The impact of currency movements on your portfolio

When we look at how global events impact on your investment portfolios, there are several factors that can impact returns, with currency being one of these.

11th August 2022

-

Gavin Jones See profile

Gavin Jones See profile

We have discussed before that currency movements can have a profound impact on equity valuations. Sterling, along with many other currencies has fallen against the dollar in particular over the course of the last year. The overseas equities that you own in your portfolio come with the currency exposure linked to those assets. A fall in Sterling has had a positive effect on non-UK assets that are unhedged. It is possible to hedge this currency risk and the decision whether to do this with growth assets is driven by a belief that hedging will deliver a greater risk-adjusted return. In practice the cost of hedging is a constant drag on returns and although hedging has been beneficial at times in history, Sterling has been gradually declining so on balance, leaving the growth assets unhedged is a sensible strategy decision for long-term investors.

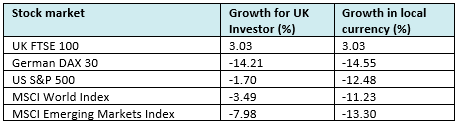

The table below indicates how overseas equities have performed this year to Friday 5 August. It includes the return of several indices – the UK main stock market; the FTSE 100 and representatives of German and US stock markets as well as a measure for global developed market stocks and Emerging Markets stocks. The return you will have received as an investor in an unhedged equity portfolio is on the left-hand side. The right-hand side gives an indication of the returns you may have experienced If we had hedged the growth part of the portfolio. Returns in local currency terms for each of the indices show you would have seen much bigger falls in the overseas equities.

Over this period, leaving the currency unhedged has reduced the fall in the value of your portfolio by limiting the fall in growth assets. As an example, for any exposure to US equities, which make up a large part of the global stock market, you will have experienced a fall of 1.7% this year because of the currency movement but the actual performance was a fall of over 12%. So, the performance improvement you will have experienced has been over 10% for that part of your portfolio.

At other times, the opposite can occur. If Sterling were to strengthen, we may see less growth or greater falls in value experienced in the overseas assets. Hedging carries a cost and as you can see at times paying that cost may also produce lower returns.

By contrast, the large swings in value currency can bring is undesirable in the defensive part of the portfolio. Here we have overseas bonds in the Global Short Dated Bond fund but the returns on this are hedged back into Sterling to mitigate any exposure to currency fluctuations. These are, after all, intended to be less volatile investments.