Q1 2025 – Investment Performance Report

We have reported below on the first quarter of 2025. Whilst it is usual to provide quarterly performance figures, given the events of the last few weeks, we have provided performance figures to the time of writing on Thursday 10 April. By the time you are reading this, markets will have moved on again but nevertheless, these charts will show defensive assets have been doing their job to protect portfolio values.

On Wednesday 2 April, US President Donald Trump announced the ‘reciprocal’ tariffs on imports into the US. The tariffs had been announced in advance and had been the focus of speculation in the weeks before, but it still turned out to be a lot worse than expected.

Perhaps adding to the immediate confusion, the tariffs were calculated in such a way (with reference to existing trade deficits with countries as opposed to any trade tariffs) that it is extremely difficult for the countries affected to propose an immediate solution.

The initial reaction from equity markets has been negative. Economic commentary has proposed that the tariffs will cause an increase in inflation, the potential for a US recession and a drag on the global economy.

The risk you have chosen to take with your investments continues to determine the investment journey. In the very near term, those with lower risk tolerances have seen smaller falls than those taking more risks in their portfolios. While we report on the shorter-term performance, the nature of investing is much longer term – in years, not days and weeks. Longer term performance is shown later in this article.

10th April 2025

-

Gavin Jones See profile

Gavin Jones See profile

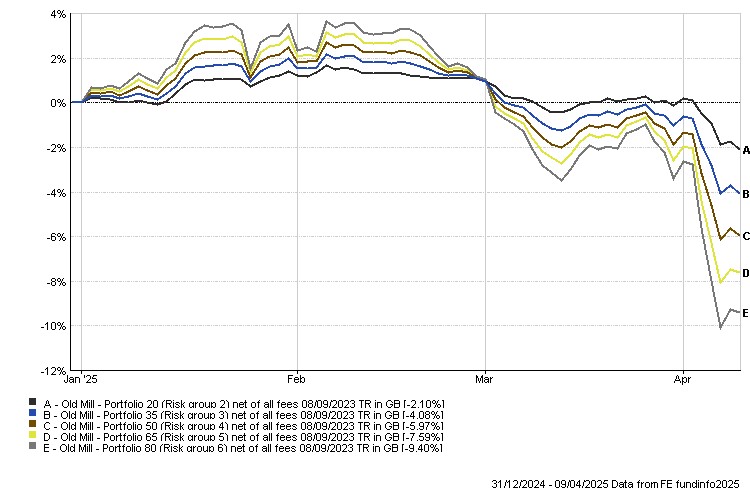

Performance over the year to date (from Tuesday 31 December 2024 to Wednesday 9 April 2025)

The prospect of Donald Trump as US president meant that the final quarter of 2024 and the beginning of 2025 was positive for most portfolios, with his policies seen generally as positive for stock markets. However, since his inauguration on Monday 20 January, the stream of policy decisions and executive orders from the White House has caused some consternation.

The world has watched as the US fell out diplomatically with Ukraine, President Trump speculated about the future sovereignty of Gaza, Greenland and Canada and extolled the virtues of tariffs.

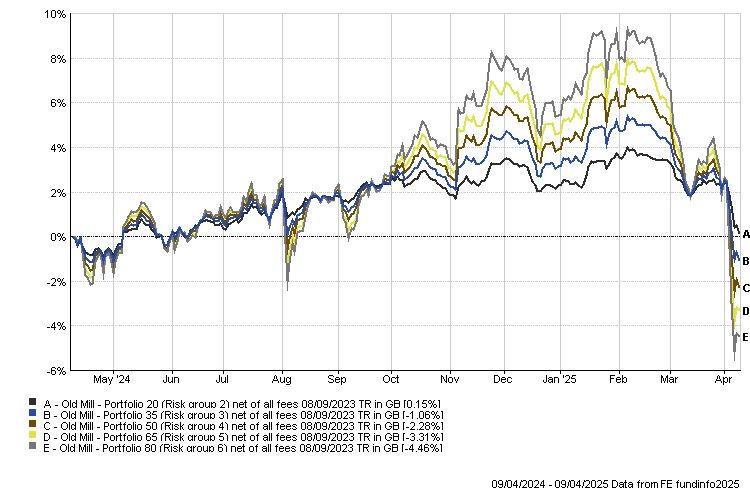

Performance over the last year (up to Wednesday 9 April 2025)

Over the year, taking into account the falls in April, most portfolios are now showing some falls. The magnitude of falls can be seen with our Portfolio 80, with strong growth of almost 10% from this time this year to February. But with this portfolio having the majority of its assets in stock market investments it has seen a sharp fall since its peak at the beginning of February. If a global solution to the tariff situation is found we could see investments rebound quickly. Time will tell.

