Performance of the Old Mill Portfolios – up to Friday 5 November

Portfolios saw some recovery in October. As we have covered in previous Insights, the current market downturn has been different for several reasons, but in particular the performance of the UK market and the performance of the defensive assets in our portfolios.

10th November 2022

-

Gavin Jones See profile

Gavin Jones See profile

The media often use the FTSE 100 index as a measure of what is happening in the UK stock market although this should not be taken as a guide as to what is happening to your own investments.

Due to its exposure to sectors that have fared well in the last few years; Energy and Finance in particular, the FTSE 100 has held up well over the course of the last year. While there is exposure to the UK stock market in the growth assets held in your portfolio, it is only a part of the mix. Also included are global developed market equities and global property which have fared less well over the last year.

Investment remains a long-term pursuit and it is this diversification in portfolios – across companies, sectors, geography and asset class that will ultimately help to drive growth in the future. Different assets, sectors or countries that we have chosen to include in your portfolio will perform differently at different times, but without that crystal ball to tell us which to be in and which to avoid, we hold them all.

Recognising that equities can be volatile at times, we include defensive assets in your portfolio to protect against stock market falls. Since the end of last year in the face of rapidly rising inflation and interest rates and particularly here in the UK, we have seen bond yields rise and as a consequence this has caused bond prices to fall which has negatively impacted on the short-term performance of lower risk assets. A bond’s yield is calculated using the bond’s current market price compared to the fixed interest rate it pays. For example, a bond that pays a fixed interest rate of 4p and has a price of £1 has a yield of 4%.

The recent rise in interest rates has seen a rise in bond yields for the fixed rate investments held in portfolios but in the short term, this has come at the cost of a fall in bond prices. The good news, however, is that much of the loss in value experienced recently will be recovered fairly quickly by the higher yields now being earned on the bond investments. Once the fall in bond prices has been recovered, portfolios will then benefit from investments that are now yielding considerably more than they were before interest rates started to rise.

If we consider the Global Short Dated Bond fund which broadly speaking was yielding about 1% a year ago and this has risen to 4% at the time of writing. Over that period the capital has fallen by about 9%. So, with the additional yield of 3%, this should take about three years to make up the capital loss. But in practice we also rebalanced portfolios in September, so will have bought more of the fund with these higher yields and the break-even period will be shorter. If expectations of future interest rates fall, then we may also see some increase in the capital value of the fund as yields fall.

The news is full of doom and gloom at the moment and predictions of how it may get worse are not terribly encouraging. The people who trade in the stock market will also be reading the same news and analysing how it may affect companies and securities. Bad news may make a particular company less attractive and the price falls as people want to sell. Conversely if the future for a particular sector is bright then more people may be buying. Across the world this is happening all the time, and this is ‘the market’. With tens of thousands of market participants, the price of any stock is a good indication of all the news – both good and bad taking into account economic forecasts.

Therefore, when the news says there may be a recession around the corner this will not be a surprise to ‘the market’. This will already be in the price of each company. The same goes for our defensive assets. Yields now incorporate an estimate of all the anticipated rises in interest rates in the foreseeable future. The current Bank of England prediction is that base rate will rise to 4.75% before falling back.

These estimates may not be entirely accurate, but it means when interest rates rise, as they did last week, there is not a further increase in yield and fall in price for defensive assets as it is all in the price already.

Historically stock market falls happen before recessions, but once they happen ‘the market’ is looking into the future again, to recovery. Rises and falls in markets are due to new news, good and bad that changes this collective assessment of the future. We cannot control this future, but we structure portfolios to give you the best possible chance of growing your wealth from investments over time.

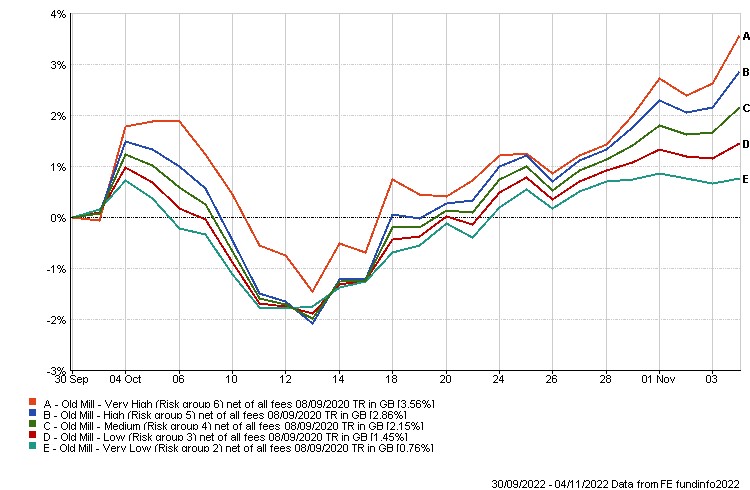

Performance since the last insight (from Friday 30 September 2022 to Friday 4 November 2022)

Political events in the UK saw sharp falls in Government Gilts caused by the high levels of potentially unfunded borrowing in the ‘growth plan’ at the end of September. Confidence started to come back as first Kwasi Kwarteng and then Liz Truss resigned. All portfolios saw positive returns over the last month.

