Review your Inheritance Tax (IHT) position

We have written previously on the major Inheritance Tax reforms unveiled in the November Budget affecting Business Property Relief (BPR) and Agricultural Property Relief (APR) . As this may result in increased IHT liabilities, it is important that the impact of these changes is reviewed ahead of them coming into force in April 2026 so plans can be adapted as necessary to limit the impact.

10th February 2025

-

Gavin Jones See profile

Gavin Jones See profile

Agricultural Property Relief (APR) and Business Property Relief (BPR)

Under current rules, assets that qualify for 100% BPR or APR have an unlimited amount of benefit. The original intention of these reliefs was to avoid the breakup of a family business on the death of an owner. It is a valuable relief and the IHT savings on large estates can run into £millions at present.

In the Budget, it was announced from 6 April 2026, there will be a new £1 million allowance introduced. This will be a combined benefit between agricultural and business property with any excess above this limit qualifying for relief but at the lower level of 50% rather than the current 100%. This results in a tax rate of 20% on qualifying business and agricultural assets in excess of £1 million.

For example, if an individual owns £1 million of assets that currently qualify for 100% APR and £1 million of assets that qualify for 100% BPR, on death after 5 April 2026 those assets will be combined so £1 million would get 100% relief from tax and the remaining £1 million would only get 50% relief. The result is an increase in IHT from zero to £200,000.

This reduction in the allowance could have significant and wide-ranging implications on some estates and will require some careful planning to try and mitigate the impact. The new allowance is still at an early stage with a technical consultation due to be published in early 2025 to provide additional details and draft legislation. Once we have this, we will be in a better position to consider what planning will be possible.

Understand your position

April 2026 will come soon enough and once the final legislation is known there may not be much time to implement any changes to your current planning. The first step is to understand your Inheritance Tax position and the tax you and your family may incur once the proposed changes come into effect. We would urge you to take professional advice as this can be complicated and rules change periodically. At Old Mill we have experts in Tax and Financial Planning so are ideally placed to give advice on your individual circumstances.

Review your affairs

A good starting point would be to review your will (or write one if you don’t have a will). While a husband and wife each have a £1 million APR/BPR allowance, unlike the IHT nil rate bands, this isn’t transferable between spouses. So, a simple mirror will that passes everything to a surviving spouse who would only then have a £1 million allowance may have large consequences if your business assets are worth over £1 million.

Case Study

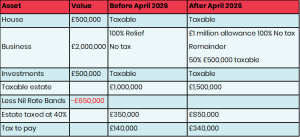

Barbara and Jim have an estate of £3 million consisting of the following assets split equally between them:

House £500,000

Business £2,000,000

Investments £500,000

Their wills are currently written on a mirror basis, so everything passes to the survivor on the first of them to die. Barbara dies and leaves everything to Jim. The table below shows the differences based on Jim dying after Barbara before and after April 2026.

As the total estate is over £2 million, the Residence Nil Rate Band (RNRB) is reduced by £1 for every £2 over this limit. Therefore, the RNRB is reduced from £350,000 to zero.

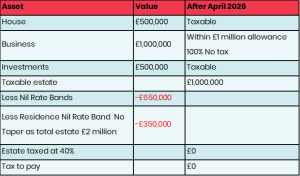

Before Barbara’s death, she also has a £1 million business relief allowance after April 2026 under the new rules but this is not transferable upon death like the nil rate bands so is effectively lost. If circumstances allow and she transfers her share of the business to her children through her will, this means her allowance is utilised. As she has gifted assets away, it also brings Jim’s total estate down to £2 million so the RNRB is available.

So, on Jim’s death, the estate will look like this:

In this example, by changing the terms of the will, it is possible to save £340,000 of Inheritance Tax which highlights the importance of reviewing wills post any material tax changes.

Plan for the changes

One of the recurring themes with clients is how IHT is to be paid. When the bulk of assets is made up of land and property or perhaps a business, it may not be possible to sell part to pay an IHT bill which becomes due. While not suitable for everyone, putting a life insurance policy under Trust for some or all of the tax due can be a simple way of ensuring your executors have the money needed to pay the tax on your estate.

While estates with assets that may be difficult to sell quickly can pay tax by instalments to give time, this does incur interest at the current rate of 3.75%. Also, it still may not be desirable to sell the business or asset so the tax will have to be found elsewhere, such as borrowing.

Transfers after Budget day

As the changes will only affect deaths occurring after 5 April 2026, there is still time to plan and make transfers of assets. New rules were included alongside the Budget so if you transfer agricultural or business property on or after Budget day and die on or after 6 April 2026 and within seven years of transfer, the new £1 million allowance will still apply so care is needed, especially when the donor is in ill health.

It is also important to consider the Capital Gains Tax (CGT) consequences of transfers. The transfer of assets is typically a disposal for CGT purposes so transferring will cause any gain on the assets to become chargeable and, consequently, there could be a significant CGT liability to consider. This will need to be balanced against any potential Inheritance Tax savings.

It may be possible to defer this tax for business assets by ‘holding over’ the gain to an individual or a Trust but this is a complicated area and professional advice should be taken if you are considering this.

Later Life

While the new changes will only apply to deaths after 2026, there are wider ranging implications and planning that has taken place in the past will affect families.

For those who have died within the last two years, it may be possible for the Executors to go back and ‘rewrite’ the will using a legal document called a Deed of Variation. This has to be done within two years of death and may provide the opportunity for the will to be changed in such a way as to reflect the changes coming to create a more beneficial Inheritance Tax position.

An example where a Deed of Variation may be worth considering. A recently deceased spouse has passed business assets onto their husband or wife taking them over the £1 million limit. The deed could redirect some of those assets to potentially save tax for the family in the future. So, in the example of Barbara and Jim above, if Barbara had died and already passed her assets to Jim, it would be possible within two years of death to complete a deed of variation and if Jim dies after April 2026 to save £340,000 in Inheritance Tax.

Summary

Significant amounts of Inheritance Tax can be saved through effective planning and the sooner any planning is commenced the better given it can often take seven years for some actions to be fully effective.

It starts with understanding the current position and then reviewing the options to improve upon this but in a manner that is supportive of your overall financial planning objectives. The most appropriate planning strategy is not always necessarily the one that will save the most tax.

Across our Financial Planning, Commercial, Rural and Tax Planning teams, we have huge experience and expertise to support families to conserve their wealth and put in place effective succession plans.

We’re here to help

If you are in business or know someone who is considering what the changes might mean for them, our specialist business and rural teams may be able to help, please do get in touch by clicking here…