Investment basics

This is the first in a limited series of articles introducing the basics of investment and the construction of your portfolio.

11th March 2025

-

Gavin Jones See profile

Gavin Jones See profile

Most people today face the prospect of having to fund some or all of their retirement income from assets that they have accumulated over time. At its most basic, investing is a process of deferring spending in one stage of your life, often the time you are working, in order to build a pot from which you can draw funds to support your lifestyle choices at a time when your income from work decreases, perhaps as you move to part-time work or full retirement. Some investors have a range of goals for their money, such as funding university for their children or grandchildren, or simply building a nest egg for themselves or to pass on to future generations.

The first thing to remember is that any money put aside is vulnerable to inflation, i.e. the rise in consumer prices. Most people are now very aware of the damage that inflation can cause, having gone through the high inflation of 2022 and 2023. Let us look at a very simple, yet powerful example of how £100 has been reduced in value. The example is self-explanatory.

Pints of draught lager that £20 could buy

Source: UK RPI – average price draught lager – per pint

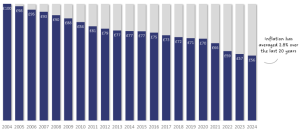

Looking a bit more specifically at inflation in the UK – as measured by the UK Consumer Price Index (UK CPI) – one can see in the figure below that the purchasing power of £100 has fallen quite materially in the past 20 years. Persistent, low levels of inflation can, over time, be as detrimental to your money as short bursts of high inflation.

Purchasing power of £100

Source: Bank of England UK CPI

Although 2.8% on average does not sound much, it’s the cumulative effect that is so damaging. The key message is that anyone putting money aside for the future and hoping that their pot of money will maintain its purchasing power will need to make sure that they take inflation into account.

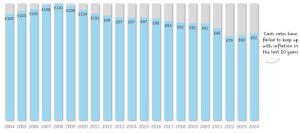

For those building a pot for retirement, protecting their wealth from inflation – and hopefully growing it after inflation value (this is sometimes referred to as its ‘real’ value) – is very important. The first thing to do is to become an investor, not a saver. For some, today’s elevated deposit rates returning above-inflation interest may look appealing. Unfortunately, cash has had a very poor track record of holding its ‘real’ value, as the figure below illustrates. Over the same twenty-year period, cash has lost around 20% of its purchasing power.

Purchasing power of £100 invested in cash

Source: Office of National Statistics UK CPI and SONIA interest rate benchmark

The next and very important basic insight is the power of compounding over time (i.e. interest on interest). When investing, small returns – and differences in returns – can grow into large differences in the value of your wealth. On the upside, these might be positive returns from an investment portfolio. On the downside, these may be from costs that you incur or from inflation.

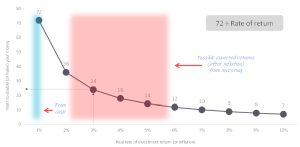

There is a rule of thumb called the ‘Rule of 72’ that you can use to see how quickly you will double your money based on the returns that you achieve, or alternatively how quickly the value of money will be halved by inflation. All you need to do is divide 72 by the rate of return, or inflation. So, a return of 3% will double your money in 24 years (72/3=24).

The Rule of 72 – how long it takes to double your spending power using after-inflation (real) returns.

Source: Albion Strategic Consulting © 2024

In the chart above, the red-coloured range indicates the level of returns for growth assets – of 2 to 6% above inflation or ‘real’ returns as they are known – on average, over the long-term that one might expect from a sensible investment portfolio.

Hopefully this note provides a useful high-level insight into some of the basic concepts that underpin the importance of investing rather than saving. The harsh reality is that for most people, keeping your money in cash is unlikely to be able to support the growth of their purchasing power both when accumulating assets and then creating an ongoing income from them. Understanding the head wind of inflation and how damaging it can be to purchasing power – particularly to those holding cash – and the need to invest and let compounding work its magic on small numbers over time, will stand you in good stead. In the next article we will look at how best to participate in the rewards of capitalism.