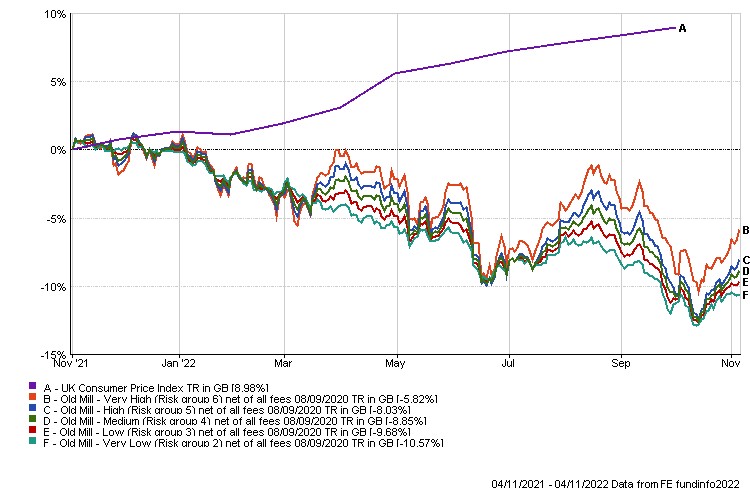

Performance over the last year (up to Friday 4 November 2022)

We have seen falls in all portfolios over the last year in the face of global economic and political turmoil and rising inflation. The graph over this period is reversed to what we would usually see – with lower risk portfolios falling more than higher risk ones. But these portfolios will be benefiting more from higher yields in defensive parts of portfolios as we described earlier in the article, and we should start to see this feed through into improved performance in time.

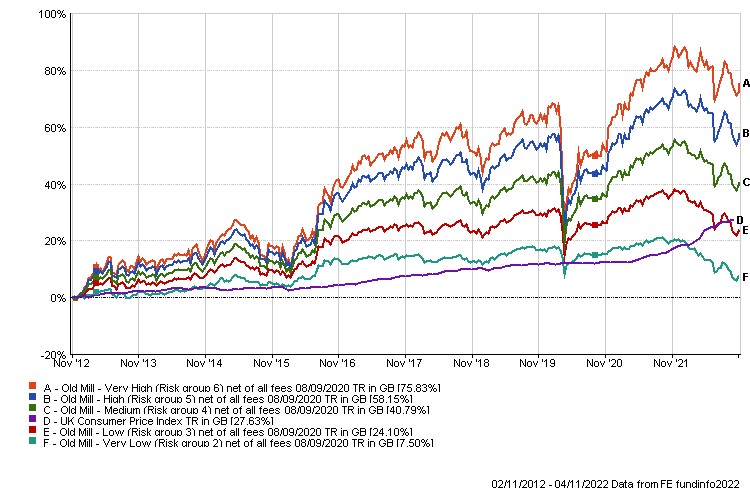

Ten-year performance of standard portfolios (up to Friday 4 November 2022)

Investing is a long-term pursuit and although some of the longer-term performances of lower risk portfolios reflect the transition to a potentially higher inflation environment, we hope you take reassurance from the longer-term results with the ten-year performance to Friday 4 November shown above.

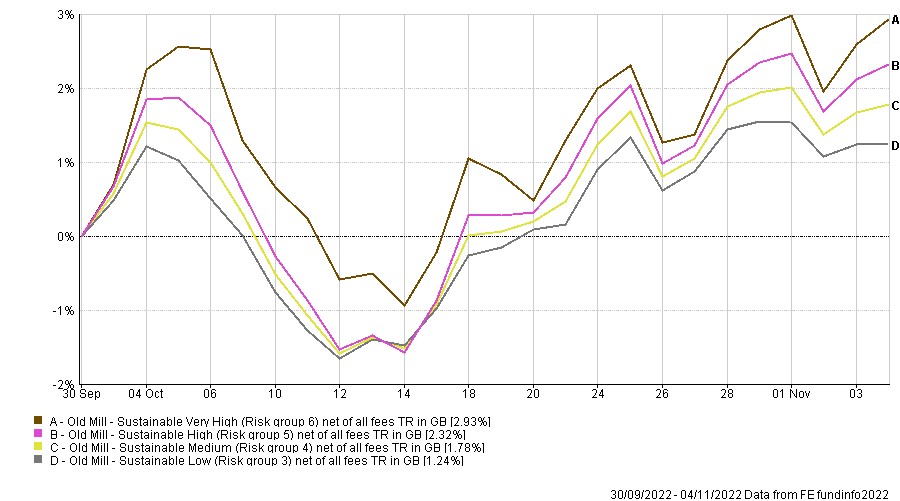

Sustainable portfolios performance since the last insight (from Friday 30 September 2022 to Friday 4 November 2022)

Sustainable portfolios rose over the period with returns over the period similar to our standard portfolios.

