Keeping your investments on track: What the Investment Committee has been up to

Living and investing since President Trump’s inauguration at the beginning of last year has hopefully given some visibility and sense of value both to the investment philosophy we have as a firm and the role of our Investment Committee.

12th February 2026

-

Stuart Coombe See profile

The world has changed, but not your investment process

We have seen time and again over the years that our managed portfolios have been in place, that society and economies will adapt, and fear of investments can quickly pass as stock markets recover and go on to greater highs.

As an Old Mill investor, you will now be familiar with us telling you: to stay calm at times of market jitters; that we will rebalance your portfolio on a regular basis; that returns come from the markets; that costs really matter; that a sensible long-term, diversified portfolio structure is key and to avoid the temptation of looking at your portfolio too often!

A firm’s Investment Committee should be focused predominantly on the risks that have been taken in the portfolio, both at portfolio structure and at a fund level, rather than discussing whether now is the time to jump in or out of markets or which manager to hire and which to fire.

Your portfolio, as it stands today, should provide you with the comfort that it is robust and capable of dealing with the wide range of testing scenarios that could be thrown at it by the markets. The process of review by the Investment Committee is ongoing, and at the beginning of February, we had our latest meeting. The graphic below shows the steps the committee goes through when reviewing portfolios.

The work of the Investment Committee

Portfolio Performance and Peer Comparison

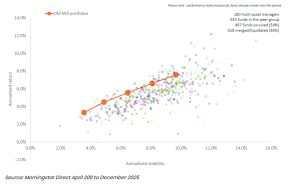

We undertook a review of portfolio performance and we shared returns for 2025 in the email we sent last month. Analysis is carried out by our investment consultants, Albion Strategic Consulting, who work with over 70 respected independent financial advice businesses around the UK, in Norway, Australia, the UAE and Hong Kong, who oversee around £23 billion of funds on behalf of their clients. They also looked at benchmarking Old Mill’s portfolios against our peers so we can assess how we are performing against similarly structured portfolios. The chart below shows the long-term performance of the portfolios against fund managers who are using a similar multi-asset approach.

Multi-asset fund manager comparison

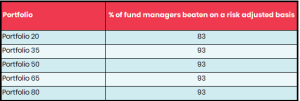

Old Mill’s portfolios are shown as orange dots on the chart and indicate a good relationship between the risk taken and the returns achieved. The long-term nature of investing shows that by taking the approach we have, over this period, we have outperformed a majority of firms taking a similar level of risk, as shown in the table below.

Asset allocation decisions

The committee spends a great deal of time considering the asset classes we have chosen to invest in rather than speculating over what may or may not happen politically and economically. In this way, we expect position portfolios to be able to deal with any future scenario.

Our asset allocations are based on sensible long-term decisions, and we will need compelling evidence to make changes to portfolios. We undertake a comprehensive review of our philosophy and process once a year, but with the world ever changing, we also consider asset classes and specific issues in depth as necessary at our quarterly meetings.

Other asset classes often come onto our radar as being worthy of consideration, and part of the role of the Investment Committee is to assess the suitability of these investments for inclusion in portfolios. Albion has concluded reviews recently on several alternative asset classes, including commercial property, cryptoassets, and private assets, to assess their suitability.

- Commercial Property: The committee agreed to retain commercial property in the portfolios as a diversifier, despite recent underperformance relative to equities and emerging markets.

- Cryptoassets, such as Bitcoin, remain excluded from portfolios due to their speculative nature, limited data history, and lack of robust products.

- Private Assets: Are also excluded, though they remain on our watch list. Private assets are investments in companies or debt that are not traded on public exchanges. Whilst there is a stronger investment rationale than crypto, as they are similar in nature to the assets we already use, due to complexity, oversight challenges, and the high dispersion of manager performance.

Fund selection as opposed to asset allocation is done more regularly, but here we adopt a market approach, so changes are only carried out if there is an obvious benefit to the client.

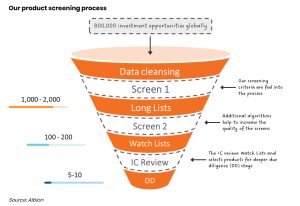

The graphic below illustrates the process to filter all of the available funds to those that provide the best value for our clients.

The screening criteria consider factors such as cost, track record, scale and the desirable attributes we look for in each asset class. Changes have largely been driven by cost in the last few years – we try to reduce investment costs for our clients where possible and have seen significant savings at a fund and platform level since we started.

Challenging the status quo

The Firm’s Investment Committee has one central question that drives its efforts: Does the investment approach adopted still represent best practice, based on the latest evidence and theory available to us? This is a big question and one which takes quite a lot of answering, as there are many layers to it.

One risk to any thesis is confirmation bias, where evidence is selected that fits, rather than challenges the thesis. An important point to note is that the overriding goal of the Investment Committee is to do what is in a client’s best interests, not to defend systematic, evidence-based investing as the only way to invest money, now and forevermore. The Committee is always open to the challenge of the status quo, but given the evidence supporting our investment approach remains highly compelling, any changes down the line are likely to be evolutionary, rather than revolutionary.

Behind the scenes, the Investment Committee works hard to ensure that portfolios remain robustly structured and therefore capable of delivering attractive long-term returns for investors using best-in-class funds.

What might the future hold?

As part of the ongoing process of challenge, there are a number of topics around which much thinking, discussion and ultimately decisions are required.

It takes fortitude and discipline not to chase ‘hot’ parts of the markets when their good performance is highlighted in the media (Bitcoin, gold, tech stocks, etc.) or to restructure the portfolio to take advantage of or avoid short-term opportunities and challenges (with the rise of AI being the latest ‘marmite’ theme).

The investment world is ever-changing, whether driven by politics, economics or technology, and therefore it is perhaps easy to see that the Investment Committee has some interesting and challenging issues to contend with in the future that may or may not slowly find their way into your portfolio.

If it ain’t broke, don’t fix it!’

Investment theory, academic research and a good dose of common sense provide the foundations for the hard work and discipline required to run a long-term, strategic and systematic approach to investing. We hope that with understanding and faith in your investment portfolio, you can withstand the noise from the media as well as the inevitable ups and downs of long-term investing.

It takes fortitude and discipline to stay calm and invested at times of market crisis, but doing so gives you the best chance of long-term investing success.

If you have any questions, your financial planner will be pleased to hear from you.