Interest rates & Cash management services

5th November 2025

-

Gavin Jones See profile

Gavin Jones See profile

Interest rates

The UK Bank Base Rate remained at 4% at the Bank of England meeting in September.

The bank began increasing interest rates in late 2021 as a result of rising inflation on the back of all the Covid support, reaching 5.25% before rates started falling again in August last year.

Since then, five rate cuts have brought the UK base rate down from 5.25% to 4% at the most recent cut.

With inflation remaining at 3.8% in September, still well above the Bank of England’s (BoE) target of 2%, it’s unlikely that we’ll see any significant cuts to the base rate over the months ahead.

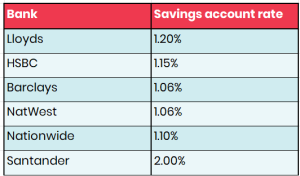

It is unclear whether there will be any further cuts to rates this year, but you should check the rate on any savings accounts you have with high street banks, as typically these remain far lower than market rates. While having a small amount in these accounts for convenience may be fine, you could be losing out on interest if you have more substantial deposits with them. The table below shows the standard savings rates on offer from popular banks.

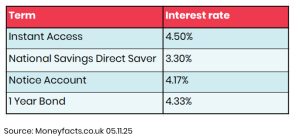

If you have one of these accounts, there are better alternative rates available and below is just a sample. Looking at rates at the time of writing (on November 5) an indicative sample of the rates you can secure at present is as follows:

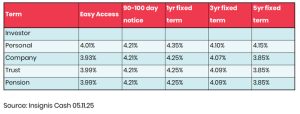

We have not included institutions in the table above as rates change quickly. If you wish to review the interest rates you are getting currently, please do speak to your financial planner.

Cash management services

For those holding funds on deposits in excess of, say, £100,000, whether personally, by a company, a pension fund or a Trust, a cash management service may be worth considering. They offer potentially higher interest rates with deposits fully protected and much simpler administration than where accounts are held directly with institutions.

For those with a larger short-term deposit or entities such as Trusts, pension funds, and companies where opening accounts is more difficult, using a cash management service can greatly simplify the ongoing administration and make it far easier to ensure the overall rate of interest remains competitive.

When you are dealing with a large sum of money, while the interest rate is important, so too is ensuring the deposit is protected by the Financial Services Compensation Scheme (FSCS) in the event an institution becomes insolvent. For individuals, this is £85,000 (£170,000 for a couple), and for entities like a Trust or some companies, this is £85,000 per institution. Opening multiple accounts to ensure the funds remain fully protected by the FSCS can be extremely onerous, especially for Trusts and companies.

Insignis is our chosen cash management service. Insignis has been helping clients manage their cash savings since 2017 with a platform that makes it easier to manage savings, diversify deposits (to benefit from FSCS protection where applicable) and find better returns. While it will be necessary to carry out the normal money laundering checks upfront, once identification is provided, multiple accounts can then be opened from the service, avoiding the need to provide separate identification to each institution with whom a deposit is placed..

If you would like to review the interest rates you are getting currently or want to know more about our cash management service, please speak to your financial planner.