendance Allowance (AA) is claimed at the appropriate level – higher level where possible.

- Where capital exists consider using an Immediate Needs Annuity (INA) to increase guaranteed income for life, the aim would be to plug the gap entirely if CHC is not available.

- Analyse and understand the financial resources to clarify the short-term and long-term adequacy positions.

- If an INA is not viable how best to use a combination of steps 2, 3, and 5 to ensure finances last as long as possible and hopefully for the entire period of tenure in care.

What is an Immediate Needs Annuity (INA)?

It’s a financial product called an annuity that provides additional guaranteed income for someone in care. The main features of an INA are as follows:

- Capital is used to buy an annuity – it’s an exchange of a cash lump sum for an ongoing income. It’s effectively buying extra pension income.

- The income is tax-free where it’s paid to a Care Quality Commission (CQC) registered care provider.

- The income is paid until the person receiving it (the annuitant) dies. The contract comes to an end at this point. The capital has gone.

- The income can be level or escalating.

- Escalating income can be arranged in line with the retail price index (RPI) or at a fixed increase of up to 10% p.a.

- Short-term death benefits are automatically included in case of death in the first few months of the contract.

- Long-term death benefits are optional and can be built in so that capital may be returned on a decreasing basis when the annuitant dies. This protection costs more (it’s an insurance added to the annuity). The protection can be set at levels up to 75% of the amount used to buy the INA (the initial premium amount). Typical levels of protection that are considered are: 75%, 50% and 25%. Death benefit cover decreases with each annuity payment made, so eventually, if the annuitant lives long enough, the life cover runs out.

- Deferred annuities can be arranged where the benefits do not start for a set period of time, for example, one or two years. You fund the care for the deferred period and the annuity pays the shortfall (or most of it) after the shortfall ends. Deferred annuities are much cheaper to buy.

- The guaranteed income provides peace of mind to the annuitant/their family or representatives.

- The income level, after claiming the appropriate benefits is calculated to meet the care shortfall so the individual has long-term financial security.

- The Court of Protection (in Deputyship cases) approve the use of INAs (where used suitably) because the product brings certainty to the planning arrangement and can be used to guarantee financial security for life.

If an INA is not viable, for example, a) if the capital available is insufficient to buy an annuity, or b) the annuity is too expensive meaning that the INA is not good value for money, then prudent management of cash and investments can improve the likelihood of funds lasting longer, although this may not guarantee that funds will not become entirely depleted.

Final thoughts

Considerations about future care and active planning can help avert a future crisis. The care industry continues to face challenges going forward and most of these relate to cost-based issues which will be passed onto clients. The key to your future security, if you need care, is to not run out of money, i.e. stay as a self-funder and not need local authority support.

To dicuss this futher speak to Chris Tweedie direct or contact us here.