Performance of the Old Mill Portfolios

9th February 2023

-

Gavin Jones See profile

Gavin Jones See profile

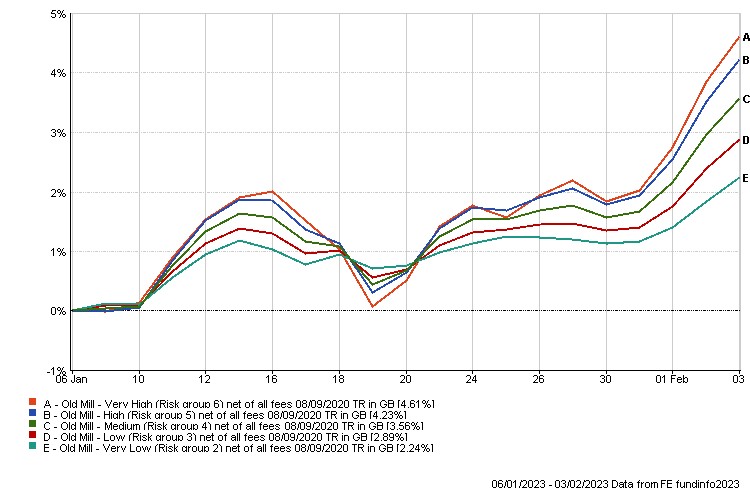

Performance since the last insight (from Friday 6 January 2023 to Friday 3 February 2023)

January was largely positive as markets see inflation as possibly reaching a peak and an end to the cycle of interest rate rises this year. Recession is likely across much of the developed world in 2023 but this is already priced into assets.

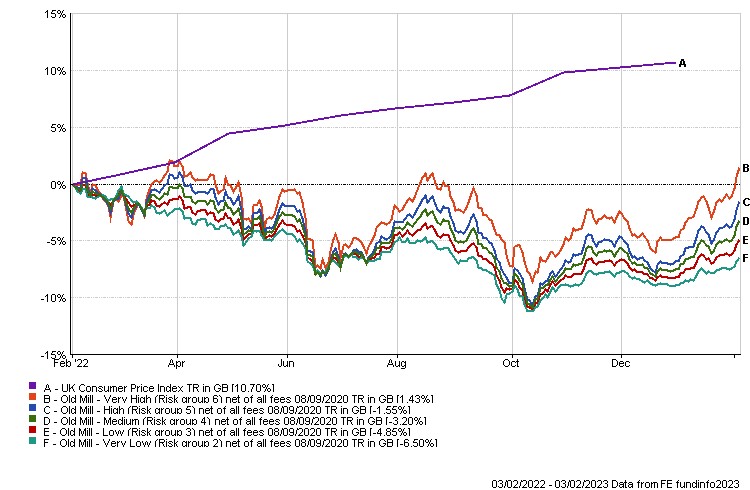

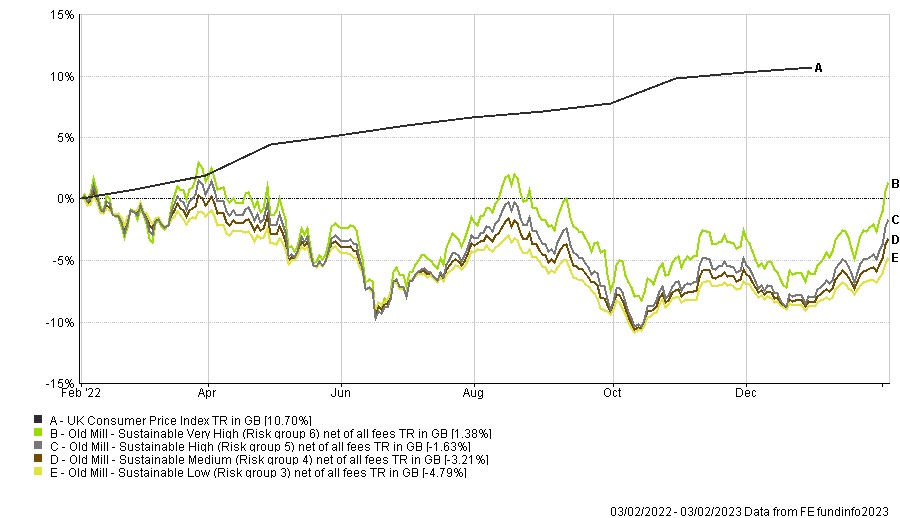

Performance over the last year (up to Friday 3 February 2023)

The graph shows sharp falls in assets until October 2022 as the impact of rising interest rates had a negative impact on both growth and defensive assets. Portfolios have been recovering since, with higher risk portfolios seeing a bounce back as markets once again sense that a peak in inflation and therefore interest rate rises is near. In the UK the main stock market index – the FTSE100 has reached a record high, as many of the global companies that make up the index are with sectors that have done well in the last year: in particular Energy and Financials.

