Looking backwards and forwards

15th January 2026

-

Stuart Coombe See profile

2025 was geopolitically a rollercoaster year, with conflict, old rivalries and a new US President intent on change. Yet despite this, investments largely finished the year higher than they began.

As the calendar turns, it is once again the season for bold predictions and confident outlooks. Experience suggests that such forecasts are best treated lightly. Markets incorporate known information very quickly, and prices only move meaningfully when something new and unexpected arrives. The future, by definition, is unpredictable. A sensible forecast for the year ahead, therefore remains unchanged: markets will go up, down or sideways.

Looking backwards

The past 12 months provided another vivid reminder of how quickly assumptions can be challenged and narratives rewritten.

Politically, 2025 was a year of striking upheaval. A new US administration set about reshaping domestic policy and foreign relations with remarkable speed and ambition. Trade policy proved a powerful source of stock market volatility. Announcements of sweeping tariffs triggered sharp and sudden market reactions, only for many of those measures to be softened, delayed or diluted as practical realities intervened. Markets, as they often do, adjusted quickly to both the shock and the subsequent reassessment.

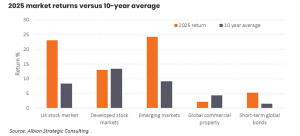

Stock markets rarely deliver returns close to their long‑term averages in any single year. In 2025, as you can see from the graph below, returns for 2025 (shown by the orange bars) were in line with 10-year averages (the dark bars) in some cases, and meaningfully above and below in others.

Artificial intelligence dominated headlines throughout the year. Vast sums were committed to AI infrastructure, chip manufacturing and model development, fuelling talk of a new industrial revolution. Company valuations, especially in the US stock market, reached eye‑watering levels and, for a time, optimism seemed boundless. Yet confidence, at times, proved fragile. The emergence of cheaper and more efficient AI models and underlying technology raised uncomfortable questions about competitive advantage and whether all that investment would ultimately translate into profits. This competition is a natural part of a capitalist world, and as such embedded in the risk and expected rewards of stock ownership.

US stock markets still did well, but holding other countries, the UK and especially emerging markets benefited your portfolio.

Beyond markets and technology, the world remained unsettled. A fragile ceasefire in Gaza held for much of the latter part of the year, offering some respite but little in the way of lasting resolution. The war in Ukraine continued, grinding on with terrible human cost and little decisive movement. Elsewhere, conflict intensified in parts of Africa, while tensions escalated episodically across parts of Asia. Natural disasters added further strain, with devastating earthquakes, wildfires, and extreme weather events affecting millions.

And yet, despite all this, the global economy proved more resilient than many had feared. Growth endured, employment held up better than expected, and some central banks were able to begin cautiously easing monetary policy by lowering interest rates. Markets, overall, delivered another reminder that they are forward‑looking, adaptive and often more robust than the prevailing mood suggests.

For diversified investors, 2025 reinforced some long‑standing lessons. Concentration in fashionable themes can magnify both gains and losses. Broad diversification across regions, sectors and styles remains one of the few defences that does not rely on foresight. High‑quality, shorter‑dated bonds continued to play their role as stabilisers, reminding us that their value lies not in excitement but in reliability. Long-term success lies in owning a broadly diversified and well-structured, evidence-based investment solution.

Looking forwards

Entering 2026, uncertainty remains abundant. It always does.

Being an investor can be emotionally challenging. After a run of positive years, it is entirely natural to worry that some of those gains may be given back. This is regularly a feature of a long-term investor’s journey. No guarantees exist, and it is for this reason that we should expect higher inflation plus returns from your investments.

Interest rates are generally lower than they were a year ago, but their future path is far from assured. Inflation has eased, but policymakers remain alert to the possibility of renewed pressures. Trade tensions, elections and geopolitical risks are ever‑present. None of this is new.

What is sometimes forgotten is that today’s prices already reflect tomorrow’s fears, hopes and expectations. Markets do not wait for events to happen; they move in anticipation of them. What will most likely matter in the year ahead are the surprises, not the scenarios that dominate the current debate.

Trying to position a portfolio for specific outcomes requires a belief that one can consistently outguess the collective wisdom of millions of other participants. The evidence suggests that very few can do this reliably – even the professionals struggle to do so, with the evidence showing the vast majority of fund managers failing to beat the benchmark they are targeting.

Acting on strong convictions about the near‑term direction of markets may feel comforting, but it carries the risk of being wrong twice: once when selling your investments, and again when deciding when to buy them back.

A word on the supposed AI bubble

Much has been written about whether the world is currently in an AI ‘bubble’. Some argue that valuations are detached from reality and that a reckoning is inevitable. Others insist that the technology will justify current prices and more. Both views may ultimately prove right in different ways and at different times.

In one view of markets, prices always reflect all known information, and what looks like excess is simply the rational pricing of uncertain future cash flows. In another, human behaviour and sentiment periodically push prices too far in either direction. In practice, these are just models, not truths.

The uncomfortable reality is that only with hindsight will anyone know whether the world is currently living through an AI bubble. By then, it will be too late to act on that knowledge.

The enduring lesson

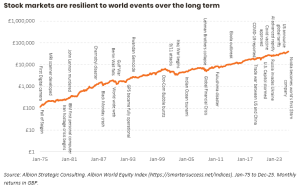

Market outcomes will be shaped by events that cannot be forecasted with confidence. Against this backdrop, the most robust response remains unchanged: maintain broad diversification, accept uncertainty as the price of long‑term returns, and remain disciplined when headlines are most unsettling. The graph below shows the growth of world stock markets through some of the events of the last 50 years.

When attention is focused on tough times, it may not be a bad idea to spend time away from headlines altogether, or search for coverage from outlets focused on positive world events and human progress[1].

From an investing perspective, as ever, we remain hopeful for the best in 2026 but remain prepared for the worst. Your financial planner will help to ensure you stay invested, stay diversified, and continue to stay focused on long‑term goals, rather than short‑term noise.

[1] For example, Good News, Inspiring, Positive Stories – Good News Network