Inflation is a tax on your wealth

It is fair to say we are all too aware of the challenge of inflation when we get to the supermarket checkout, or when paying our energy bills. Inflation does not only affect the spending power of our income today, but also the real value of assets (e.g., investment portfolio assets) that will deliver future spending power, perhaps in retirement.

18th June 2024

-

Gavin Jones See profile

Gavin Jones See profile

While most people understand the nature of this hidden tax, it may surprise many just how big the impact of the inflation head wind has been over the past few years.

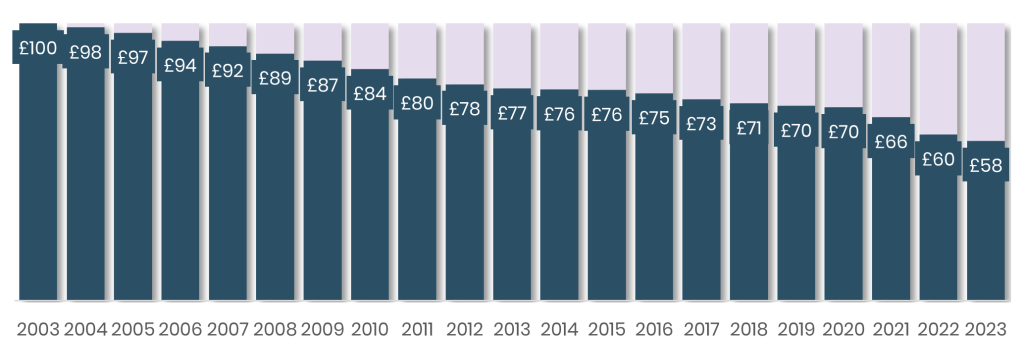

The figure below looks at the impact that inflation has had on the spending power of £100 over the past 20 years. Even periods when inflation has been relatively low, it has silently whittled it away. On average over this period, inflation has been around 2.8% per annum, which does not sound a lot but in reality it is. Over 40% of one’s spending power has disappeared.

Figure 1: The insidious taxation of spending power by UK inflation – 20 years to 2023

Source: Albion Strategic Consulting. Data: ONS – UK CPI

What is to be done?

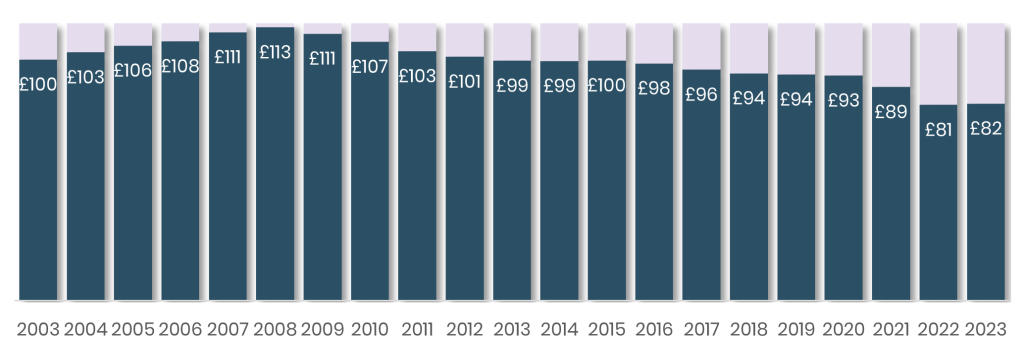

For those building up a pot for retirement, protecting wealth from inflation – and hopefully growing its real (after inflation) value – is very important. The first thing to do is to become an investor, not a saver. For some, elevated deposit rates returning above inflation interest may look appealing. Unfortunately, cash has had a very poor track record of holding its real value, as the figure below illustrates, over the same period. This shows that £100 in cash, over the last 20 years has fallen in its value taking inflation into account, falling to effectively £82 in 2023.

