Spring Budget 2024

You will have already received our Old Mill Spring Budget Summary 2024 with the headlines of all the announcements in the budget earlier in March.

With the headline announcements effectively reduced to nothing more than a cut to National Insurance contributions, there was little of note for many of our clients. While billed as a tax cutting budget, with Income Tax allowances remaining frozen and a decrease in Dividend and Capital Gains Tax allowances, taxes may well increase for those who have finished working. According to the Institute of Fiscal Studies, the overall level of taxation in the UK is at its highest level in 70 years.

We have looked at how the announcements may impact you and have provided further detail of steps you may wish to consider.

19th March 2024

-

Gavin Jones See profile

Gavin Jones See profile

-

1. Income tax

In terms of general planning, investing couples should aim to use their dividend and personal savings allowances in full.

You should also try to arrange your investment holdings in such a way to ensure you fully use both personal allowances, personal savings allowances, dividend allowances and starting/basic rate tax bands.

Consideration can also be given to making Gift Aid payments to help save tax while helping good causes.

-

2. Dividends

The 0% dividend allowance means that, regardless of your tax rates, you can receive £500 dividend income from Saturday 6 April 2024 with no tax liability.

This has reduced significantly since the original £5,000 allowance introduced in 2016, before falling to £2,000 in 2018 and £1,000 last April.

-

3. Capital Gains Tax (CGT)

Another allowance falling is the CGT annual allowance. This was £12,300 in 2022 before falling to £6,000 last April and it will be £3,000 from the new tax year.

As a result of the reduction in the annual allowance, we think it will be more common to pay CGT in the future. While paying any tax can be galling, this may be one of the more palatable taxes given it is only payable on capital gain and the rates are half that of income taxes: 10% for basic rate taxpayer and 20% for higher rate taxpayers.

As part of the annual management of your portfolio outside of Individual Savings Accounts (ISA) or Pension wrappers there may be unintended consequences if we try and avoid paying CGT on gains. As you know we rebalance portfolios back to your original risk profile each year. If we do not do this, the resulting differences in investment performance could easily outweigh any tax saving.

-

4. Savings and investments

Investing within a pension and an ISA remains attractive as income, dividends and capital gains will not be subject to further taxation.

Ensuring you use your ISA allowance consistently becomes even more important now, especially where your dividend allowance is fully utilised. If we assume you hold £100,000 in ISAs in our medium risk portfolio compared to holding the investments directly and the interest and dividends earned remain the same, this could provide tax savings of over £2,400 in the next five years for a basic rate taxpayer and over £5,600 for a higher rate taxpayer.

-

5. The British Savings Bond

The British Savings Bonds will be delivered through National Savings and Investments with a launch date of early April. This product will offer a guaranteed interest rate, fixed for three years, increasing the savings opportunities available to consumers.

As soon as we get further details, we will review how competitive the rate is and include our thoughts in the next Insight.

-

6. UK Individual Savings Accounts (UK ISAs)

The Government also plans to launch a new UK ISA with a subscription limit of £5,000 which will be in addition to the current standard ISA subscription limit of £20,000. The new ISA will be a new tax-free product that will allow people to invest in UK focused assets.

A consultation document was released alongside the budget to determine which assets will be appropriate for the investment and this consultation will close in June. Once details have been released we will consider for your circumstances.

Income Tax

As well as the points above consideration ought to be given to maximising pension contributions which remain very efficient tax wise.

High Income Child Benefit charge

The High Income Child Benefit threshold is set to increase with a tax charge for the highest earner in a family with income between £60,000 and £80,000 from Saturday 6 April. The limit is based on ‘adjusted net income’ so pension planning and/or making gift aid payments can reduce your income for this purpose for those impacted and reduce the tax charge.

From next month, child benefit is £25.60 a week for the eldest or only child, and £16.95 a week for each additional child. For someone with two children who earns £80,000, there would be a tax charge of £2,212. Making a £20,000 pension contribution (costing £16,000) would mean self-assessment tax savings of £4,000 Income Tax and no child benefit charge of £2,212. So the effective cost of the contribution after the tax saved would be £9,788 or 51% tax relief.

Removal of Income Tax Personal Allowance

Pension contributions and Gift Aid can also reduce income below £125,150 which is the point where the personal allowance is lost completely. If income falls to £100,000 the personal allowance is fully reclaimed which is worth over £5,000 in saved tax. The tax relief in fully reinstating the personal allowance by making a pension contribution is 60%.

National Insurance Contributions (NICs)

The further reduction in the main rate of National Insurance for employees and self-employed individuals will be a welcome change with both employees and self-employed individuals will be better off.

According to the Chancellor, the average earner now has the lowest effective personal tax rate since 1975, although it was pointed out by the opposition that overall taxes in the country are the highest they have been for 70 years.