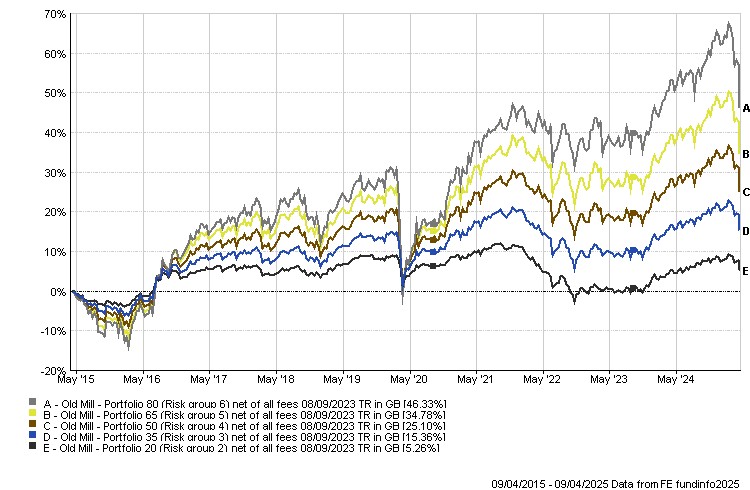

Longer term performance over the last 10 years (up to Wednesday 9 April 2025)

The ten-year returns illustrate the value of investing over the longer term. It also highlights that in pursuing higher returns, there will be periods of volatility that call for patience and trust in the investment process. Nowhere did we see this more than in the early days of the covid pandemic in spring 2020 where markets saw a sharp fall over February and March before staging a recovery to the previous peak over the next five months.

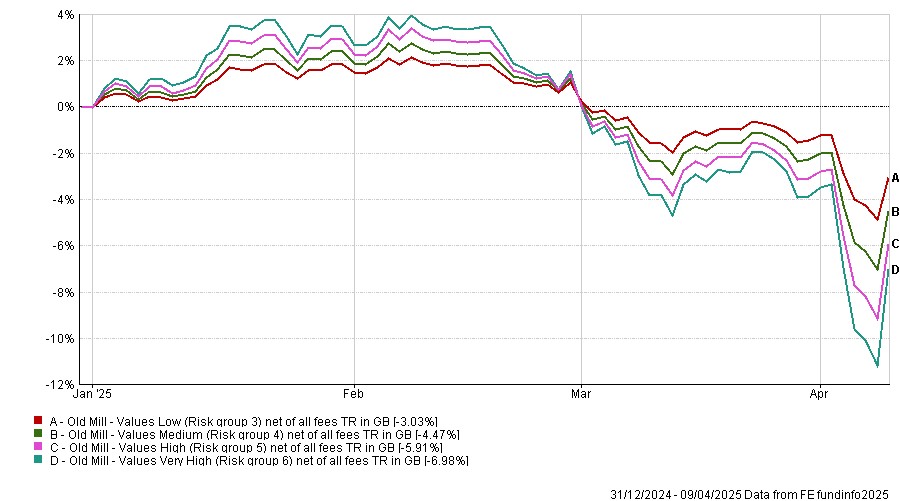

Performance over the year to date (from Tuesday 31 December 2024 to Wednesday 9 April 2025)

Values portfolios have seen similar returns over the period to standard portfolios.

Performance over the last year (up to Wednesday 9 April 2025)

Performance over the last year for values portfolios has been slightly positive when compared to the original portfolios with the ESG screened global equity fund rebounding quickly.

