Commercial property – please don’t pick on me!

For many investors, commercial property (often referred to as ‘real estate’) provides an opportunity to diversify some of the pure equity risk in portfolios. Owning property directly (either individually or via a ‘bricks and mortar’ fund) comes with liquidity and diversification challenges. Investment via Real Estate Investment Trusts (REITs) helps to mitigate this. A real estate investment trust (REIT) is a property investment company with special tax rules to very broadly, simulate (from a tax perspective) direct investment in UK property. They are listed on global stock markets, and shares in the company are freely tradeable and easily realisable as opposed to bricks and mortar.

6th October 2023

-

Gavin Jones See profile

Gavin Jones See profile

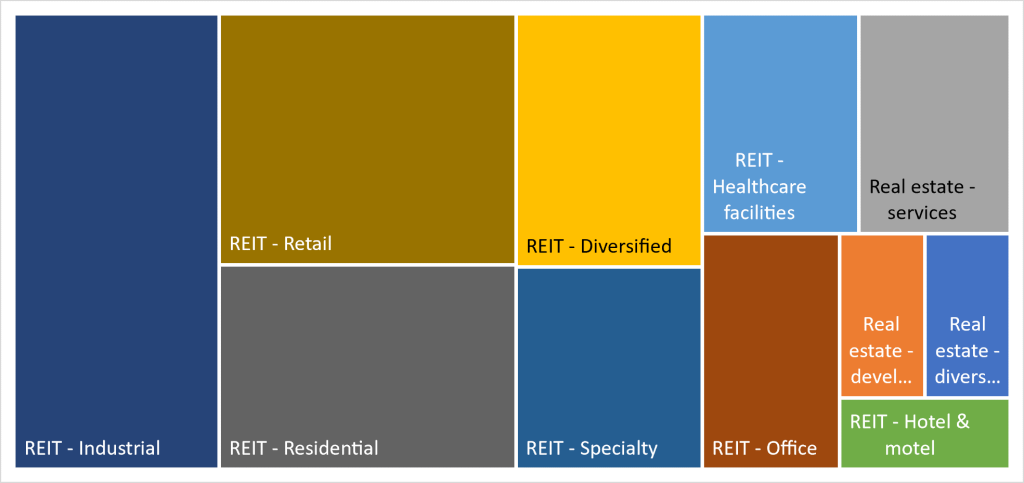

A common misconception is that REITs are made up of exposure to predominantly offices, retail shopping centres and warehouses, but that is to miss the much wider scope of what global commercial property represents these days, as the chart (Figure 1) below illustrates.

Figure 1: Global commercial property is far more than offices, retail malls and warehouses

Source: Morningstar Direct © All rights reserved – sector breakdown of iShares Developed REIT Index (IE) D Acc £.[1]As at 31/07/2023

Over the past 20 years, global REITS have delivered around 4.5% above inflation returns and a little under 3% above inflation over 10 years[2]. That is a pretty good outcome, as it is not unreasonable to expect that global commercial property has a long-term expected return lying somewhere between those for bonds and equities, which have historically delivered around 1% and 5% above inflation over the longer-term[3].

Over the past 10 years every property sector has contributed positively to portfolio returns. Perhaps unsurprisingly – on account of the pandemic’s unforeseen impact on working patterns – office property has been the worst performing sector over the past five years.

[1] See here for sector definitions (pp 15-17): https://indexes.morningstar.com/resources/PDF/Methodology%20Documents/SectorArticle.pdf

[2] Using the S&P Global REIT Index in GBP to 31/07/2023

[3] Broad estimates based on long-term data – for illustration purposes only.

The past three-year period has been less rewarding than owning the broad global equity market – almost everything was! REITs are up about 6% and global equities are up around 11% per annum to 31 July 2023, although much of the return of the latter relates to just a handful of mega-sized US companies. Over the past year, returns have been -12% and +7% respectively. The rapid rise in interest rates across much of the world will no doubt have contributed to investors’ less optimistic views on the potential returns available from real estate companies. All property sectors over the previous 12 months have delivered a negative contribution to performance. That is the nature of investing.

Such differences between asset classes may, unfortunately, tempt some investors into questioning why they continue to own property companies (or any other investment for that matter that has recently performed less well than others). The doomsters narrative for Global REITs goes something like this ‘shopping malls are history, everyone knows that online shopping is going to put them out of business’ or ‘offices are done for, as no-one is going into work these days’. ‘And with interest rates rising…’

Yet that is to ignore two very important aspects of investing.

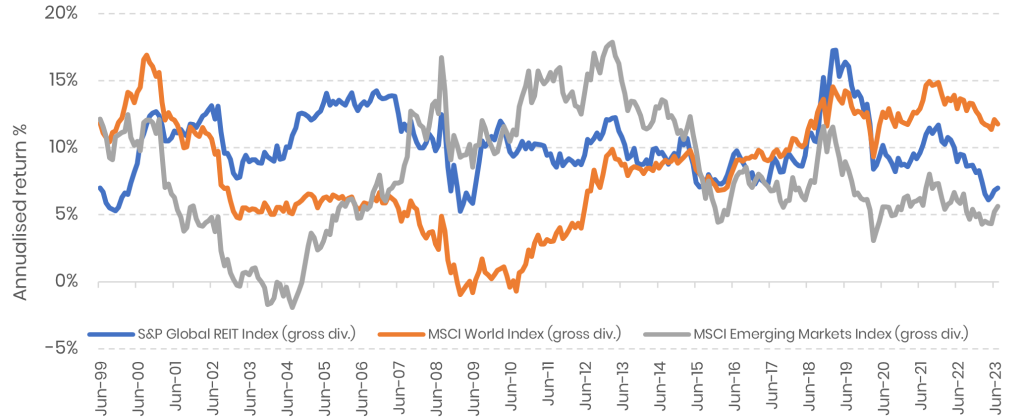

The first is that every asset class has its day, year or run of years. Over the past few years, that has largely been the US market and growth-oriented tech stocks in particular. Look back to the decade from 2000 to 2010 and the US equity market was the laggard as it endured its ‘lost decade’. The chart below (Figure 2), which you might have seen before, highlights the fact that every asset class has extended good and bad periods. To lose faith in a sensible allocation, simply on the back of poor recent performance is best avoided.

Figure 2: 10-year rolling returns of different asset classes before inflation (to Monday 31 July 2023)

Source: Morningstar Direct © All rights reserved

The second point worth remembering is that all of the information available and investors’ views on commercial property are already baked into today’s prices, including not only the pessimistic news but also, for example, the possibility that in the future offices may well be repurposed, perhaps into city living. Unless something fundamentally changes the validity of the decision to invest in the first place, it makes good sense to stay with the strategy, despite disappointing short-term performance. Don’t pick on commercial property just because it is out of favour.