Financial Independence. Retire Early (FIRE)

The idea of gaining financial independence to retire early is not a new concept; indeed, it’s something many have aspired to across generations.

Inspired by the 1992 book ‘Your Money or Your Life’, by Vicki Robin and Joe Dominguez, millions of people are now following the FIRE formula and aspiring to retire well ahead of reaching the age of 65.

So, what does the FIRE lifestyle involve and how achievable is it?

22nd March 2022

-

Gavin Jones See profile

Gavin Jones See profile

What is FIRE?

FIRE is a movement or lifestyle that encourages:

- Saving as much of your income as possible (up to 70%)

- Paying off all your debt, including your mortgage

- Investing in a low-cost way

- Building up a net worth of 25 times your estimated annual spending

- Drawing a maximum 4% from your savings/investments each year to fund your retirement

- Having 3-6 months of savings in your emergency fund.

Finding the balance between saving hard to facilitate early retirement and actually enjoying one’s life in the now is part of the challenge for those aspiring to achieve FIRE. It’s very much a personal journey, advocating mindful spending and living life in line with your values alongside maximising your income by potentially having ‘side hustles’ and looking at other ways of generating passive income alongside your main job.

Practical considerations of achieving FIRE

For many, while saving as much as 70% of their income may not be achievable, by adopting some of the thinking and discipline behind FIRE, you may still be able to retire somewhat earlier than might otherwise be possible.

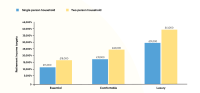

One of the challenges of this approach is estimating how much you may need to spend each year. The table below detailing the results of a Which? Research survey of 6,800 retirees in 2021 shows how much income one might need in retirement based on the participants’ actual spending.

Using the 25X multiplier and based on your own view of how much you want to have to live off every year, it’s possible to work out at a simple level how much you will need in your retirement fund. For example:

Expenditure of £19,000 per annum x 25 = £475,000

Once you have £475,000 invested, the suggested maximum withdrawal rate of up to 4% each year would then fund your £19,000 a year expenditure over time.

The 4% withdrawal rate is derived from studies, largely in the US, that look at the level of income that can be maintained over time, while increasing by inflation. More recent studies suggest that this may be a little high and a rate of 3% may be more realistic (so the income multiplier becomes 33X). This also involves taking a higher level of risk with your investments and may not be for everyone.

Old Mill’s approach and FIRE

For anyone looking to achieve FIRE, we would advocate having a clear financial plan setting out what you want to achieve and by what age.

Our Cashflow Forecasting tool is a great way of looking at how likely it is for your money to last your lifetime and enable you to live the lifestyle you desire, whatever that may be.

Looking at both your income and your expenditure will enable you to get a clearer picture of how much you can realistically save each year and where you might be willing to make sacrifices (or choose your ‘side hustle’) to increase how much you can save to achieve the financial independence to be able to retire early.

Maximising your pension(s), including the State pension and making the most of tax-efficient savings vehicles (like a stocks and shares Individual Savings Account) will almost certainly form part of any financial plan alongside investing in a diversified portfolio.

It’s important to remember that most pensions are not accessible until the age of 55 and that this will increase to age 57 in 2028, so it will be important to take this into account when working out how much you need to have invested in addition to your pension if you want to retire in your 50’s or earlier.

When it comes to deciding which portfolio to invest in, if you need a higher rate of return to achieve your financial goals, you will need to take a higher level of risk in your portfolio. The level of risk associated with any portfolio you choose to invest in is a key factor to understand as is the cost of managing the portfolio. Look for portfolios that are structured to minimise the product and transactional (buying and selling) costs of investing to give a lower cost investment experience rather than more costly approaches that follow a more active management approach (for example, where managers attempt to but rarely outsmart the market).

Summary

If achieving financial independence – the ability to support your lifestyle from passive income, including that from investments, so that you can retire early (i.e., work is no longer an obligation) well before traditional retirement age is something you aspire to, then it may well be possible. It will require discipline, potentially making lifestyle choices that reduce your outgoings and ideally, a well-paid job that will allow you to hopefully save a more significant proportion of your salary so that you can achieve your version of FIRE.