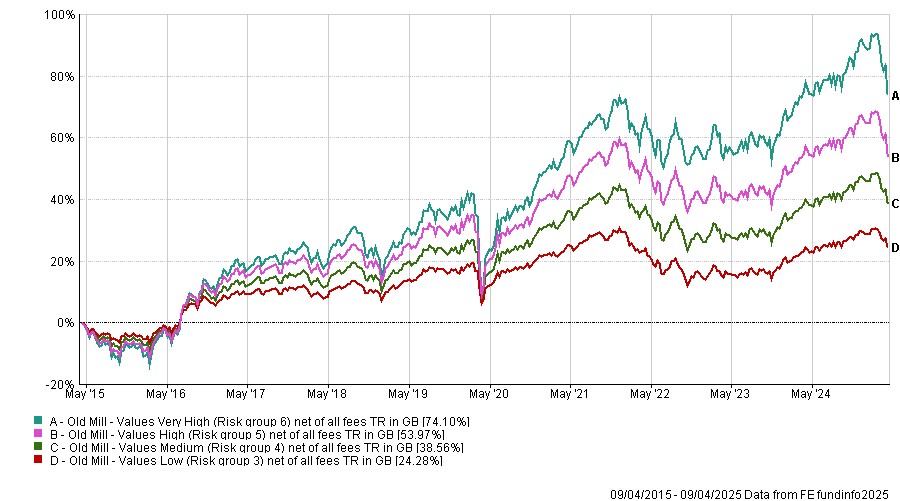

Longer term performance over 10 years (up to Wednesday 9 April 2025)

The values portfolios have only been available to our investors for the last five years, but the graph below shows the longer time frame of ten years showing the potential upside over longer periods.

Longer term performance of the values portfolios shows robust growth.

