Portfolio changes

An important role of the Old Mill Investment Committee is to continually review our approach to investing and the positioning of the portfolios to ensure they deliver a positive and robust investment experience.

We shared our thoughts earlier in the year on areas where we have been reviewing the portfolios and as a consequence, we have decided to make the changes at the annual rebalance in September.

The sustainable portfolios are being looked at separately as the existing growth assets already incorporate several of the proposed changes and there are several new funds we are reviewing. We will update investors in those portfolios once this has been concluded.

11th August 2023

-

Gavin Jones See profile

Gavin Jones See profile

While we are making several changes, when it comes to the expected returns on portfolios, the evidence remains the same that risk and return are related.

When constructing an investment portfolio, there are certain key decisions that need to be made around the assets and the funds we use. We wanted to share some of the discussions we have been having to highlight the changes we will be making to portfolios.

We share below the key areas of discussion from the most recent Investment Committee meeting and the resultant changes we will be making.

What changes are you making?

The changes to the growth assets in the portfolio are as follows:

- Legal & General UK Index and Legal & General International Index funds to be sold and reinvested into the Fidelity Index World fund

- Equalise the allocation to Dimensional Global Value fund and Dimensional Global Small Companies fund.

The specific reasons for these changes are set out below:

Relevance of the UK Stock market

We have discussed previously that sometimes investors choose performance comparisons that may not be appropriate. One of these we often come across is the comparison of portfolios to the FTSE 100 stock market index. The FTSE 100 measures the performance of the largest 100 firms listed in the UK and is frequently quoted in the papers and media outlets. The comparison when used to gauge the performance of equities is loosely correct, as global stock markets are reasonably well correlated so if the FTSE 100 is going up it may well be that our growth assets and therefore portfolio values are going up also.

Over the last few years, the FTSE 100 has been one of the better performing stock markets, largely due to its exposure to energy stocks – BP and Shell as an example which have benefited from the increase in oil prices after the Russian invasion of Ukraine. However, the UK exposure is only part of the growth asset exposure in portfolios and with pressure on other areas, most notably the fixed interest securities (which form the defensive assets in portfolios) some investors have been disappointed to see falls in their portfolio when comparing against a rising FTSE 100 index. This comparison however is apples v pears.

It is important to remember however that the FTSE 100 is not representative of the constituents of your portfolio as it only measures the performance of 100 UK companies and is pure equity based which makes it very high risk. Your portfolio on the other hand consists of both global equities and also bond investments which provides a very different level of risk and investment experience.

Investing in the UK

Historically, investors have favoured companies listed in their home country as opposed to those overseas. This home bias was partially down to the additional cost, complexity, and unfamiliarity of investing overseas, although these hurdles are relatively negligible nowadays.

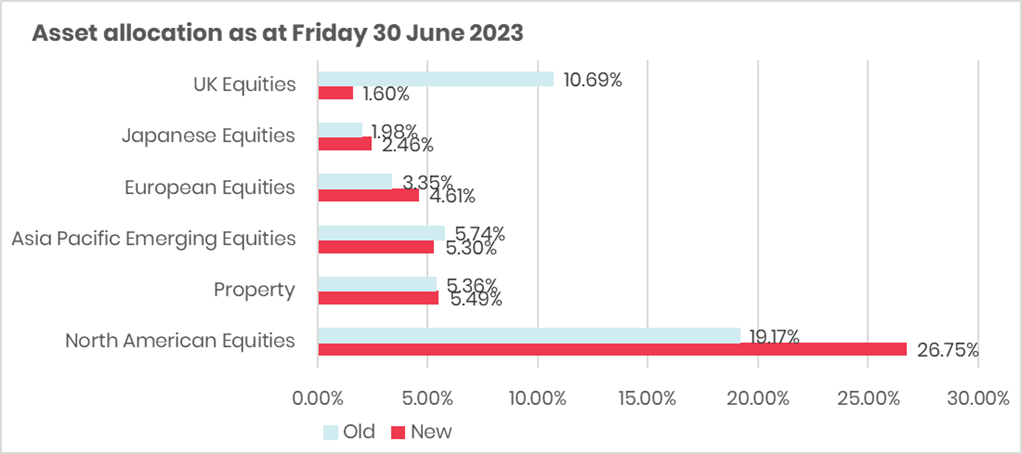

For some time, we have had an overweight in UK stocks which we have been steadily reducing. The UK stock market only forms about 4% of the global total but currently makes up about 20% of growth assets in our portfolios. A medium risk investor currently has a UK equity exposure of 10% and a market weighting value would reduce this to 1.6%. Whilst we have had this overweight since the portfolios began, it is not an overexposure to the UK economy as most large UK companies will derive much of their profits from overseas. This exposure in reality has always been largely global and the Investment Committee has been considering if we should maintain this overweight position.

