Reviewing your pension

Proposals have been made to bring pension funds into estates for Inheritance Tax (IHT) purposes for deaths occurring on or after 6 April 2027.

Until the legislation is published, we cannot be certain how the final rules will look and until then, the current rules will continue to apply. It is difficult to give specific advice at this early stage but below we have given more detail in simple terms of what we believe will be the tax treatment of your pension fund on death post-April 2027.

While details of the changes have not been released, it is still sensible to review your circumstances in light of the proposals.

4th June 2025

-

Gavin Jones See profile

Gavin Jones See profile

The story so far

The limited published information states that IHT will be payable on the value of your pension fund immediately before death. The IHT charge will need to be calculated by the pension scheme administrators and held back before funds are distributed or designated to beneficiaries. The scheme administrators will pay any IHT due directly to HMRC.

The process will require the personal representatives and the pension scheme administrator/trustee to work together to establish the IHT charge and the proportion of the charge the pension scheme must pay.

As an example, consider an estate of £2 million which includes a pension fund of £1 million for an individual with no spouse and no children. They have an IHT nil rate band of £325,000 which will be shared equally between the free estate and the pension fund. The personal representatives contact the pension scheme administrators and agree that the IHT nil rate band will be split equally between the free estate and the pension fund.

The pension administrators ignore the half share of the nil rate band (£162,500) and apply 40% IHT to the remainder. £1 million – £162,500 = £837,500 x 40% = £335,000 IHT for the pension scheme to pay to HMRC.

This leaves £665,000 in the pension fund to be distributed according to the deceased’s wishes.

Spousal Exemption

Spousal exemption will work in the normal way so if your spouse or civil partner is nominated for the entire pension death benefit, there should not be an IHT charge on the first death at least.

In the example above, if there was a surviving spouse or civil partner, there would be no charge to IHT.

Existing pension tax charges

Although pension funds currently are not subject to IHT, they can be subject to other pension charges which we believe may continue to apply post-April 2027 in addition to any IHT charge.

At the present time, we understand IHT will be calculated and charged before any existing tax charges are applied. Broadly, this means there will be a difference depending on whether you die before or after age 75 and who your death benefit goes to. Put simply, unless your pension is nominated to your spouse, the fund available to be distributed could be reduced by up to 40%.

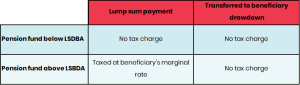

If you die before your 75th birthday

There should be no additional tax charges where benefits are taken in the form of a beneficiary’s drawdown plan.

However, there could be additional tax due for those below 75 where the pension death benefit is taken in the form of a lump sum death benefit above the Lump Sum and Death Benefits Allowance (LSDBA). The standard LSDBA is £1,073,100 but higher figures may be possible if pension protection is in place.

The table below isn’t exhaustive but covers the tax charge for most scenarios.

It will often be better from a tax point of view to use beneficiary drawdown for any benefit above the LSDBA to avoid any immediate marginal rate tax charges on lump sum death benefits. Instead, under beneficiary drawdown, tax is only applied when withdrawals are taken and the beneficiaries are standard or higher rate taxpayers.

After your 75th birthday

For deaths occurring after age 75, where benefits are transferred to a beneficiary drawdown plan, any funds subsequently withdrawn will suffer Income Tax in the hands of the beneficiary at their own marginal rate of Income Tax.

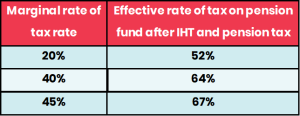

Rather than the death benefit being payable to a drawdown plan, there is also the option for a lump sum to be paid. Where a lump sum payment is made to an individual, there is a marginal rate tax charge on the recipient of up to 45%, which, including the IHT, can mean a total tax charge of up to 67%.

The table below shows the effective tax rate where death benefits are provided via a drawdown plan having incurred IHT at 40% and Income Tax in the hands of the beneficiary at their marginal rate of tax.

As for deaths before age 75, it may also be better to use beneficiary drawdown to avoid the 67% tax charge on lump sum death benefits, where tax is only applied when withdrawals are taken and the beneficiaries are standard or higher rate taxpayers.

A lump sum can also be paid into a discretionary trust, subject to a marginal tax rate of 45%. Subsequent distributions from the trust to beneficiaries are paid with a 45% tax credit, however, for those beneficiaries paying lower rates of tax, they can reclaim the difference between their tax rate and 45%.

