Interest rates

15th January 2026

-

Gavin Jones See profile

Gavin Jones See profile

Interest rates

The UK Bank Base Rate was cut from 4% to 3.75% at the Bank of England Monetary Policy Committee (MPC) meeting in December.

The MPC is responsible to try and keep inflation low and stable. It meets regularly to decide what interest rate is needed to return inflation to, or keep it at, the 2% target inflation rate over time.

At the latest meeting, the MPC made the following points:

- We have cut Bank Rate (interest rates) by 0.25% to 3.75%. Since August 2024, we have cut rates six times.

- Inflation has fallen a long way from its peak of over 10% three years ago and is 3.2% in the latest measure.

- We think that Bank Rate is likely to fall gradually further in future, but that will depend on whether variables like pay growth and services inflation continue to ease.

- We set interest rates to make sure that inflation falls all the way back to the 2% target and stays there.

In 2025, inflation actually rose slightly, with the main rate of Consumer Price Inflation (CPI) rising from 3% in January 2025, peaking at 3.8% in July last year before moving down.

The rate of inflation is the change in prices for goods and services over time. CPI measures the change over a year of a basket of goods and services, and the latest figure is for the period to November 2025. The Bank of England try to forecast the future path of inflation, and this enabled them to cut rates at the beginning of 2025, when the rate was 4.75% despite inflation creeping up, with cuts to interest rates in February, May, August and again in December.

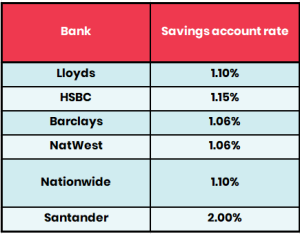

It is unclear whether there will be any further cuts to rates this year, but you should check the rate on any savings accounts you have with high street banks, as typically these remain far lower than market rates. While having a small amount in these accounts for convenience may be fine, you could be losing out on interest if you have more substantial deposits with them. The table below shows the standard savings rates on offer from popular banks.

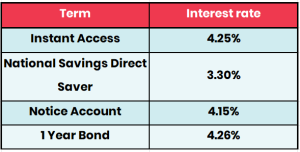

If you have one of these accounts, there are better alternative rates available and below is just a sample. Looking at rates at the time of writing (on 12 January), an indicative sample of the rates you can secure at present is as follows:

Source: Moneyfacts.co.uk 12.01.26

We have not included institutions in the table above as rates change quickly. If you wish to review the interest rates you are getting currently, please do speak to your financial planner.

Cash management services

For those holding larger amounts on deposit, a cash management service may be worth considering. They offer potentially higher interest rates with deposits fully protected and much simpler administration than where accounts are held directly with institutions.

These are essentially platforms to help manage cash deposits and allow you to easily switch between different deposit accounts without having to go through the arduous account-opening process each time.

For those with a larger short-term deposit or entities such as Trusts, pension funds, and companies where opening accounts is more difficult, using a cash management service can greatly simplify the ongoing administration and make it far easier to ensure the overall rate of interest remains competitive.

When you are dealing with a large sum of money, while the interest rate is important, so too is ensuring the deposit is protected by the Financial Services Compensation Scheme (FSCS) in the event an institution becomes insolvent. For individuals, this is £120,000 (£240,000 for a couple), and for entities like a Trust or some companies, this is £120,000 per institution. Opening multiple accounts to ensure the funds remain fully protected by the FSCS can be extremely onerous, especially for Trusts and companies.

If you would like to review the interest rates you are getting currently or want to know more about our cash management service, please speak to your financial planner.

FSCS Deposit Protection Scheme limit increase

On 1 December 2025 the Financial Services Compensation Scheme (FSCS) deposit protection rose to £120,000.

This means that if you hold deposits or savings with a UK-authorised bank or building society and it goes out of business, FSCS can compensate you up to the new limit of £120,000 per eligible person, per authorised firm.

This also covers temporary high balances, which also rose up to £1.4 million. These may occur from major life events, such as selling a home or receiving an inheritance. Temporary high balances are protected for up to six months.