Figure 2: Cash has done a poor job of protecting savers’ spending power

Source: Albion Strategic Consulting. Data: ONS – UK CPI, Bank of England 3m T-Bill (cash)

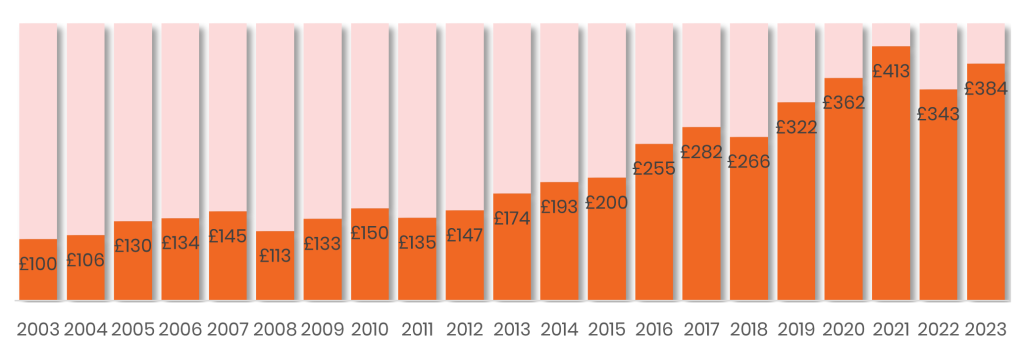

On the other hand, global equities have managed to provide positive real returns for investors over the past 20 years, which includes the equity market turmoil in 2007-2009 during the global financial crisis, and 2022. Here we see that the same £100 invested in global equities will have almost quadrupled in value, after inflation, over the same period.

Figure 3: Global equities have done a better job of protecting investors’ spending power

Source: Morningstar Direct © Period: 2004-2023: MSCI ACWI in GBP after UK CPI.

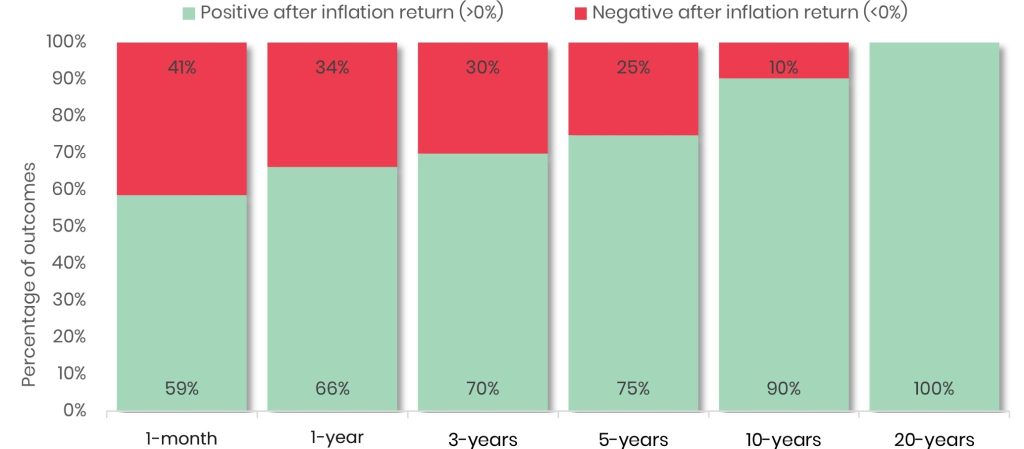

Owners of equities, however, require staying power as these positive inflation-beating returns do not come in straight lines. The figure below illustrates that the longer an investor is able to hold their equity investments for, the greater the chance that they will receive positive, after-inflation returns. So, for the rolling periods of each column (1 month, 1 Year etc.) it shows the percentage of periods the after-inflation return was positive or negative.

So, if you look at monthly periods, while 59% of periods saw growth above inflation, 41% saw returns lower than inflation. Longer holding periods reduce the percentage of negative returns and when you look at 20-year periods over the last 50 years then all have seen growth in excess of inflation.

Figure 4: Equity ownership requires staying power but helps to mitigate inflation

Source: Morningstar Direct © Period: 01/72 – 11/23. Inflation: UK RPI (31/01/88), UK CPI (thereafter). Equities: MSCI World (31/12/00), MSCI ACWI (thereafter) in GBP.

In conclusion

Inflation is a risk that all investors must have in their sights, and it is not an easy one to mitigate in the short term. Over the longer-term, equity assets can help to deliver inflation-plus returns to protect and grow wealth. The key is to cover off this risk as far as possible by owning, and keeping with, a well-diversified investment portfolio. The patient investor is usually rewarded.