Emotions and market timing are likely to be costly

One of the greatest temptations in investing is to try to time when to be in or out of markets. It is logical to want to be fully invested in the equity markets when they are going up and to be in cash or bonds when they are going down. Yet logic transforms into emotion at times when markets feel a little bit frothy on the upside, such as the late 1990s or even 2020-21, or full of gloom and despair on the downside, such as the depths of 2003 (technology crash), 2008-9 (Global Financial Crisis), Q1 2020 (Covid) or the challenges of 2022 for both bonds and equities.

9th November 2023

-

Gavin Jones See profile

Gavin Jones See profile

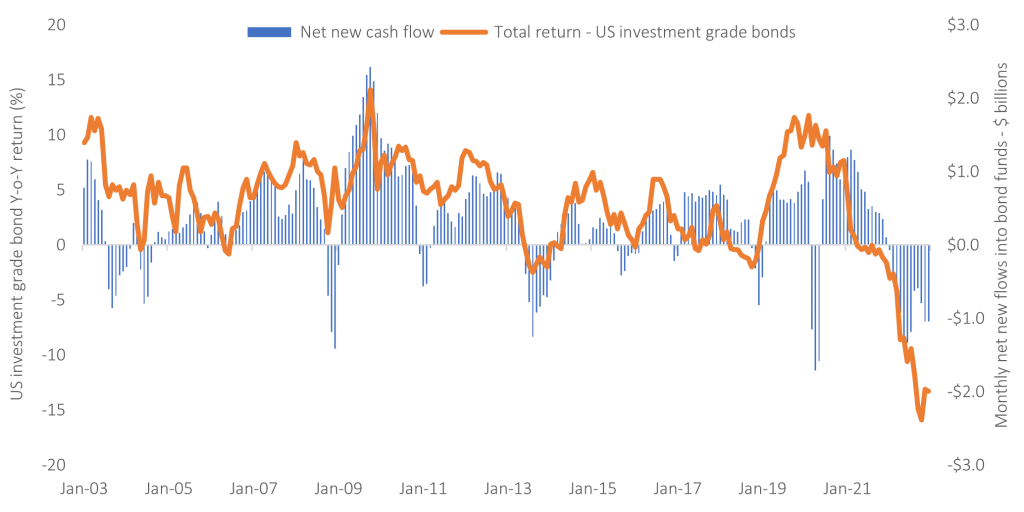

Yet, these temptations are strong. As an example, the chart below provides an insight into US investors’ net flows into bond funds annually over the past 10 years. Whenever bond returns are strong money flows into bond funds, and conversely, when they are weak or negative, investors tend to sell out of bonds, with 2022 being a prime example. This is the opposite of ‘buy low, sell high’, buying as prices rise, only to sell when they fall is a fast track to wealth destruction.

Figure 1: Some investors tend to be influenced by good or bad performance

Source: Net flows ICI Funds Factbook 2023[1], bond index data from Morningstar Direct ® All rights reserved (see endnote).

It is worth remembering that every decision to get out of any asset class also requires a decision on when to get back in, and vice versa. It would be great news if there was a clear signal that allowed us to make these calls, but as the late, great John C. Bogle, the founder of Vanguard once said:

‘The idea that a bell rings to signal when investors should get into or out of the stock market is simply not credible. After nearly fifty years in this business, I do not know of anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has done it successfully and consistently. Yet market timing appears to be increasingly embraced by mutual fund investors and the professional managers of fund portfolios alike’.

A recent piece of research looked at market timing strategies with respect to equity market, size, value, and profitability premiums in the US, developed ex US, and emerging markets. In all, the authors looked at 720 possible strategies[2]. Of these, only 30 showed any real promise, at least at first. On further investigation, they were shown to be very sensitive to the time periods under study and how any live strategy might be constructed. Without deep insight and testing of the robustness of these thirty strategies, it would be easy to see how investors might have thought they had found the ‘holy grail’ they were looking for. Sadly, not.

Perhaps this should be no surprise, given that markets do a pretty good job of incorporating new information into prices quickly and that would include any signal indicating that now is the time to get out of (or into) equity markets! Any new information is, by definition, a random event.

A paper by AQR – a systematic hedge fund manager in the US – with an exceptionally bright and talented team, stated [3]:

‘Successful market timing is a tantalizing holy grail for investors, especially when there seems to be persuasive evidence that simple valuation measures can predict subsequent market performance. But, as both researchers and investors have discovered, outperforming a passive buy-and-hold approach is harder than it might seem.’

We agree. The costs of getting it wrong – either through making emotional decisions or believing one has some ‘system’ that rings Bogle’s bell – are likely to be high.

Stay invested. As we have said many times in the past, the secret to success is time in the markets, not timing the markets.

[1] Net new cash flow is reported as a percentage of previous month-end bond mutual fund total net assets, plotted as a three-month moving average. Data exclude high-yield bond mutual funds.

[2] Another Look at Timing the Equity Premiums. Dai W, Dong A. Dimensional Fund Advisers – Research (2023)

[3] Asness, C., Ilmanen, A., & Maloney, T. (2017). Market Timing: Sin a Little. Journal of Investment Management, 15(3), 23–40.