Impact on your estate

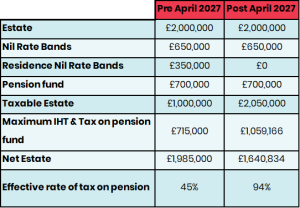

There are unanswered questions about the interaction with estate planning in general. For those with estates over £2 million, the Residence Nil Rate Band (RNRB) is reduced by £1 for every £2 above this limit. So, for an individual’s estate above £2,350,000 the £175,000 RNIB is removed completely. Similarly, a couple’s RNRB of £350,000 will be lost on estates over £2,700,000.

Our current understanding is that pension funds would be included in the estate for this calculation. In certain situations, this could lead to an effective tax rate on your pension fund after 5 April 2027 of over 90%.

As an example of this if an estate worth £2m is left to direct descendants by a couple who die after age 75 and includes a property and a pension of £700,000, it would have around £400,000 deducted in IHT and a maximum pension fund charge of £315,000. The family would receive just under £2m.

Based on our interpretation of the new rules from 2027, the beneficiaries would receive over £344,000 less – because of the pension fund falling into IHT and the loss of the Residence Nil Rate Band allowance. The resultant effective tax rate on the pension fund is over 94%.

This is because the pension would bring the estate above £2,700,00 so wiping out the RNRB.

The pension would also absorb part of the two £325,000 nil rate bands that can be claimed on any estate, further increasing the IHT due.

What next?

Until final details are known, we are not able to provide specific advice. While the current rules remain in place until April 2027, you may not want to disturb your current arrangements for dealing with your pension fund on death.

For those who are likely to draw on their funds significantly to support their retirement income requirements, these changes are likely to have less impact. For those who do not require their pension funds to generate income, these changes are potentially very significant, and how this can be managed will require very careful consideration. In all cases, the implications of this change will need to be factored into your planning.

Starting to draw upon your pension

If you are over the age of 55 (rising to 57 from April 2028) you can start drawing on your pension fund, with a tax-free lump sum of usually 25% of the fund value (within limits) and any income received is simply taxed at your marginal rate of Income Tax.

For anyone who is a non-taxpayer or pays tax at the basic rate and, especially those over the age of 75, it may now be beneficial to start drawing income ahead of the changes in April 2027 provided it remains taxable still at the basic rate. Even where this income is not required, it could potentially be free of IHT if gifted whereas leaving the funds to accumulate in the pension could mean they will become taxable if the estate is liable to IHT.

If you have reached the age of 75 and not yet drawn your tax-free cash sum, then it is likely to be sensible to take this before the changes in 2027. Whilst the lump sum may be liable to IHT at 40% in your estate, it will avoid additionally incurring pension charges as well, which would see an overall effective tax rate of 67%. Your financial planner will be able to advise on the merits of doing this in your circumstances.

Pension nominations

It is likely all pensions and death benefit nominations will need to be reviewed before the changes take effect and especially for those who have earmarked their pensions for estate planning purposes.

For those with a spouse or civil partner, it is likely to become the default that they are nominated to avoid an IHT charge on the first to die. This will avoid unnecessarily using nil rate bands that may otherwise be used by the survivor on the second death.

Insurance

With such major changes to pensions, there are other ways to ensure your family receive a similar level of inheritance. One of these is to take out life insurance to cover any shortfall between the pre and post 2027 amounts due. Drawing pension income to cover the premium cost can be very effective. Your Financial Planner can discuss your individual circumstances and advise on the suitability of this option.

Summary

There has long been an argument for a set of consistent rules for pension schemes, as this gives people confidence to plan for the future. While some of the proposed changes are understandable from a tax point of view, the cliff-edge implementation in 2027 will have serious consequences for some who had planned within the existing rules.

The inclusion of pension funds within estates for IHT purposes is potentially very complex, and as a consequence, it also seems that the job of personal representatives will get more onerous with the need to deal with pension companies and arrange for them to settle tax liabilities. We have an estate administration service to make this job a little easier for your loved ones on your death and we will be writing about the benefits of this service in a future Insight.

Once the final legislation on the Budget proposals is published, we think that many of you will need to review your financial position to understand the impact of these changes on your own circumstances. They are a potential minefield, making it more important than ever for people to take advice on how best to navigate the changes to reduce the potential impact.

If you have family or friends with pensions who may be impacted by these changes, we have an enquiry service: the financial health check, which can give an initial indication of whether advice should be sought. You can find details of this service here Old Mill Health Check Flyer

If you have any questions or want to discuss your individual circumstances with an Old Mill financial expert, please do get in touch.

We are also holding a webinar to discuss these details, and you can register for this here: Your Inheritance Tax Position & pensions Webinar