Market commentary

High inflation in 2022 led to a rapid rise in interest rates around the world, contributing, in part, to the fall in global bond and equity prices.

2023 has delivered a much more positive story and all core assets delivered positive returns but it was a very volatile year.

The US market contributed the lion’s share of returns – and in particular the ‘Magnificent Seven’ as the press have dubbed the big tech firms – regained the losses they suffered in 2022. In fact, they contributed around three quarters of the return of the US market over the year. As a consequence, global developed market returns were very strong, given that the US weight in global markets is around 63%.

On the defensive side of portfolios, high quality, short-dated bonds have recouped over half of the falls suffered in 2022 – largely on account of the higher bond yields, which caused the pain in 2022 – delivering returns similar to cash.

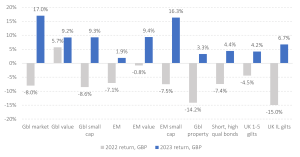

In the graph below we compare asset returns for last year compared to the year before.

10th January 2024

-

Gavin Jones See profile

Gavin Jones See profile

In the graph below we compare asset returns for last year compared to the year before.

Data: Morningstar

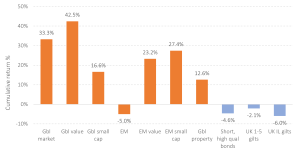

We talk about remaining invested and the long-term benefits from investing but we know it can be hard to do this. The graph below shows three-year cumulative returns to illustrate the benefit of remaining invested through tough years such as 2022.

Bond returns over this period have been poor due to low starting yields around 0% due to the Covid crisis followed by subsequent yield rises (and thus bond price falls), but these were more than compensated for by strong growth asset returns.

Data: Morningstar

You only need to look at the news to see uncertainty abounds. It is important to remember that forward-looking views are already reflected in today’s prices. What comes next, no-one truly knows. The key is to remain highly diversified, resolute in the face of any market setbacks and focused on long-term goals. We have set out some of the key issues that will impact on market returns.

Rishi Sunak has announced that the UK election will be in the second half of the year.

The Chancellor has set the date of the Spring Budget for 6 March and in an election year there has already been speculation, in particular about an Income Tax cut ahead of the general election.

European Parliament elections will be held at the beginning of June.

The European Central Bank will be watched closely as the first major economy to be predicted to reduce interest rates, possibly as early as the first quarter. As we know from last year, central banks are still suggesting that interest rates will have to remain higher than we expect in order to ensure inflation remains under control.

US Presidential elections will be on 5 November. Expect this to dominate the news through much of the year.

While the US economy is still strong, there is the expectation that the rapid rise of interest rates may still cause a recession in the US. Something which President Biden will want to avoid.

Eyes are on the Chinese as the major economy in the emerging markets.

This month there will also be scrutiny on the Taiwanese election in the light of their fractious relationship with China.

There are also elections in India which will end in June.

Defensive assets have played a strong part of portfolio returns in 2023. We expect more of the same as higher yields and the prospective of interest rate cuts in many developed countries is on the cards.

Central banks are still saying that they are not in a rush to cut interest rates, watching inflation figures closely.