Live by performance, die by performance

On any piece of investment literature, the warning ‘Past performance is not a guide to future performance’ is often prominent, and generally glossed over by most readers. Yet all actively managed funds are sold specifically on their ‘great’ past performance, usually by comparison to their peers or a market benchmark. Those that perform poorly never get to see the light of day in adverts or best-buy lists. Many investors would be well advised to take heed of this warning. Those investing in a systematic way, seeking to capture market returns for market risks taken on, certainly do.

24th June 2022

-

Gavin Jones See profile

Gavin Jones See profile

Deep down in the investor psyche lurks a little demon that wants to get rich quick, suffers terrible pangs of FOMO (fear of missing out) and becomes blinded by the urge to jump on the runaway train of rampant performance despite the warning signs that flash as they clatter down the track ‘Past performance is not a guide to future performance…past performance is not a guide to future performance’.

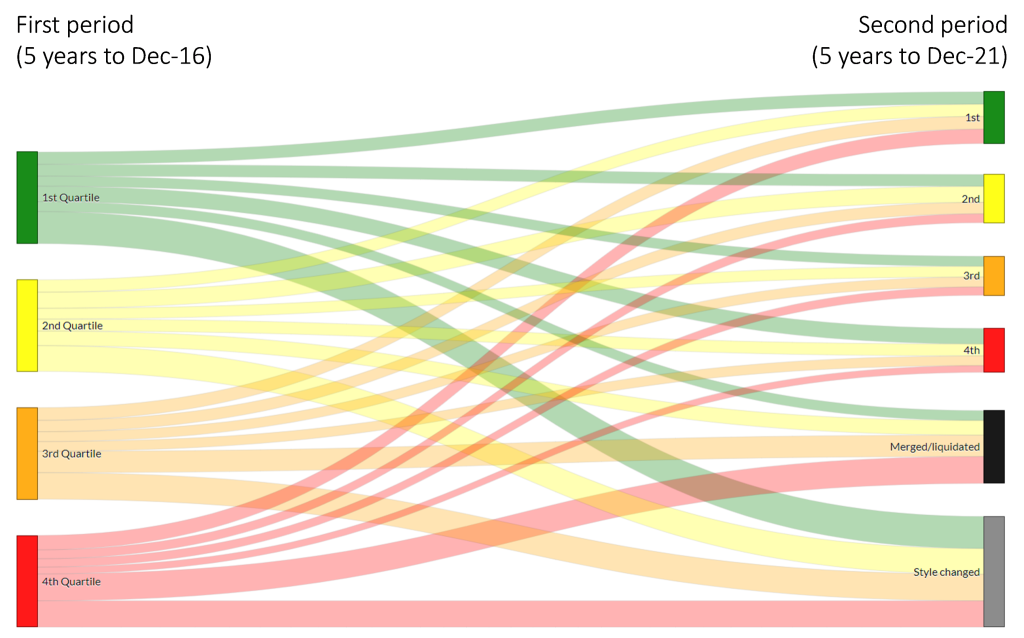

We know too, from experience, that often funds that outperform over the shorter-term are riding an investment style train, such as technology companies or growth stocks, that happen to be in favour at the time. Markets make managers. The harsh reality is that past performance does not tend to persist. This is clearly demonstrated in the chart below which shows that top performing managers (green) in one period – defined as top quartile (top 25%) in a rank of their peers – end up scattered randomly, as expected by chance, throughout the ranking over the subsequent period.

Figure 1: Past performance is not a guide to future performance

Source: Albion. Data: US Persistence Scorecard Year-end 2021 © All rights reserved.

A recent example of this in the UK was Neil Woodford, a fund manager heavily promoted by the likes of Hargreaves Lansdown that saw his fund suspended in 2019 hitting the savings of thousands of investors.

Taking a look at one of the funds that hit the headlines in 2020-1 with its stellar performance provides a sobering insight into the dangers of chasing performance. ARK Innovation – a highly concentrated, high risk, ‘disruptive innovation’ technology fund – had a stellar rise of over 214% from the start of 2020, in US dollar terms, to its peak on 12 February 2021. Its CEO Cathy Woods was a regular on US business TV shows, spawning an almost cult-like following. It hit a unit price high of $157 (up from US$50 on 1 Jan 2020), but has since then plummeted to US$37, losing 76% of its value (to 12 May 2022). Its return is now almost exactly in line with the broad US equity market for those invested over the entire period. If you live by performance, you die by performance. It is worth remembering that the worst fall in the UK equity market since 1900 was of a comparable magnitude (-73%) in 1973-4.

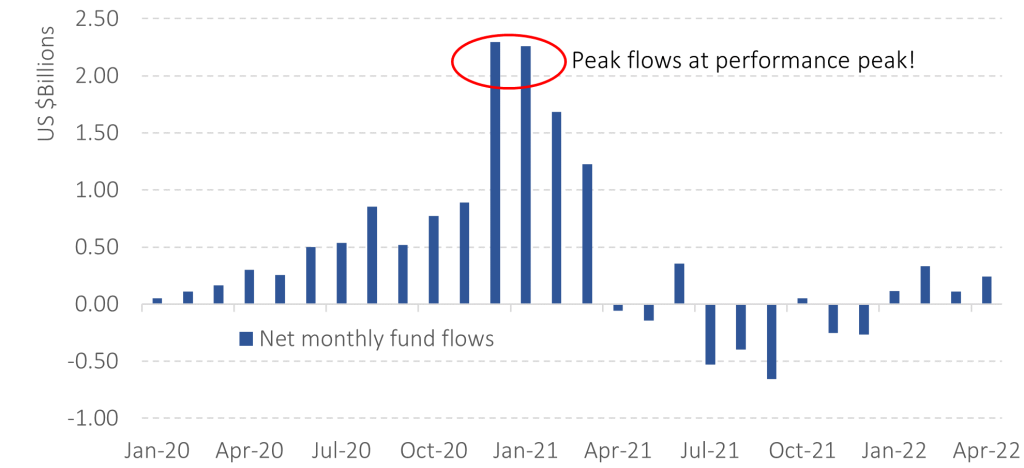

Unfortunately, performance chasing investors tend to come to the game late, as the chart below clearly shows. Net flows into the ARK fund peaked at the start of 2021, just as performance peaked. Assets gathered from investors in 2020 and 2021 represented around 90% of all net inflows since the fund’s inception in 2015[1]. That is not good news.

Figure 2: Bad timing decisions punish late arrivals – ARK fund (ARKK) net monthly flows

Source: ARKK net fund flows from Morningstar Direct © All rights reserved 2022.

It is evident that most investors failed to capture the strong upswing, piling in at the top and suffering the subsequent calamitous downturn. The average investor’s return is likely to be materially worse than the fund’s return, on account of this poor timing, although no exact data is yet available.

Investing is a hard enough emotional challenge at the best of times. Chasing performance just adds to the complexity and stress involved and may well put long-term investment goals at risk. Taking specific risk on such a fund is simply a gamble.

Next time you read a product factsheet or see an advert for a fund in the paper avoid the siren calls of stellar performance and take a moment to reflect on the free, sensible, and seemingly boring advice it is obliged to provide: ‘Past performance is not a guide to future performance’.

[1] Morningstar (2021) ARKK: An Object Lesson in How Not To Invest. Amy C. Arnott. https://www.morningstar.com/articles/1071658/arkk-an-object-lesson-in-how-not-to-invest Accessed: 11-05-2022