The chart below looks at the shorter period returns of the FTSE 100 and global developed equities. Overall, the return has been reasonably correlated as you can see from the shape of the graph below. Rolling annual returns show the recent outperformance of the FTSE 100 as highlighted above but also that there have been other periods of underperformance, notably during the pandemic.

Rolling 12-month returns of the FTSE 100 and global equity markets

Data source: Morningstar Direct © All rights reserved. Funds: HSBC FTSE 100 Index Fund, Vanguard Global Stock Index Fund.

When reviewing which assets to include in portfolios, we have to balance both performance and risk considerations. Although the FTSE 100 index has performed strongly in recent years, there are some very sensible reasons why having too many eggs in the basket of the 100 largest companies in the UK makes less sense from an investment portfolio perspective:

- The FTSE 100 is highly concentrated with over 33% of the assets held in just the top 10 companies – the likes of Shell, HSBC and AstraZeneca being the top holdings at present

- The FTSE 100 is materially overweight to certain sectors such as energy (12% vs 5% globally) and underweight to the point of almost not having any in terms of technology (1% vs 21% globally)

- This explains much of the recent performance differential above – where technology has struggled, energy stocks have flourished in the high-inflation environment exacerbated by the Russian invasion of Ukraine

- Over longer periods technology stocks have dominated (Apple, Microsoft, Tesla etc.)

- Investing into global stock markets more broadly means your portfolio consists of over 10,000 companies across over 50 countries against 100 UK Companies in the case of the FTSE 100. Diversifying across them all as a starting point makes good sense and should lead to a smoother investment journey.

On reviewing the allocation to global stocks, we have decided to move more closely to the global market, as measured by the relative stock market value of each country. This will give your portfolio more diversified exposure to profits from large global companies without the current concentration to a handful of large UK stocks.

UK Equity Weighting

For the reasons detailed above, we will be reducing the exposure to UK equities to bring it in line with the global market capital weighting for developed markets. We will be doing this by replacing the Legal & General funds – International Index and UK Index with the Fidelity Index World fund.

Value and Smaller Companies Weighting

At present, we have a higher allocation to global value companies than we do to global small companies. As an example, for a medium risk portfolio there is an allocation of 10% to global value companies and 5% to global small companies. As the potential benefit of both of these strategies are to give additional returns over time and to diversify your investments, we intend to equalise the allocation. This means that for a medium risk portfolio there will be an allocation of 7% to global value companies and 7% to global small companies.

There are no fund changes in this space.