Performance over the last year (up to Friday 4 November 2022)

Investments in the sustainable portfolios exclude a number of industries to reduce the exposure to carbon emissions. One of the impacts of this over the year has been little or no exposure to energy industries such as oil and gas which have seen strong performance in the face of the Ukraine war. The impact of this was seeing slightly bigger falls since the beginning of this year than in our standard portfolios.

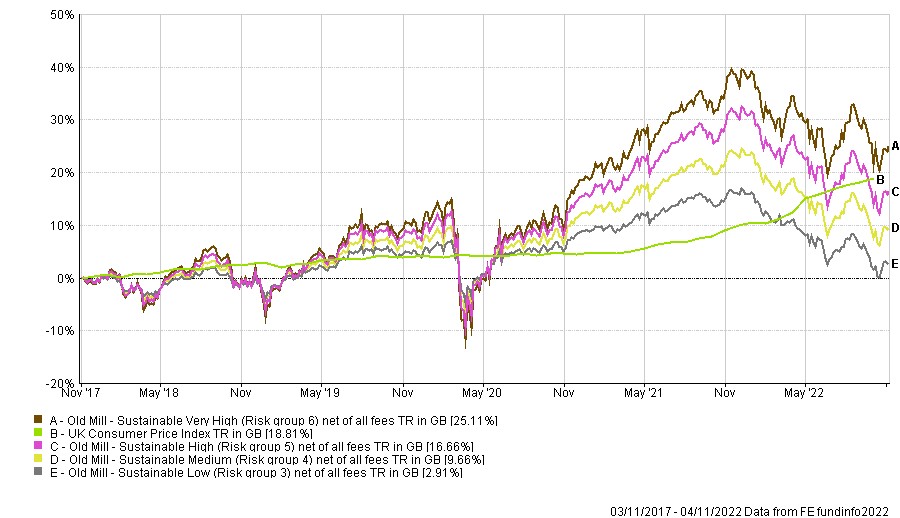

Five-year performance of Sustainable portfolios (up to Friday 4 November 2022)

As the sustainable portfolios have only been available for the last five years this is a shorter timeframe but still showing the potential upside over longer periods.

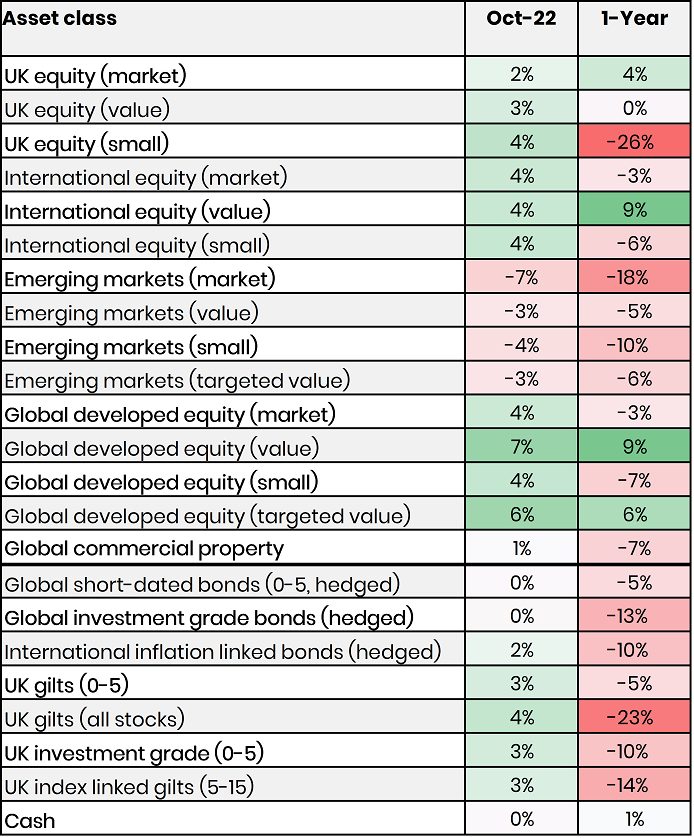

Below shows the performance of a number of asset classes for the month of October and over the last year as at close of play on Friday 28 October.

Looking at the underlying asset classes this shows the green shoots of recovery in most asset classes in October but reinforces the short-term pressure investments have been under for the last year.