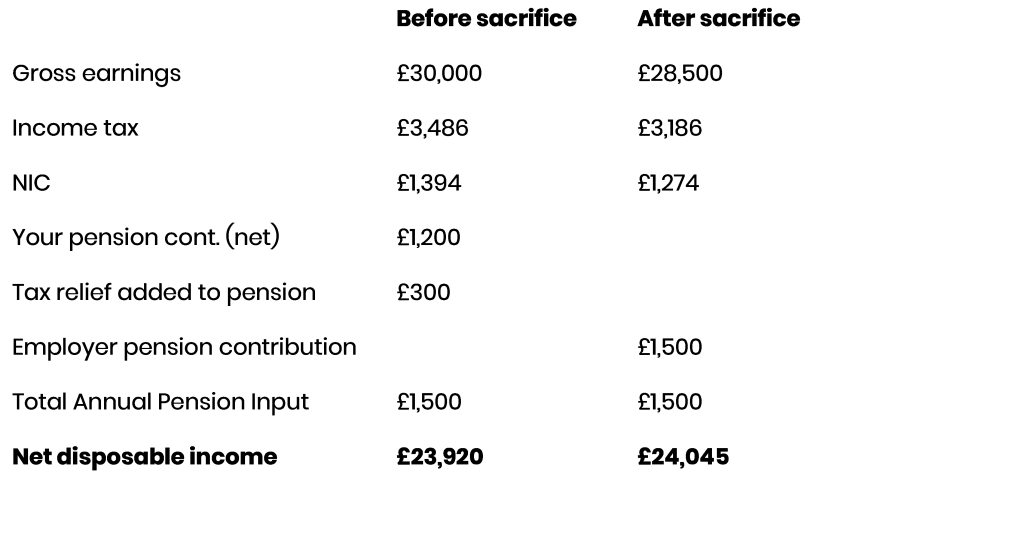

Employees should continue to consider salary sacrifice for pension contributions. Using salary sacrifice means that both the employee and the employer pay less NICs, so further tax savings can be achieved. Take an employee with a salary of £30,000. 5% pension contributions mean that £1,200 would be taken from their after tax salary (which will be £1,500 in their pension after tax relief is added). If they instead sacrifice £1,500 of their salary each year, their salary for tax and NIC purposes will be lower as the table below illustrates:

For those who already have salary sacrifice in place, it may become slightly less attractive as the tax savings will be less and a review of the agreement may be needed to ensure the same level of pension saving is maintained (or increased!).

Abolishing Class 2 NICs and reducing the rate of Class 4 NICs will also be a welcome change given it will save more for so many while still being able to get access to contributory benefits including the State Pension

Dividend vs salary

Business owners should ensure they are drawing income in the most optimal way. A remuneration structure review, in conjunction with their accountant becomes vital for the future.

This is especially so given the reductions we have seen to employee NICs in both the 2023 Autumn Statement and the 2024 Spring Budget and the increase in corporation tax for many businesses.

Shareholder directors should work with their accountant to review their remuneration structure, ensuring that they are drawing income in the most tax efficient manner. Creating a remuneration structure with the correct blend of salary, dividends and tax efficient pension contributions can make a significant tax difference to the after tax and NI outcome for shareholding directors.

With the relatively recent changes to dividend tax rates, corporation tax and the reduction in the dividend tax allowance together with the new changes to employee NICs, this review will be very important.

Almost every ’moving part’ in the decision-making process has recently changed or, in the case of employee NIC between the lower earning and upper earning limit, is about to change.

Capital Gains Tax (CGT)

Buy-to-let landlords who are considering making disposals of residential properties may want to consider deferring when CGT is due (usually the date of exchange) until after 6 April 2024 to take advantage of the reduction in the rate of CGT from 28% to 24% that will apply to gains made on disposals on or after that date.

Furnished Holiday Lets (FHL)

Historically, the commercial letting of furnished holiday accommodation has been treated as a trade so has benefited from a number of tax advantages:

- CGT reliefs for traders (Business Asset Rollover Relief, relief for gifts of business assets and relief for loans to traders)

- Plant and machinery capital allowances for items such as furniture, equipment and fixtures

- Profits count as earnings for pension purposes.

The abolition of the FHL tax regime from Saturday 6 April 2025 will mean that furnished holiday lets will lose this beneficial treatment.

Business Asset Disposal Relief (formerly Entrepreneurs Relief) means that any gain made on disposal of an FHL business would be taxed at just 10% but from 6 April 2025 they will be subject to the same rates of CGT on disposal as any other residential property of 18% or the recently reduced 24% rate.

Landlords of FHL properties will need to take tax advice on how best to structure their property investments following abolition of the current favourable regime.

Trusts

While there have been no changes to trust tax rates announced, the reduction of the CGT rate of disposals of property from 28% to 24% from Saturday 6 April 2024 will also be relevant to trustees holding property although this will be offset by the reduction in the CGT annual allowance, falling from a maximum of £3,000, to £1,500 or lower if the settlor has created more than one trust.

While not announced in the budget, there is a reminder below of the new rules coming into effect from 6 April 2024 for trusts, namely:

- Exemption from tax for trusts and estates with income up to £500. Where a settlor has made other trusts, the amount is the higher of £100 or £500 divided by the total number of existing trusts (subject to some exceptions)

- Removal of the default basic rate and dividend ordinary rate of tax that applies to the first £1,000 slice of discretionary trust income (i.e. the ’standard rate band’).

If you’d like to discuss the impact of the Budget announcements on your personal finances, please contact your financial planner.