Performance of the Old Mill Portfolios

At present, it would be fair to say that it is more difficult than usual to predict what will happen to economies over the next few years. Over just the last month for example, economic markets have become less concerned about inflation and more concerned with the risks of recession taking more of a lead role.

Goldman Sachs’s economists currently ascribe a 45% probability to the UK entering a recession within the next 12 months, a higher probability than for Europe and the US which are 40% and 30% respectively. Remember that stock markets are forward looking and these statistics will already be priced in to share prices.

20th July 2022

-

Gavin Jones See profile

Gavin Jones See profile

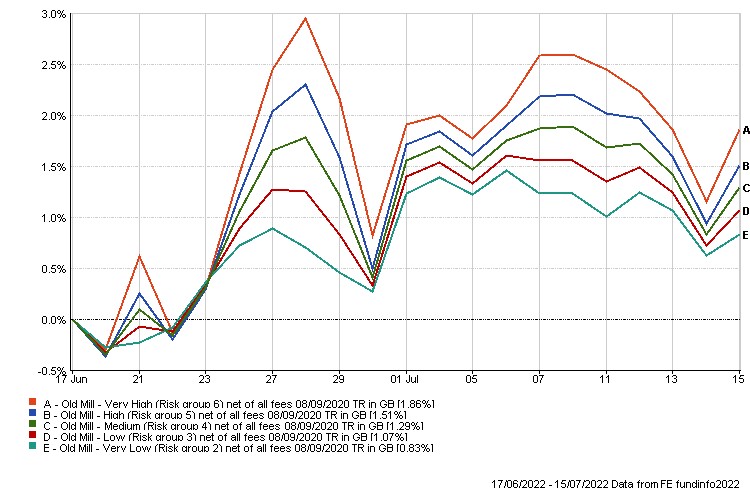

Performance since the last insight (from Friday 17 June 2022 to Friday 15 July 2022)

Perhaps surprisingly given the amount of bad news about, portfolios all rose over the period as global equities and bonds reversed the falls from the beginning of June.

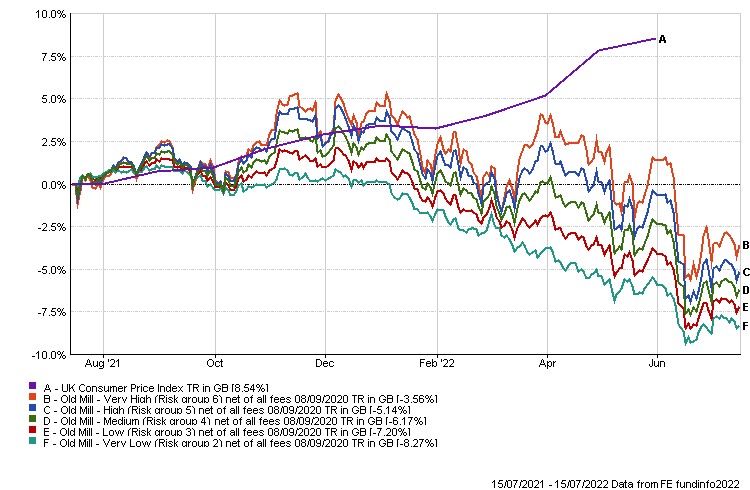

Performance over the last year (up to Friday 15 July 2022)

We have seen falls in all portfolios over the last year in the face of global economic and political turmoil and rising inflation.

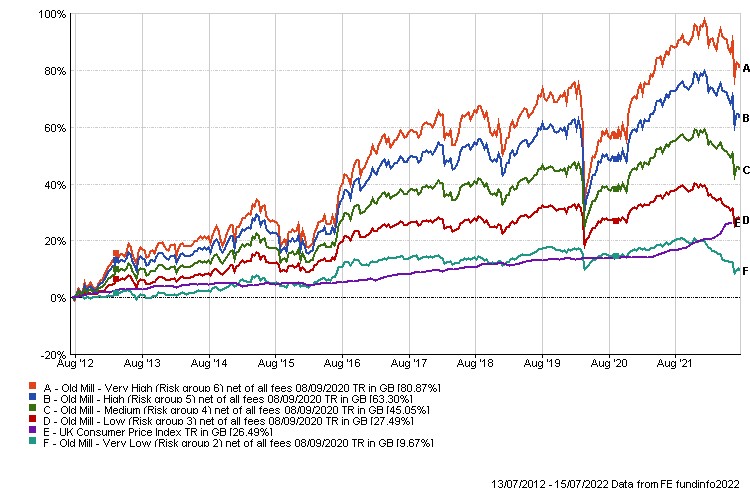

10-year performance (up to Friday 15 July 2022)

Investing remains a long term pursuit and while we can look at short term performance to explain what you are experiencing, we hope you take reassurance from the longer term, 10 year results.

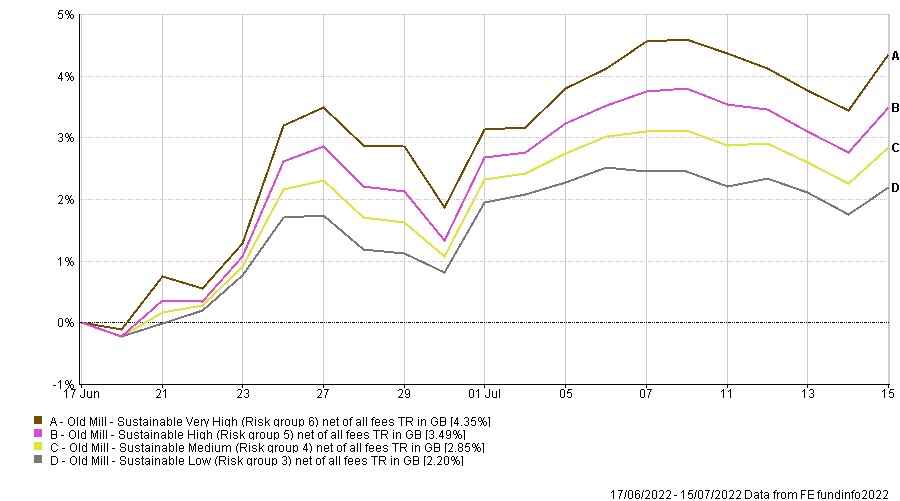

Performance since the last insight (from Friday 17 June 2022 to Friday 15 July 2022)

Sustainable portfolios saw a good recovery over the period with international stocks which forms a greater percentage of the sustainable portfolios (30%) than in the standard portfolios (20%) seeing good rises.

