Donald Trump makes his mark

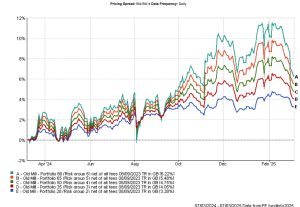

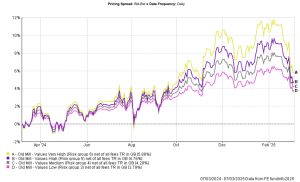

February proved to be a relatively chaotic month with a rapidly evolving US policy in many areas from President Trump’s incoming Administration. While markets have taken the first month of a Trump presidency in its stride, the pace of change has increased with tariffs on goods, for China, Mexico and Canada and erratic foreign policy with Ukraine and Gaza resulting in falls in global stockmarkets over the last few weeks. The graphs below show this fall in the context of growth over the year. Based on the risk you are willing to take there have been sharp falls at the end of February and beginning of March but to date the performance over the last year has been positive.

11th March 2025

-

Gavin Jones See profile

Gavin Jones See profile

Performance over the last year (up to Friday 7 March 2025)

Performance of the Values portfolios over the last year (up to Friday 7 March 2025)

Being an investor in markets like this is not easy. We must contend not only with the erratic and unpredictable nature of markets but also with the sometimes erratic and irrational ways in which we are tempted to think and behave.

As Benjamin Graham, one of the great investment minds of the twentieth century, famously stated (Graham and Dodd, 1996): ‘The investor’s chief problem – and even his worst enemy – is likely to be himself.’

Avoid ‘fast’ decisions when investing

Our brains take two approaches when making decisions: ‘fast’ decisions are often intuitive and emotional, and ‘slow’ decisions that are logical and rational[1].

The problem we face is that we tend to use our ‘fast’ decision-making process more often under a set of conditions that apply to the types of decisions we face as investors. These include complexity, incomplete and changing information, when we are stressed, and when we need to make decisions that involve other people in the process (Montier, 2010).

Source: Albion Strategic Consulting

We tend to pay too much attention to recent market events, such as the news surrounding President Trump’s latest policy decisions. Some are tempted to look at what has happened in the past and feel that this was predictable (hindsight bias), implying that forward-looking predictions are easy. We may be overconfident in an ability to pick good investments and see patterns in the markets where none probably exist.

[1] In 2011, Daniel Kahneman, who previously won a Nobel Prize for Economics, published his book called Thinking Fast and Slow (Kahneman, 2011), which takes you through the two thinking systems in depth. This is great read for those who are interested in the subject.

So, what can we do?

The key to curbing the fast driven thinking system and firing up the logical and rational part of our brain, is to give it the time and space to reflect on the challenge at hand. A good starting point is to ask yourself – perhaps in conjunction with your financial planner – a few questions. If you really want to turn on your logical decision making process , then write down your questions and your answers. If you have the urge to act on your portfolio, ask yourself the following:

- Are you being influenced by recent events, such as good/bad market or fund performance? Does this go against the investment approach that you have previously bought into?

- Do you think that you have some form of insight into the investment decision that other bright and dedicated investors do not? Remember that most professional managers fail to beat the market!

- Are you under the illusion that investing is easy, as what just happened was ‘obvious’ looking back at it?

- If so, are you tempted into making predictions about the future? If so, polish your crystal ball, wave your rabbit’s foot, and cross all fingers and toes. It is well-nigh impossible as markets do a pretty good job of reflecting information into current prices.

- Are you being swayed by the familiar? Do you know the company, industry, or markets better than other possible options? Be careful of familiarity bias.

- Are you very excited by the trade-off between the returns promised and the risks you are taking? If so, look hard, as these opportunities are rare. It is probably just that you have not fully uncovered the risks that you will be taking.

At the end of the day, the poor decisions that we make based on our emotions and driven by the biases we all suffer from result in less money in our retirement (or other) investment pots, which will have lifestyle consequences down the line. By heeding these simple bits of advice, we can at least buy ourselves a little time to allow our reflective, logical brains to kick in and control the narrative, wrestling it away from our intuitive reptilian brains. Stick with your investment process and avoid temptation.

His impact on markets

So, how does all this impact on markets? When he was first re-elected, the US equity market rallied, perhaps as its view on future corporate earnings was favourable. On the other hand, the US bond market has suffered rising yields (falling prices) on the prospect of higher inflation on account of the strong economy and the prospect of Trump’s tariffs.

Going forward, no one knows what the impact will be of Trump’s second term in office. Markets will reflect new information as it is released, which is by definition a random event. We are yet to see the impact of the burgeoning global trade war in response to US tariffs and possible events such as a military clash with China over Taiwan, a deal with Russia and what that may mean for Ukraine and a highly confrontational dialogue with Iran. As investors, all we can do is remain highly diversified across equity markets, sectors and companies, and balance our equity risk by holding an adequate amount of higher quality bonds to see our way through any prolonged downturn in equity markets, if they should occur. We are, as ever, in uncertain times.