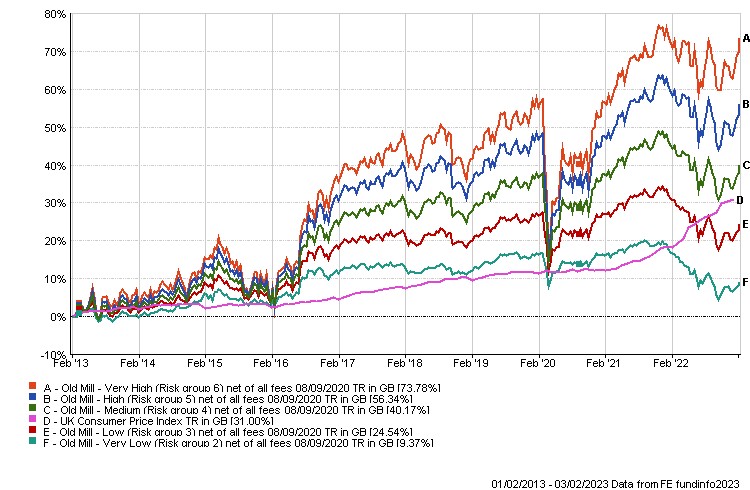

Longer term performance of standard portfolios (up to Friday 3 February 2023)

Investing remains a longer-term pursuit and taking a look at the ten year graph to the beginning of February, the portfolios are showing a more robust picture.

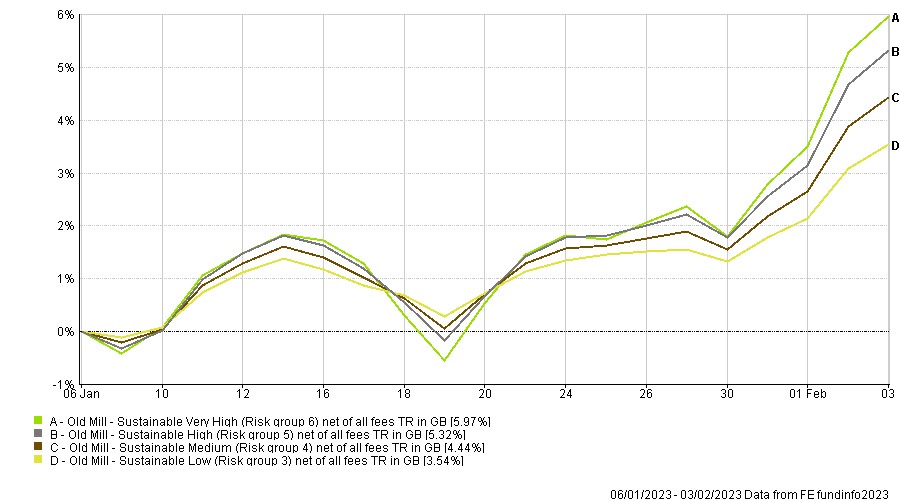

Sustainable portfolios performance since the last insight (from Friday 6 January 2023 to Friday 3 February 2023)

Sustainable portfolios, have seen greater growth since the beginning of the year. Hopes of moderating inflation, in particular in the US has led to a sharp rebound in those markets. As the sustainability portfolios have a higher exposure to the US so have benefited from this.

Sustainable portfolio performance over the last year (up to Friday 3 February 2023)

Over the year, the path of sustainable portfolios with little exposure to the oil and gas sector, which has been one to the top performers, has been different to the standard portfolios but over the year performance has been similar.

Longer term performance of Sustainable portfolios (up to Friday 3 February 2023)

As the sustainable portfolios have only been available for the last five years this is a shorter timeframe but still showing the potential upside over longer periods.

