Q2 2025 – Investment Performance Report

We have reported below on the second quarter of 2025, which, after a volatile first quarter, has seen overall performance more positive.

In April, US President Donald Trump announced the ‘reciprocal’ tariffs on imports into the US. The tariffs had been announced in advance and had been the focus of speculation in the weeks before, but it still turned out to be a lot worse than expected. Initial reaction from equity markets was negative, but looking back at the time of writing, there has been a de-escalation in the tariffs in the days and weeks since.

The future remains highly uncertain, with many plausible scenarios and a wide range of views about which are most likely. Fortunately, for individual investors who trust that markets are broadly efficient, we can rely on the collective intelligence of the market for guidance. It processes this vast, complex web of scenarios, risks, and probabilities, and distils them into a single figure: the price of each stock and, in aggregate, the market itself.

Rather than trying to predict whether the US will now flounder under President Trump, or the outperformance of the US continues, we have taken a neutral stance – neither moving overweight nor underweight U.S. equities based on short-term narratives. This neutrality reflects the collective wisdom and aggregate expectations of all market participants.

By avoiding market timing, which according to substantial academic evidence is regarded as a strategy with a poor track record, and remaining diversified through well-structured, low-cost systematic funds, investors increase their odds of achieving strong outcomes.

10th July 2025

-

Gavin Jones See profile

Gavin Jones See profile

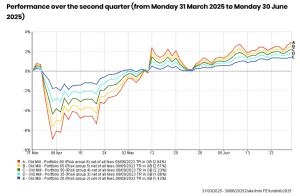

The risk you have chosen to take with your investments continues to determine the investment journey. In the very near term, those with lower risk tolerances have seen smaller falls than those taking more risks in their portfolios. While we report on the shorter term performance, the nature of investing is much longer term – in years, not days and weeks. Longer term performance is shown later in this article.

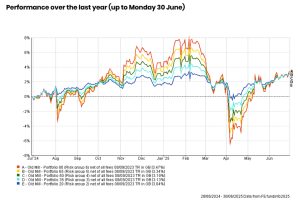

Over the course of the last year, despite the falls seen in April, portfolio returns have been positive. The risk of market timing can be seen with our Portfolio 80, with strong growth of 8% from this time last year to February. With this portfolio having most of its assets in stock market investments, it has seen a sharp fall since its peak at the beginning of February until the beginning of April. The news was certainly disconcerting as the tariff situation played out, but at the time of writing, portfolios have recovered well.

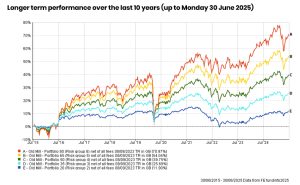

The ten-year returns illustrate the value of investing over the longer term. It also highlights that in pursuing higher returns, there will be periods of volatility that call for patience and trust in the investment process. Nowhere did we see this more than in the early days of the COVID-19 pandemic in spring 2020, where markets saw a sharp fall over February and March before staging a recovery to the previous peak over the next 5 months.

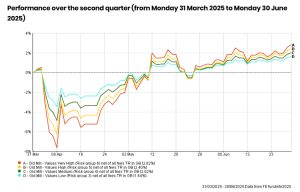

Values portfolios have seen similar returns over the period to standard portfolios.

Performance over the last year for Values portfolios has been slightly lower but still positive when compared to the original portfolios, with the ESG screened global equity fund rebounding quickly.

The Values portfolios have only been available to our investors for the last five years, but the graph below shows the longer time frame of ten years, showing the potential upside over longer periods.

Longer term performance of the Values portfolios shows robust growth.

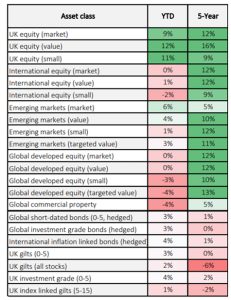

The table below shows the performance of a number of asset classes in 2025 so far and the annualised return over the last five years as at close of play on Monday 30 June.

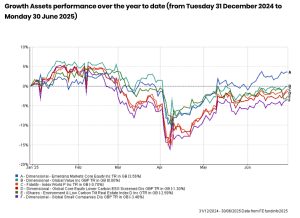

Growth assets

These assets form the ‘engine’ of your portfolio and consist of higher return, equity investments. To own an entire portfolio made up of these higher risk investments – however well-diversified, would take some staying power when markets are in turmoil. In the past, portfolios of growth assets have fallen by as much as half or more, before recovering over time.

Since the beginning of the year, there has been pressure on these assets, with only emerging markets ending the last six months positive. After falls, they have all been recovering well since April.

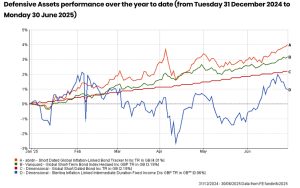

Defensive assets

Defensive assets, for longer-term investors, play a key role in all portfolios. For more cautious investors, they provide downside protection by delivering lower levels of potential falls than equity markets and should preserve purchasing power over the long term.

Short-dated, high-credit-quality bonds provide useful defensive properties. Their short-dated nature, i.e., the amount of time until the bond matures and capital is repaid, leads to lower volatility than longer-dated bonds, all else being equal. High-credit-quality bonds tend to attract money fleeing from riskier assets at times of equity market trauma, driving the prices of these bonds up.

At times of unanticipated high inflation, such as the 1970s, ordinary bonds risk losses to purchasing power. Inflation-linked bonds provide a structural link to inflation indices, such as the UK’s Retail Price Index, providing some protection from inflation. Ideally, inflation-linked bonds should be shorter-dated to reduce unwanted volatility, although in practice, good products in this space remain limited. We use index-linked gilts of 5 to 15 years duration and balance this with global short-dated inflation-linked bonds.

Looking at the funds themselves, through the turmoil, we can see the protection of capital overall.

Of course, there are headwinds for all asset classes, and you can see the greater movement of the inflation-linked intermediate duration fund. As this has a longer duration than the other funds, one of the potential consequences for the world is higher future inflation and interest rates. Most global central banks have been taking stock of the US tariff cuts and have either paused interest rate cuts or have been cutting at a slower pace than was previously predicted. As you may remember from 2022, rising inflation and interest rates can be detrimental to bonds, with a bigger impact the longer the duration of the bond. The overall impact on your portfolio value, depending on the proportion of defensive assets you have, has been positive.