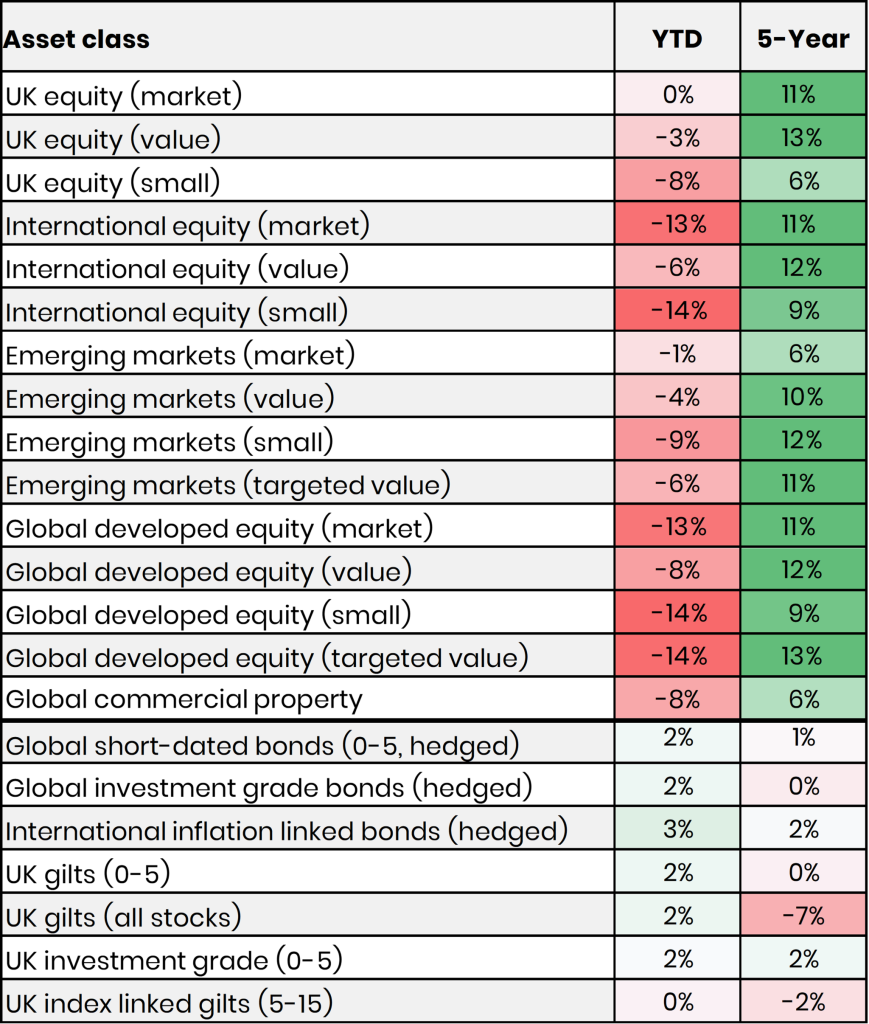

The table below shows the performance of a number of asset classes in 2025 so far and the annualised return over the last five years as at close of play on Friday 4 April.

Defensive assets

Defensive assets, for longer-term investors, play an important role in all portfolios. For more cautious investors, they provide downside protection by delivering lower levels of potential falls than equity markets and should preserve purchasing power over the long term. For more risk tolerant investors, they provide a crucial balance against equity market trauma, delivering solid returns to offset equity market losses.

Short-dated, high-credit-quality bonds provide useful defensive properties. Their short-dated nature, i.e. the amount of time until the bond matures and capital is repaid, leads to lower volatility than longer-dated bonds, all else being equal. High-credit-quality bonds tend to attract money fleeing from riskier assets at times of equity market trauma, driving prices of these bonds up.

At times of unanticipated high inflation, such as the 1970s, ordinary bonds risk losses to purchasing power. Inflation-linked bonds provide a structural link to inflation indices, such as the UK’s Retail Price Index, providing some protection from inflation. Ideally, inflation-linked bonds should be shorter-dated to reduce unwanted volatility, although in practice, good products in this space remain limited. We use index linked gilts of 5 to 15 year duration and also balance this with global short- dated inflation linked bonds.

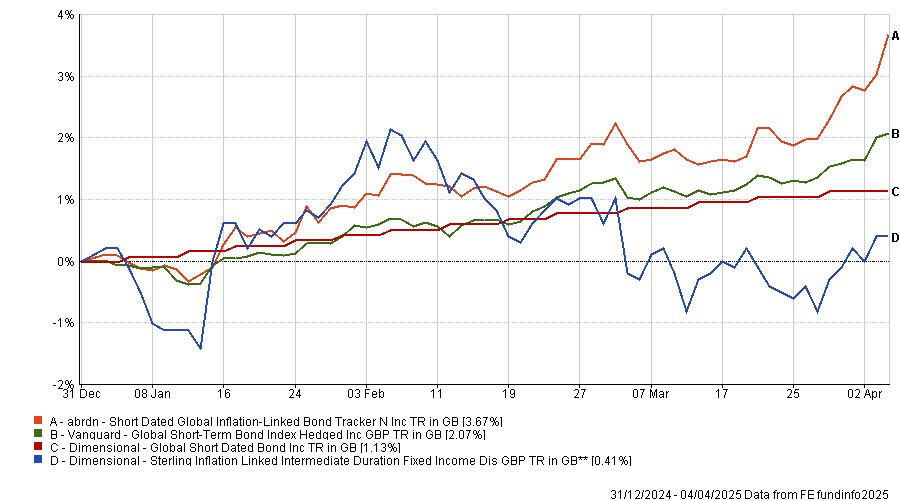

Looking at the funds themselves, through the turmoil we can see the protection of capital overall.

Defensive Assets performance over the year to date (from Tuesday 31 December 2024 to Friday 4 April 2025)

Of course, there are headwinds for all asset classes and you can see the greater movement of the inflation linked intermediate duration fund. As this has a longer duration than the other funds, it may be impacted more as one of the potential consequences of Trump’s tariffs for the world is higher future inflation and interest rates. As you will remember from 2022, this can be detrimental to bonds with a bigger impact, the longer the duration of the bond. The overall impact on your portfolio value, depending on the proportion of defensive assets you have has been positive.

In recent days there have been yield rises for US government bonds (US Treasuries) in particular. This will be in part due to the higher inflation expectations as described above. However yields can also rise if there is an increase in risk for an asset – investors demand a greater return if they are taking on more risk. At the moment we do not see a need to change the defensive assets in your portfolio, but will be keeping an eye on developments.