Investing for the long term

Good investing is grounded in three things: -using investment logic to think clearly about what goes into a portfolio; using empirical insights to inform us of general longer-term characteristics of assets and how they work together and the shorter-term exceptions to these generalities; and the fortitude to stick with a sensible portfolio strategy despite shorter-term, trying periods.

7th July 2023

-

Gavin Jones See profile

Gavin Jones See profile

A portfolio mix of bonds and equities balances the potentially severe downside falls in equity markets by owning far less volatile, good quality bonds that will not fall as far, if they do fall at all. There is a general expectation that at times of severe equity market trauma, money seeking a safe haven will move into high quality bonds pushing yields down and as there is a see-saw effect between yields and prices, bond prices will go up. This is often, but not always the case, as 2022 and 1994 demonstrated. 2022 saw these bond prices fall as yields rose in response to inflation.

We are often asked if these assets are still suitable to hold in portfolios and whether they remain ‘lower risk’.

Investment logic still suggests that shorter-dated, high quality bonds will remain a useful balance to extreme equity markets, if and when they occur, providing strong downside protection. At market extremes, scared money will still flow to these assets. Bonds are now yielding substantially higher yields today than 18 months ago with a yield now of 4.7% compared to less than 1% on the global short dated bond fund, providing more return and a greater buffer against any future yield rises.

Empirical evidence suggests that bonds are often, but not always, negatively correlated to equities (i.e., they move in the opposite direction). It also suggests that markets work pretty well and trying to guess which asset class will do well this or next year is well-nigh impossible. As such, having the patience to stick with an investment strategy over the longer term is really important.

Press articles are often influenced by recency bias, which encourages investors to make portfolio decisions based on recent events. For example, it is easy with the benefit of hindsight to identify the assets that have done well in the last few years, commodities including gold, other metals and oil have done well. While we do not hold these explicitly you will benefit from the companies that are exposed to them – in 2022 your portfolio benefited from Global value stocks and its UK exposure, both of which are exposed to resource and energy. Holding these volatile assets directly or with a large weighting risks the downside of their material underperformance compared to the growth assets we use over the longer-term as shown by the graph below.

To include them in a portfolio, after a bout of strong short-term performance, fails the investment logic and empirical evidence tests.

When we see investment falls it can be easy to compare a flat or negative return in your investment portfolio to the increasing returns you can receive on deposit accounts.

It is certainly fair to say that the past five-year period has been tough for balanced portfolios, given that it included the global pandemic, the war in Ukraine, a rapid end to the era of low nominal and negative real interest rates, the highest inflation in 40 years in the UK, and a downturn in global equity markets in 2022.

Compare this to the 1970’s, which saw a decade of rampant inflation – up an alarming 240% cumulatively – from 1970 to 1979. Five-year, after-inflation returns for a balanced portfolio from 1970 to 1975 were, perhaps not surprisingly, negative. Yet investors who stuck with it during this very difficult period ended up with positive real returns after 15 years, increasing purchasing power by around 50%. Over the same period, holders of cash would have turned £100 into £85 of purchasing power. Investing remains a long-term game.

As an illustration the Financial Conduct Authority (FCA) has recently published rules which require platforms to provide a warning to pension clients who hold certain levels of cash or cash-like funds for a sustained period of time.

The FCA has noted that clients are at risk of having their savings eroded by inflation. The regulation states that if a customer is more than 5 years away from their pension age and holds more than 25% in cash or cash-like investments for a period of six months, the platform provider, must make them aware of this. The cash warning illustrates the effects of inflation on their long-term savings objectives.

The challenge that all investors face is that forecasting investment returns based on the information we have today is a highly challenging game to win consistently over the long term. If markets work, then prices effectively reflect the views of buyers and sellers of each company and their expectations for the future. Unexpected shocks, such as pandemics, wars, financial crises, and political turbulence are quickly factored into expectations, and prices adjust accordingly. Very few individuals possess the skill (or fortune) to anticipate such events and reposition their portfolio appropriately.

It is easy to say this here when you look at the flat or negative returns from your portfolio in the short term and the enticing promise of a deposit offering 5% or more for the next year. The key is the reason you are investing. For example, if the money is needed in the short term then keeping it on deposit makes sense but if you are investing for the longer term there is a real risk that your money may not keep pace with inflation. Investments also tend to move in a two steps forward one step back pattern and if you are out of the market when we see a large rise it can materially impact your long term returns.

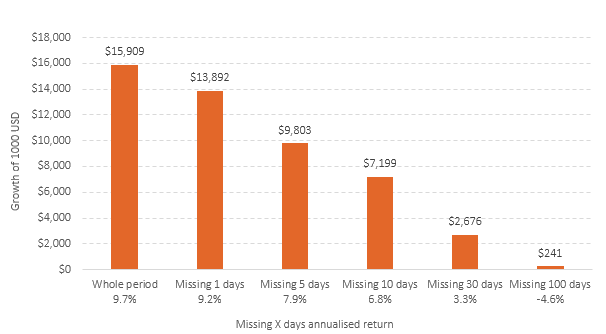

An analysis of missing the best days in the market from earlier this year (Albion, 2023) provides some food for thought, as the figure below illustrates.

Missing the best few days in the markets could be very costly

Source: Albion Strategic Consulting.

Data: Morningstar Direct © All rights reserved: SSgA SPDR ETF. Returns in USD. 23/01/1993 – 30/01/2023

Whilst these types of study imply a binary approach to being invested in equities or cash, which is a somewhat unreal scenario, it is evident that a few good days, weeks or months drive the bulk of market returns and missing them can be costly. Missing the best 30 days in this 30-year period would have only provided 17% ($2,676) of the rewards that the market delivered over the whole period ($15,909).

Remain focused on your long-term goals, stay invested and rebalance regularly, for a simpler life and the likelihood of better outcomes.