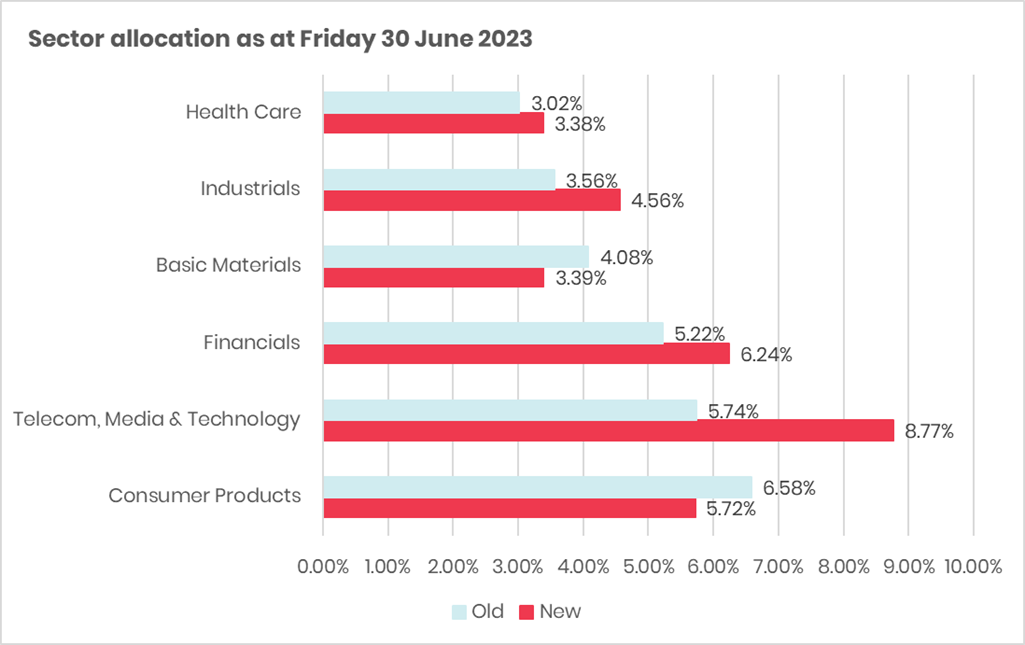

Growth asset and sector allocations

To illustrate the differences between allocations for the changes please see the charts below:

The Investment Committee have also been considering the defensive assets held in Old Mill Portfolios and the impact of recent inflation and high interest rates on those assets.

What changes are we making?

The changes to the defensive assets in the portfolio are as follows:

- A proportion (between 60% & 70% depending on your risk group) of the Dimensional Global Short Dated Bond fund to be sold and reinvested into the Vanguard Global Short-Term Bond Index fund

- Legal & General All Stocks Index Linked Gilt Index Trust to be sold and reinvested between the Dimensional Sterling Inflation Linked Intermediate Duration Fixed Income fund and the abrdn Short Dated Global Inflation-Linked Bond Tracker fund

- The defensive assets allocation to be changed and split equally between short dated high-quality bonds and inflation linked bonds.

- Reduce the cash held in the portfolios.

The specific reasons for these changes are set out below:

Short-dated high quality bonds

With interest rates having risen sharply in a short period and the possibility of them subsequently falling if the expected recession occurs, we are often asked whether this might be a good time to buy longer duration bonds to participate in higher yields and an improvement in bond prices if rates do start to fall.

Generally, we are expecting the growth part of the portfolio to generate the majority of long-term returns. The defensive assets in our view should remain lower risk and we should avoid the temptation to try and eke out small additional returns from higher risk longer duration and lower credit quality bonds. It is important we retain the defensive characteristics in this part of the portfolio as it gives us the reassurance to take on equity risk.

Diversification of short-dated bonds

We currently have a large allocation to the Dimensional Global Short Dated Bond fund. This has been a solid performer in the past, but we now have access to other funds which have a slightly different investment approach and we believe this diversification will be beneficial to the performance of the portfolios. The existing fund has a variable duration strategy so can vary from its current duration of about 1 year up to 5 years. The geographical split can also vary, currently the top allocations are to Canada, UK and Australia.

The Vanguard Global Short-Term Bond Index fund will be added as a diversifier in the short-dated bond fund allocation via a 50/50 split with the current Dimensional fund. The duration and geographical split of the Vanguard is far more static with a majority of holdings in the US and a duration of approximately 3 years. We believe this will be complimentary to the Dimensional fund.

Changes to inflation linked bonds

One of the risks to the defensive part of portfolios is inflation. The Short-dated bonds held in portfolios should provide acceptable inflation protection if inflation comes in at anticipated levels as it will already have been incorporated in bond yields. As bonds mature, their proceeds can be reinvested into bonds with yields that should compensate investors for any changes in the anticipated level of inflation.

We are currently experiencing a period of unanticipated high levels of inflation which presents a significant risk that purchasing power could be eroded in the short term with short dated bonds. Index linked gilts – and other inflation-linked bonds (hedged to sterling) on the other hand provide structural protection against inflation as the value is indexed upwards at the rate of inflation and any income is paid based on the inflated amount.

Ideally, we would use a short dated index linked gilt fund for this allocation to give exposure to UK Inflation with a lower volatility from shorter dated bonds. Unfortunately, there is not currently a suitable fund available to us.

