Property as an investment

There is no doubt that many established buy-to-let landlords have made considerable money over the years. For those with money to invest, looking back at history could point to returns from buy-to-let comparable or even superior to more conventional investing via equity and bond portfolios. We should however be considering some of the recent developments to look at the viability of property investment for the future.

9th February 2023

-

Gavin Jones See profile

Gavin Jones See profile

Rising interest rates, recent tax reforms and increased regulation mean newcomers and those with high loan-to-value mortgages should proceed with caution.

The rise in house prices over the years has been driven by a combination of factors including a rising population, a lack of new housing stock and very low borrowing rates.

While long standing landlords may have little or no borrowing, newcomers to the market may have large mortgages. While these were easy to service when interest rates were low, the sharp increases through 2022 and continuing this year will have substantially increased costs for many landlords.

Combined with pressures on affordability for renters as a result of the cost of living crisis, increasing rents to cover the higher mortgage costs could cause tenants to seek lower cost accommodation.

In successive budgets over the years, it seems there has been a number of tax changes that fundamentally change the profit dynamics and thus risks to the buy-to-let investment proposition. These changes include:

- A supplemental 3% duty being applied to all bands of stamp duty (SDLT) in 2016 so the cost of acquiring investment property was higher.

- Previously, landlords could automatically offset 10% of their rental income as costs, but this was changed at the same time, so they are only able to offset actual costs incurred.

- While landlords were previously able to offset all mortgage interest payments against rental income, from 2020, they have only been granted tax credit worth 20% of the interest cost to offset against income tax, irrespective of their marginal rate of tax.

- In the latest budget, the Chancellor reduced annual capital gains tax allowance from £12,300 to £6,000 from April and then £3,000 from April 2024. In addition, the capital gains tax rate for residential property is higher at 28% rather than 20% on most assets apart from property, or for basic rate taxpayers, 18% rather than 10%. Consequently, the costs for landlords to exit their properties has also increased.

Since 1 April 2020, landlords can no longer let or continue to let properties covered by the Minimum Energy Efficiency Standards (MEES) Regulations if they have an Energy Performance Certificate (EPC) rating below E, unless they have a valid exemption in place.

In 2021, the Government consulted on bringing this minimum level up to a C rating, from 2025 for new tenancies and 2028 for existing ones. This legislation hasn’t yet been confirmed but bear this in mind when looking for new property or factor it in if you have a rental property and the EPC doesn’t meet this level as there may be additional costs in the future.

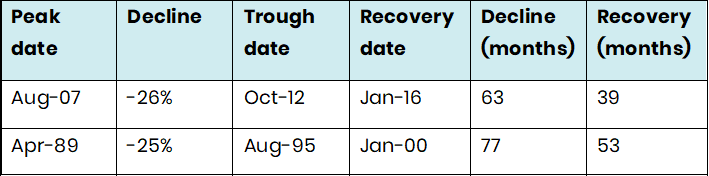

Take a look at the table below, which sets out two of the largest falls in house prices since the Halifax Property Index began in January 1983. Interest rates rises have caused the housing market to dip but at times house prices can and do fall.

Source: Halifax UK All House Price Index

When inflation was taken into account, the property ‘crash’ in the late 1980’s meant that house prices took over ten years to recover their value to the previous peak of April 1989.

The last few years saw an acceleration in house prices, particularly in the South-West. However, those that bought at the peak may well now have a property that will be worth less than they paid for it.

House price rises have been good for most of us. Our own homes usually bought with a mortgage at outset have seen their value increase many times over in the last twenty years or so.

It is borrowing that has made many buy-to-let owners wealthy in rising markets, but this, along with the tax and regulation headwinds may mean returns will be lower, for the next few years anyway.

The perception sometimes is that it is a small step from your money sitting in cash to buy-to-let. We do hear the view that ‘property values never fall’ regularly. In reality, it is leaping from one end of the risk spectrum to the other, particularly if an investor is borrowing heavily to buy the property. When individuals enter the buy-to-let market in this way, they are in fact starting a very highly geared business with all the costs, tax, reporting issues and risks that go with the territory. The business may also be difficult to get out of at times – the sale of a property can be a long and stressful process.