Defensive assets

Investors sometimes convince themselves that they know what the future holds and seek to position their portfolio to benefit from that knowledge. As one of our clients, you will know that this is not a game we play when it comes to investing your money.

7th July 2023

-

Gavin Jones See profile

Gavin Jones See profile

A topical example is the belief earlier in the year that central banks around the world were reaching the peak of their base rates – the rates that they pay commercial banks who lend them money – as inflation was expected to decline. The theory is that higher interest rates are passed through the economy and end investors are encouraged to save rather than to spend, reducing the impact of inflation[1]. Central bankers, however, will be the first to admit this task is more difficult than it sounds!

Bond investors know about base rates; they also know that central banks use them as a tool to try to control inflation. Therefore, the market already has an expectation of what the future base rate will be, which is reflected in current bond prices.

The reality is that prices adjust to new expectations due to the, by definition, random release of new information that we experience each and every day. In June, persistent inflation, in the UK in particular made investors reconsider their expectations. One of the indicators of this was mortgage lenders increasing their rates through June in expectation of higher rates going forward. By the time the Bank of England announced base rates were to increase to 5% on Thursday 22 June much of that rise had already been anticipated by lenders and the increase was already incorporated into their interest rates.

Over the last few months, stubborn inflation has led to a strengthening in wage inflation. In response the Bank of England has continued to steadily raise interest rates in the UK to dampen this demand.

[1] Bank of England (2022) Interest rates and Bank Rate. Target = 2%. https://www.bankofengland.co.uk/

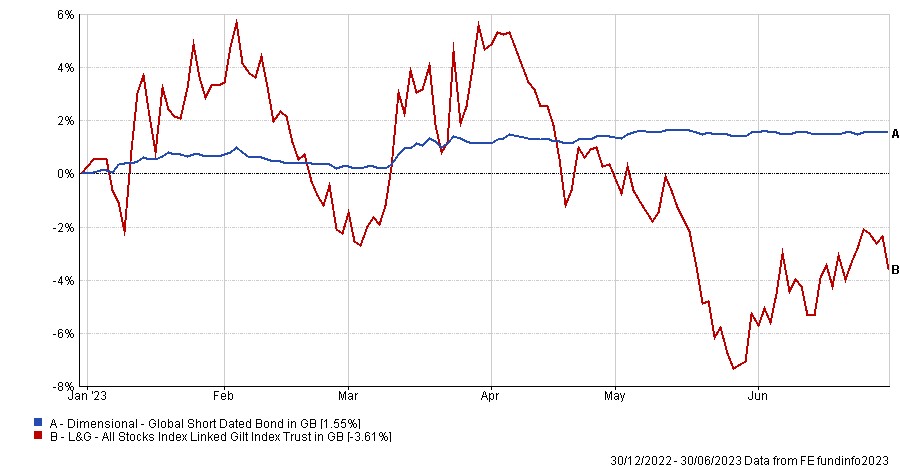

Your bond exposure is not just to the UK market. The main fund we use, as shown in the graph below, (Dimensional Global Short Dated Bond Fund) invests globally so will be exposed to other markets with the biggest exposure to Canada and the US where inflation has been falling faster and there is a greater expectation of a cut in interest rates earlier than the UK (L&G All Stocks Index Linked Gilt Index Trust).

The Legal & General Index Linked Gilts fund has a longer duration so is naturally more volatile.

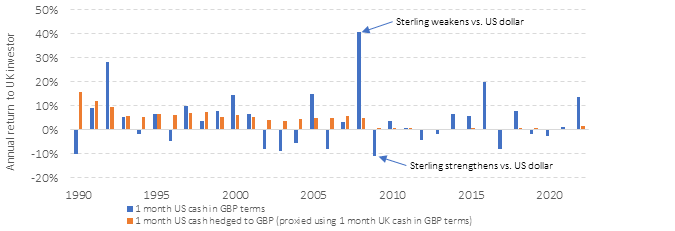

Buying foreign bonds increases the choice of bonds for investors and diversifies the risk of interest rate movements across markets. A foreign bond comes with currency risk between the currency of issue (e.g., US dollars) and the base currency of the investor (e.g., Sterling for a UK investor). Currency exposure introduces an equity-like risk into the bond portion of portfolio, creating a volatile asset. Let’s run a quick experiment. For simplicity’s sake, imagine that you placed a deposit in US dollars for one month and rolled it over each month without hedging the currency, from 1990 to 2022. Imagine too, an alternative scenario where you hedged the US dollars back to GBP, in effect ending up with a synthetic GBP cash deposit, as the cost of hedging is calculated using the difference between the two interest rates (unfortunately there are few free lunches in investing!). The chart below reveals the material difference in annual outcomes. The orange bars represent the hedged interest rates and the blue bars, the unhedged interest rate. At times you would have been very happy with the unhedged return – in the Global Financial Crisis as sterling weakened this gave an equivalent interest rate of 40%. But this would be balanced by all the times the interest rate is negative – meaning the value of your deposit fell in value which is undesirable for defensive assets.

Figure 3: Currency adds material volatility to the equation (1990-2022)

Data source: Federal Reserve and Bank of England.

Investors need to be able to talk themselves out of a sensible starting point of shorter-dated, higher-quality, currency-hedged bonds, when deciding what type of bonds to own.