The importance of diversification in investment portfolios

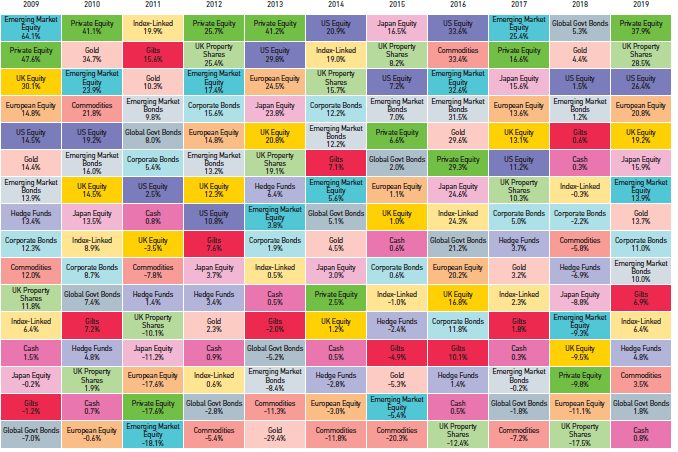

Even with a globally diversified portfolio, market movements can tempt investors to switch asset classes based on predictions of future performance. The table below clearly demonstrates that there is little predictability in asset class from one year to the next, suggesting that predicting future performance is a difficult if not impossible task. The chart makes a strong case for investors to rely on portfolio structure, rather than market timing, to pursue returns.

24th April 2020

-

Gavin Jones See profile

Gavin Jones See profile

Data source: © Seven Investment Management LLP 2018. All rights reserved

Portfolio structure - start with the why

It’s over 10 years since we started investing our clients’ money into portfolios that are managed directly under the governance of our own Old Mill Investment Committee. The drivers for managing our own portfolios remain the same as they were at the outset:

- Portfolios that are suitable for people like you – people who are planning or approaching retirement, retired or financially independent, and who want to grow their money over the long term

- Portfolios that are consistent with our investment philosophy, enabling us to provide effective delivery of investment advice, with the flexibility to create a solution tailored to your specific requirements, rather than a ‘one size fits all’ approach

- A robust investment solution that will stand the (unknown) tests of time, such as the current turbulence we have seen as a result of COVID-19.

Old Mill Investment Portfolios delivering real diversification

You may hear other investment managers say they’re diversified over hundreds of stocks. We believe we offer something truly different; at Old Mill our portfolios have over 12,000 securities across different asset classes, countries and investment styles.

The asset choices are split into those that form part of the ‘return engine’ of your portfolio and those that form part of the ‘defensive mix’. Your individual attitude to risk will determine the split of the funds in your portfolio between growth and defensive assets and as a result the extent of any positive or negative market movements over time. For example, someone with a lower risk portfolio will have seen lower falls since the start of the major stock market falls in February due to the higher weighting of defensive assets in their portfolio compared to someone with a higher risk portfolio.

Building the return engine of our portfolios

Some of the factors we consider when choosing asset classes for the growth part of our portfolios are:

- home bias – investing wholly in UK markets versus diversifying into overseas (developed) markets

- emerging – investing primarily in developed markets versus choosing fast-growing emerging markets

- factor tilts – investing into broad market indices versus tilting towards factors that can provide additional growth over time, including undervalued or smaller companies

- asset mix – whether we are choosing equities only or considering other assets

- currency mix – if we diversify overseas we introduce currency risk; a currency can gain or lose against sterling, and it’s possible to ‘hedge’ this (so the overseas currency is converted to sterling at an additional cost) or to leave this risk unhedged

- We leave currency unhedged in the growth part of portfolios. Movement of growth assets can be large and currency movement will be a part of this – both up and down – so hedging is less important.

Defensive asset considerations

For defensive assets we look at:

- Bond duration – bonds that have a short life (up to five years) have less volatility than longer dated bonds

- Credit quality – higher credit quality companies have less volatility than lower quality bonds. Credit quality is assessed by ratings agencies, with the most secure being AAA; UK Gilts, for instance, have a rating of AA

- Inflation risk – an enemy of bonds is inflation, which can eat away at value over time

- Currency risk – hedged or unhedged

- As the defensive assets aim to protect the portfolio we remove the currency risk by hedging.

As mentioned earlier, the resulting portfolio is highly diversified.

What we leave out of portfolios is as important as what is included. Many of the assets detailed as excluded in the graph above will be used by other investment managers, but we have good reasons for excluding them from our portfolios.

Conclusion

Rather than trying to speculate on the markets and predict future investment returns, our investment philosophy relies on a structured and patient approach to investing in a selection of asset classes that we believe will deliver strong results over the longer term and smooth out the impacts of any short term market crisis. This approach also removes the risk of making knee-jerk, emotional investment decisions that are based on current events as history shows that such decisions are often found to be wealth destroying not wealth creating.

If you’d like to know more about the approach we take to Financial Planning and our Investment Portfolios please talk to us.