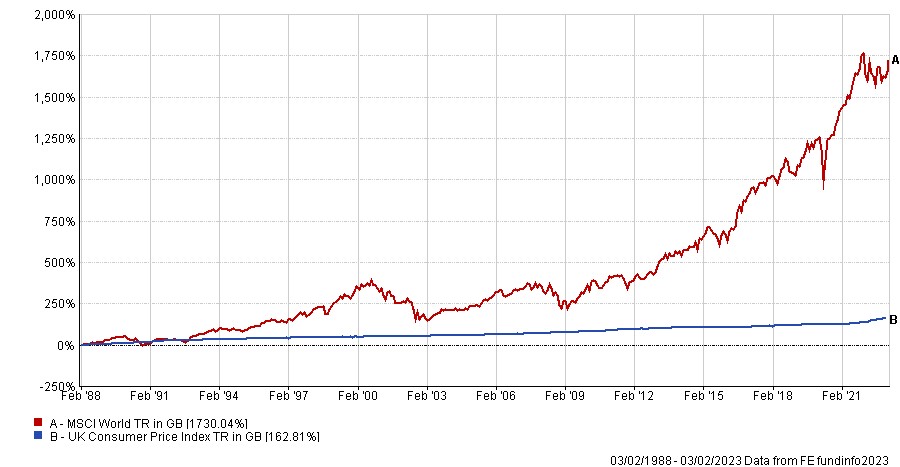

In the short-term, inflation has risen against portfolio performance but taking a longer term view, and investing into assets that can provide protection against inflation – assets such as equites can grow your wealth in real (after inflation) terms.

The graph below shows the long-term performance of world equities, shown by the MSCI World index against UK Consumer Price Index inflation over the last 35 years. Over longer periods you can see that equities have the potential for returns that grow the value of your investments in excess of inflation.

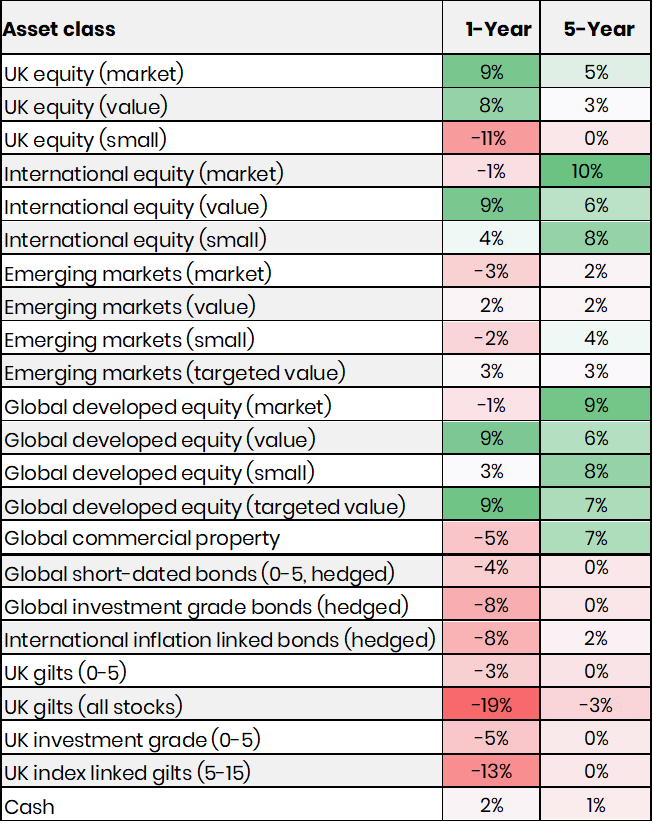

Below shows the performance of a number of asset classes for the last year and over five years as at close of play on Wednesday 25 January 2023.

The left-hand column shows the movement of assets over the last year and while there have been lots of falling values, there are a number of bright spots with value companies and UK equities providing useful diversification for portfolios. Over five years there are strong returns for most growth assets but with sharp falls this year, the longer term picture for defensive assets is flat. This does mask the necessary job defensive assets usually play in protecting assets when stock markets are falling.

Much of the defensive assets in portfolios is made of from high quality, short-dated bonds. The increased yield of this fund, currently over 4% should help make back the fall in capital over the next few years. In practice recovery could be quicker due to the rebalancing process in portfolios, where we bought more defensive assets at low prices in September. In addition, any expectation of falling interest rates will mean be could also see a rise in capital values.