Market commentary

Inflation remains a major concern around much of the western world.

6th September 2022

-

Gavin Jones See profile

Gavin Jones See profile

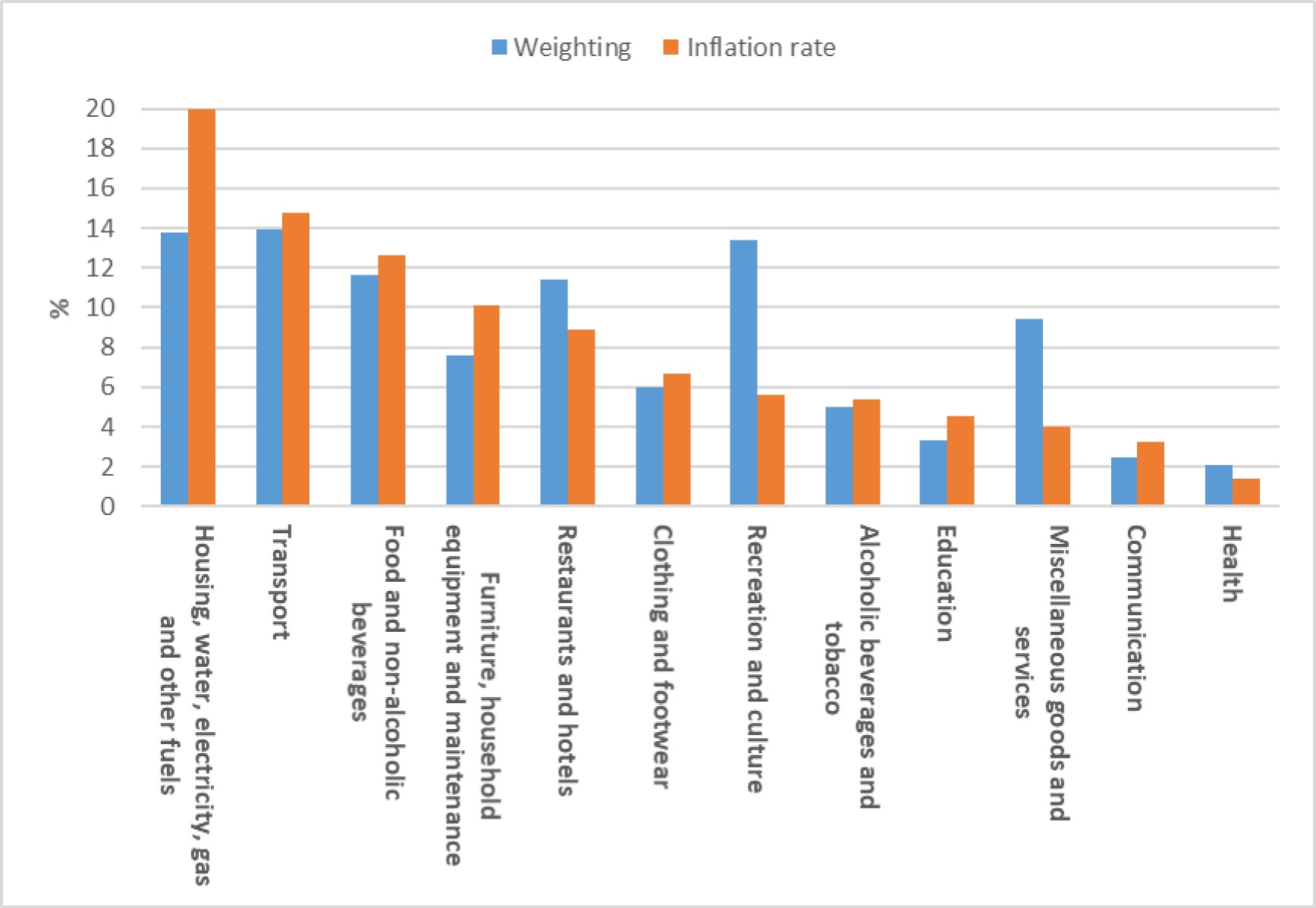

In the UK, inflation as measured by the Consumer Prices Index (CPI) reached 10.1% in July 2022; a year earlier it had been 2.0%.

The graph below shows the breakdown of the CPI basket and an indication of July inflation for each of these constituents. The Housing, water, electricity, gas and other fuels division of the CPI has a weighting of 13.8%. Of this 3.5% – about a quarter – is the electricity, gas and miscellaneous fuels category. That may seem a small part of the total but with sharp inflation in this category, it will have a big impact on the overall annual inflation amount.

Source: ONS July 2022 data

Newspaper headlines in August reported that Citigroup calculations suggest inflation will peak at 18.4% in January, over 5% above the Bank of England’s forecast earlier in the month of ‘just over 13%’ in the final quarter of 2022. ln the Citigroup inflation calculation the gas increases contribute over 9% to annual CPI on its own. The Bank of England figures were published on 4 August, so would have used late July data. Since then, gas and electricity prices have surged.

Whilst the impact of gas prices is material with the July 2022 annual increase in the electricity, gas and miscellaneous fuels category at 69.1%, if you strip out the household energy category from the July 2022 CPI number, inflation from the rest of the economy is still running at 7.7%.

In the Eurozone, the corresponding figures were inflation of 8.9% in July and 2.2% a year earlier.

European economies face a similar challenge to the UK as needing to import much of their energy from elsewhere. The reductions of Russian gas supply to Germany and latterly France has caused sharp increases in gas prices.

The end of August saw a change in monetary policy outlook across in Europe. Some individuals at the European Central Bank are now openly discussing the idea of hiking interest rates by 0.75% at the meeting in September to try and control inflation. The governor of Austria’s central bank said that a 0.75% move “should be part of the debate”, and that a 0.50% move in the meeting was “the minimum for me”.

The US saw the annual inflation rate fall to 8.5% in July from 8.9% in June. The rate a year ago was 5.4%.

The Chair of the federal reserve, Jerome Powell used his speech in August at the Kansas City Fed’s annual policy forum to reiterate that the US central bank would keep raising rates and probably leave them elevated for a while to reduce inflation. Markets had been reducing expectations of interest rates rises in the US after inflation there fell from 8.9% to 8.5% in July raising hopes that it had reached a peak. The speech reversed much of this so expectations for interest rate hikes in the US rose, with equity markets selling off in the aftermath.

While Chinese Inflation in July rose to 2.7% with the rate a year ago 1%, it remains low compared to some of the inflation rates we are seeing in the US and Europe.

In contrast to the economies in the western world where Covid restrictions have largely been lifted, China continues to face rolling lockdowns because of the country’s zero-Covid policy and this is negatively impacting on economic growth.

In the wider emerging economies inflation has been more of an issue. These economies are seeing less of an Impact because of energy prices, but with food making up a bigger proportion of their CPI baskets, food price increases are having a big effect.

With the further expectation of interest rate rises there has been some further falls in the prices for defensive assets since the last Insight. The fall has been greater in the Index Linked Gilt fund due to the longer duration of the underlying assets. The Global high quality bond fund has shorter dated assets and these are less volatile and help to reduce falls when yields are rising.

Both funds are now sitting with higher yields and we expect this to help recoup, over time, the losses we have seen more recently.

Please speak to your financial planner if you want to discuss your portfolio.