Index linked gilts issued over the last few years have been of longer duration, and consequently there is a limited number of shorter dated index linked gilts available. There are also specific fund rules that limit the proportion that can be held in individual gilts making the creation of a short dated gilt fund impossible at this time. In the absence of this option, we have been using a measured exposure (at a lower allocation) to longer duration bonds hence the use of the Legal & General All Stocks Index Linked Gilt Fund.

Having reviewed our options in this space following recent fund developments, we are taking the opportunity of using shorter dated overseas inflation linked bonds (hedged to sterling). While this only provides a proxy for UK inflation protection, this will provide diversification from the impact of longer duration index linked gilts. The abrdn Short Dated Global Inflation-Linked Bond Tracker fund comprises high quality bonds (overall AA) and will be introduced into the portfolios.

Alongside this, we have also decided to introduce a shorter duration index linked gilt fund. While a short-dated fund is not possible, the Dimensional Sterling Intermediate Duration Index-Linked Gilt fund we are introducing limits the duration to no more than 15 years so will be approximately half the overall duration of the current L&G index linked gilt fund.

The Dimensional and abrdn funds in combination provide shorter duration and therefore less volatility than the current L&G fund.

Short dated / Inflation linked bond split

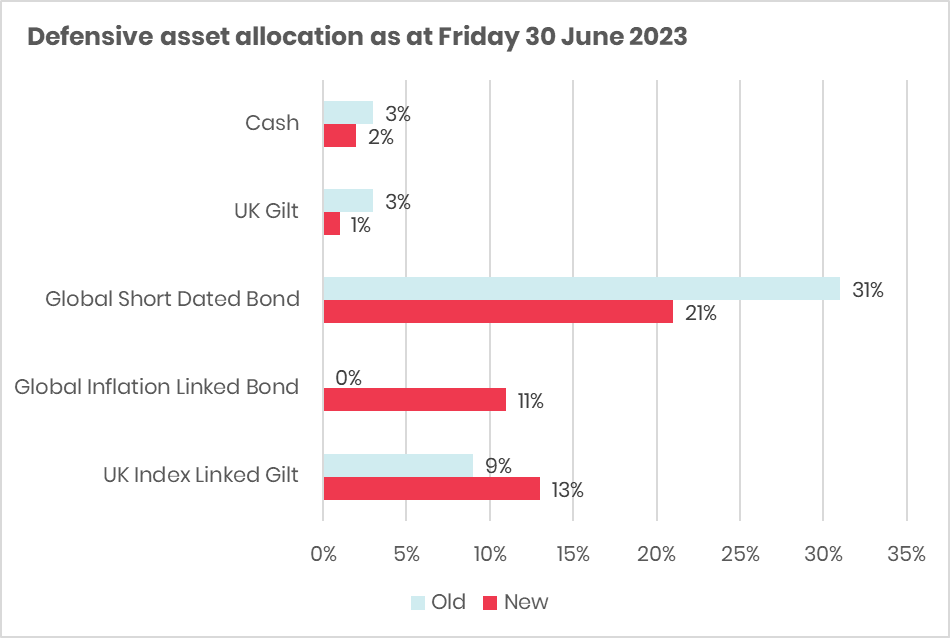

Reflecting the new funds in the portfolios, we will increase the allocation to inflation linked bonds and defensive assets and move to a 50/50 split between short dated high-quality bonds and index linked bond / gilts.

Level of cash

Portfolios currently hold between 3% and 5% in cash. Cash sits in the defensive part of portfolios as a stable asset and is held primarily to cover fees and withdrawals. On annual rebalance, the cash fund is topped up when the portfolio is returned to its original allocation.

We intend to reduce the level of cash held in all portfolios to 2% of the value and to reduce the necessity to top up the cash fund from time to time by selling funds, we will be switching funds to income units. At present portfolios are either growth portfolios, which hold accumulation units and any income is reinvested automatically in the fund, or Income portfolios which have income units and any income is paid into the M&G Wealth cash fund. By moving all funds to income units, any income generated by the funds will be paid into the cash account to top it up on an ongoing basis. If you have a growth portfolio at present the change will be made in October by converting the accumulation units to income units. This will not have any additional tax implications.

Defensive asset allocation

To illustrate the differences between allocations for the changes there is a chart below:

We will be sending out a letter to all clients impacted with details of the changes the week commencing Monday 14 August, and if you have any questions about the upcoming changes, please contact your financial planner.