Savings rates

Although interest rates remain significantly below inflation, rates have nevertheless increased substantially over recent months.

8th December 2022

-

Gavin Jones See profile

Gavin Jones See profile

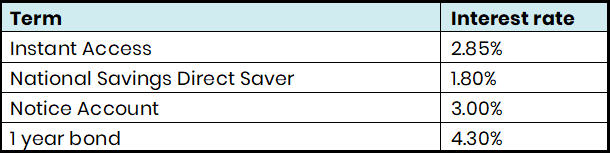

Looking at rates at the time of writing (on December 5) an indicative sample of the rates you can get at present are as follows:

Source: Moneyfacts.co.uk 05.12.22

With interest rates rising rapidly, we typically see mortgage rates increase almost immediately but savings rates can take a little time to catch up.

We have not included institutions in the table above as rates change quickly. If you wish to review the interest rates you are getting currently, please do speak to your Old Mill Financial Planner.

Banks have been under intense scrutiny since the credit crisis in 2008 and The Financial Services Compensation Scheme (FSCS) was established to provide a level of protection up to £85,000 worth of cash savings per individual, per financial institution.

The FSCS only applies to funds that are saved within a financial institution with a banking authorisation. If you have savings of £85,000 or more with two different banks who are owned by the same institution with just one authorisation, for example if you have savings with Halifax and Birmingham Midshires, you are only covered for a total of £85,000. If you are with two banks under the same banking authorisation and your savings with those banks exceeds £85,000, it might be worth transferring the excess to an account with another bank or use National Savings and Investments which have 100% protection as they are backed by the UK Government. You can check your individual position for your deposits online on the FSCS website – Bank & savings protection checker | Check your money is protected | FSCS

There is a measure in place to protect temporary high balances for up to £1m for six months for some funds. There are a limited number of situations whereby you would have a qualifying temporary high balance, the most common of which would be money deposited to buy – or money received from selling – a main residence.

General savings for a property do not qualify, nor do transactions for property that is not your main home.

If you do wish to hold more than the FSCS limit but do not wish to open multiple accounts, you can use National Savings products such as the Direct Saver Account in the table above. While the interest rate is slightly off the best in the market, higher amounts can be held above the FSCS limit as they are backed by HM Treasury.