Market commentary

In writing this Insight, we have been faced with the challenge of a fast-moving economic environment. Much of the content is written in the days before it is sent to you. We saw remarkable actions last week from a political and market point of view and at the time of writing, market reaction continues as the implications of a U-turn on one of the pillars of the Government’s proposed mini-budget is still being digested.

6th October 2022

-

Gavin Jones See profile

Gavin Jones See profile

The FTSE100 stock market index has help up in the past year, supported by large holdings in sectors such as energy and low holdings in technology, combined with the fact that a majority of earning for these companies are from overseas, benefitting to some degree from these exchange rate movements. More domestically focused companies, however, such as those found in the FTSE250 index have faired less well – hampered by higher production costs, including energy and reducing sales to squeezed UK consumers and companies.

There has been a noticeable impact in exchange rates with sterling seeing short term gains on Monday. The abolition of the 45p tax cut was only expected to cost £2-3bn, a small sum compared to the national insurance reversal or cut to basic rate tax.

The outlook for the European economy remains challenging. Rising electricity prices are hurting European manufacturing, with some heavy energy-consuming businesses such as steel, chemical, and fertilizer manufacturing announcing plans to shut down temporarily some of their operations, warning that high costs are denting competitiveness.

Now that the Nord Stream 1 pipeline is ‘indefinitely’ shut down, further energy supply disruptions are in the offing although with gas storage in the EU almost full before the winter starts, it is currently being viewed as uncomfortable rather than disastrous for the economies of EU countries.

Showing how quickly sentiment can change, we have moved from a situation in August where many investors were hoping for the federal reserve to start signalling that inflation, and therefore interest rate rises may be approaching a peak. Fast forward to September and the Fed has unequivocally said that they do not see interest rates falling until 2024, with further rises expected into next year, although they are currently predicted to stop in Q1 2023.

The Fed’s economic projections still show remarkable resilience in the overall economy, suggesting that inflation may stay high. Their predictions are pointing towards 2025 before inflation in the US gets back to the 2% target.

While inflation is forcing much of the world to increase interest rates, China is on a different path with The People’s Bank of China unexpectedly cutting interest rates for the third time this year in late August. Growth in the country continues to slow amid a property downturn, Covid lockdowns and lower consumer spending. Weaker overseas demand from pressures of rising costs of living in many western economies are also expected to weigh on exports and the Chinese economic outlook.

Reviving growth has become a top priority, and Chinese policymakers, with domestic inflation currently below 3 percent may well make additional rate cuts in China in the near future.

This forecast of rate cuts and the soft economic outlook may cause the Chinese currency to weaken further against the dollar although this is not unique to China with most of the world’s economies, both developed and emerging seeing weakening currency against the strong dollar. With much of the world’s commodities priced in dollars the cost of raw materials have gone up for manufacturers and while exports become competitive it has affected most emerging countries so competition has increased. Beyond China, those countries that have debt in dollars are seeing those loans become more expensive.

Investors’ portfolio structures are put under the spotlight at times of market downturns, and this has certainly been the case for bond investments in 2022.

As we wrote earlier in the year, rapidly increasing inflation and interest rates present particular challenges for the assets making up the defensive element of investment portfolios.

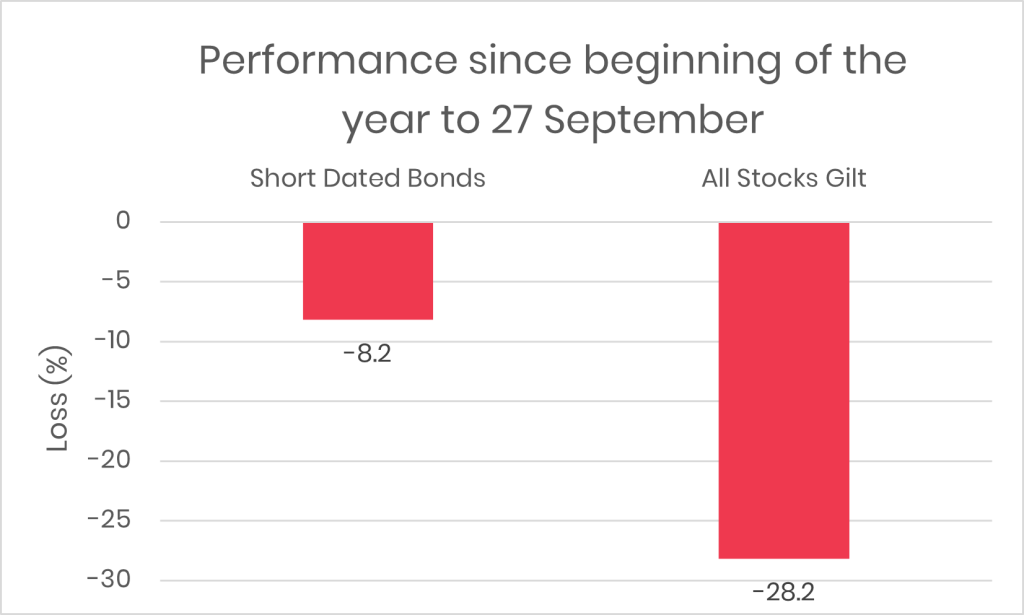

These challenges have been helped by the short duration nature of the main defensive fund we hold, aided by its diversification across different countries. Despite short term falls, the future looks brighter, helped by the transition to higher yields providing additional returns for these funds in the future. The shorter dated, high-quality bonds we hold have performed relatively well compared to the bond market as a whole and will provide the benefit of higher yields on the fund in the future. The defensive nature of the short-dated bonds we use compared to longer dated bonds can be seen from the following chart.

Our index linked fund has been more volatile albeit with a maximum exposure of no more than 10% in portfolios. This fund was positively impacted by the Government intervention and saw some big up swings in value last week.

Please speak to your financial planner if you want to discuss your portfolio.