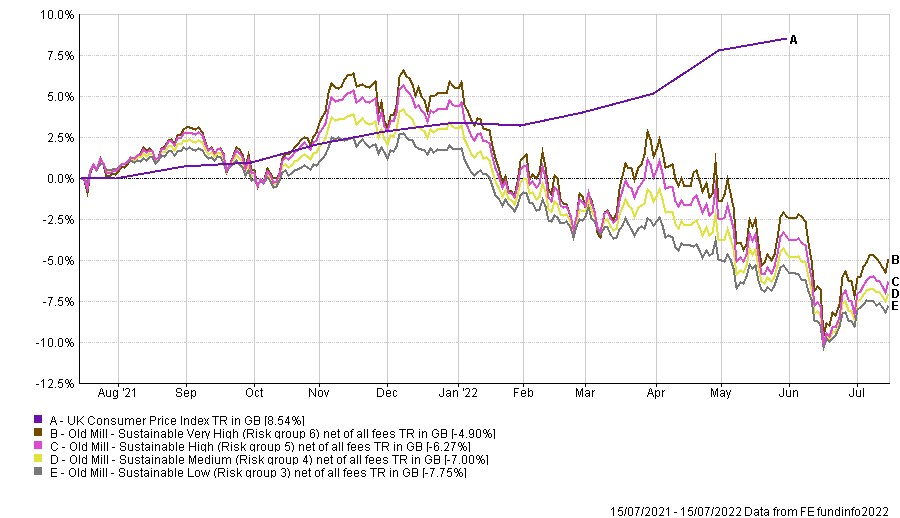

Performance over the last year (up to Friday 15 July 2022)

Investments in the sustainable portfolios exclude a number of industries to reduce the exposure to carbon emissions. One of the impacts of this over the year has been little or no exposure to energy industries such as oil and gas which have seen strong performance in the face of the Ukraine war. The impact of this was seeing sharper falls since the beginning of the year. There has been some recovery since mid-June and portfolios have recovered some returns.

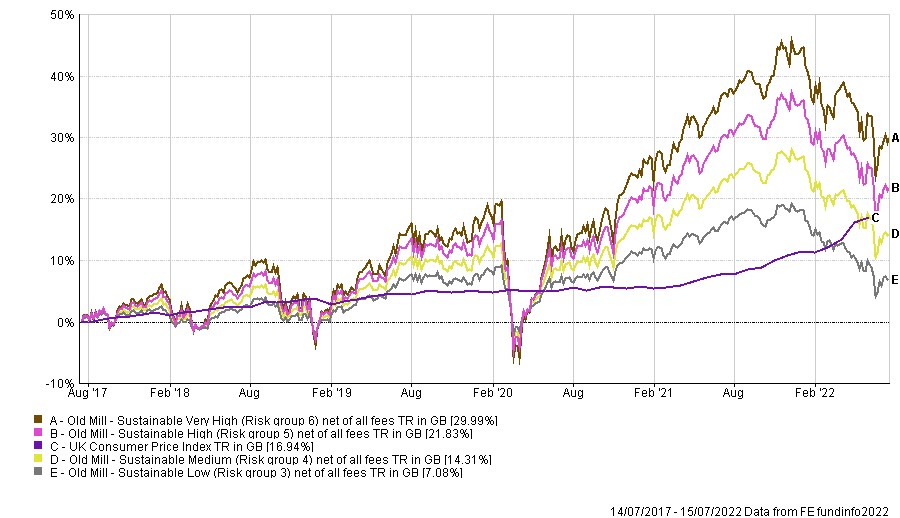

Longer term performance (up to Friday 15 July 2022)

As the sustainable portfolios have only been available for the last five years this is a shorter timeframe but still showing the potential upside over longer periods.

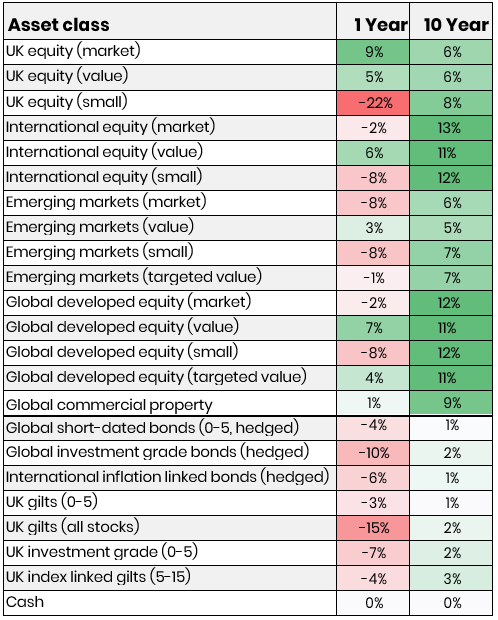

The table below shows the performance of a number of asset classes for the last year and over the last ten years as at close of play on Friday 1 July.

Looking at the underlying asset classes this reinforces the short term pressure investments have been under for the last year but also the higher returns available over longer time periods.