Three key topics debated at the Investment Committee

The Investment Committee recently met and as usual was attended by our external Investment consultants who help bring insight, rigor and challenge to our discussions.

The role of our Investment Committee is to monitor the portfolios and ensure they remain robust and capable of delivering the investment outcomes we expect. It is no more important than at the present time when the performance we are seeing from equities and bonds is challenging. We are very conscious when we compare returns against rising inflation, that in the short-term, the portfolios have fallen short. It is important to not get too focused on the short term for as we have said on many occasions in the past, investing is a long-term pursuit however we still have to consider the current returns being delivered. There is insufficient space here to cover all the matters considered by the Investment Committee and therefore we have instead addressed three particular points that we covered in our deliberations which we feel to be very pertinent at the moment.

12th May 2022

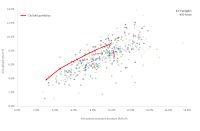

Overall, investors over the last few years have received a good absolute return from portfolios in line with the expectations we set out for the risk they were prepared to take on board. Looking back over the time we have been investing in our portfolios, they have stood up well against their competitors. The graph below compares the performance of our portfolios since we started to manage them on the current basis in 2009, against similar multi asset funds from 81 different investment managers available from June 2009 to March 2022 and comprises of 430 different funds. It considers the return achieved and the investment risk taken to achieve this. The red dots, emphasised by the red line are the Old Mill portfolios and reflects one of our key investment principles, namely that you should expect higher returns if you take on more investment risk.

When we compare the portfolios against other funds based on the investment risk they are taking, you will see from the table below that over the last 13 years, our investment strategy has stood up well.

| Portfolio | Funds beaten |

| Very Low Risk | 99% |

| Low Risk | 99% |

| Medium Risk | 96% |

| High Risk | 88% |

| Very High Risk | 77% |

It is easy, with the benefit of hindsight to find an asset class, or fund that has done better over different time periods. As an investment committee, it is incumbent on us to look back at our asset choices and consider how our portfolios have performed and whether our investment process can be improved on.

Source: Morningstar Direct

Rapidly increasing inflation and interest rates can present particular challenges for the assets making up the defensive element of investment portfolios. The key function in portfolios for defensive assets is to minimise volatility, however since the beginning of the year in the face of higher inflation and interest rates, bond yields have risen but this has caused bond prices to fall. Given the current climate of rapidly rising inflation and consequent pressure on interest rates to increase, we took the opportunity in conjunction with our external investment consultant to undertake a detailed review of our defensive assets to ensure we remain comfortable with our approach given the current economic backdrop we are operating within.

Defensive assets

In the last few years, we have faced some challenging choices when it comes to investing in bonds, not least because yields on bonds were at historical lows and below that of UK inflation. Owning high quality bonds to balance a portfolio against equity market falls will have reduced overall returns, but there was not much one could do to avoid this.

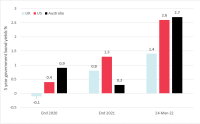

If you ask any investor if they would like higher or lower returns in the future, the answer is a given. Today the Bank of England’s base rate is still only 1%. Fortunately, short-dated, high-quality bonds in a number of major markets are now yielding in the region of 1.5% to 2.5% as yields have risen quite substantially since the beginning of the year, as markets have begun to reflect the risks of higher-for-longer inflation. The chart below shows what has happened to various global bond yields since the end of 2020. While this has caused falls in value in the short term, going forwards this will be beneficial with portfolios benefiting from the higher yields on these defensive bonds.

Figure 1: Bond yields have been rising fast

Data source: UK – Bank of England, US – Federal Reserve, Australia – Reserve Bank of Australia

Unavoidably, the short-term cost of securing higher yields is small capital losses on shorter-dated bonds. These smaller losses should be viewed in the context of the increased potential downside of higher risk equities at times of volatile markets and other bond alternatives. For a longer-term investor this should be seen as a price worth paying for higher future returns.

Although we have seen some capital losses, your bonds now have a higher yield going forward, which will compensate you for this loss over time and deliver a higher return thereafter. That is a good thing for any longer-term investor. So as an example, your bonds may have fallen in value from £100 to £97 in the last few months, but this will mean that instead of a 1% yield in the future you will be receiving 2%.

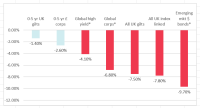

It is also worth noting that the yield rise impact has been materially less severe in high quality, shorter-dated bonds that form the majority of exposure in our defensive assets than for longer-dated and lower quality bonds, as the chart below illustrates.

Figure 2: Longer-dated and lower quality bonds performance in 2022

Source: Morningstar Direct YTD to 30-3-2022. * = hedged to GBP

The graph highlights the importance of holding high quality, shorter dated and lower yielding bonds as the backbone of our defensive assets. The blue bars represent lower quality but higher yielding bonds but as can be seen, the impact of rising inflation and interest rates has resulted in significantly higher capital losses.

Benefits of the short dated, high quality bonds held in our portfolios

Other portfolio managers have been tempted to exchange lower risk and lower yielding bonds in favour of higher yielding bonds in an attempt to squeeze some additional return out of what felt like an unproductive portfolio allocation.

As has been shown by recent events, this approach was unfortunately, an accident waiting to happen. It has always been Old Mill’s investment philosophy to hold bonds for their defensive characteristics, as insurance against the stock market falls we see from time to time. Retaining the lower risk characteristics of our bond investments is a core element of our investment philosophy and without this, there is a danger of our lower risk assets taking on the behaviour of riskier assets and in so doing, create potentially more uncertain investment outcomes for investors. We believe it is better to have the discipline of taking more quantifiable risk from equities and use the bond investments for the purpose for which they are intended, i.e., to help manage not create unnecessary risk.

The future

In reality, no one knows if yields will rise again, stay the same or fall. Remember that if there was any certainty in which direction yields should move, they would already have moved! If they do rise again, owners of bonds could see some additional falls in value, but they will end up in a better place with yet higher expected future yields. Patience and a long-term view are required. The shorter dated, high quality bonds we hold have performed relatively well compared to the longer dated bonds held by many other managers and you will benefit from the higher yields on the fund in the future.

While it is disappointing to have seen falls in these defensive assets the committee concluded we would not make any changes to the portfolios at present.

When looking at the current economic and political situation in the world, it is tempting to consider whether you should sell some of your investments in a flight to safety and go back in once everything is more ‘certain’. It is logical to want to be fully invested in the equity markets when they are going up and to be in cash when they are going down.

It has been our strongly held view that it is not possible to consistently make these decisions correctly which is why we prepare for a range of outcomes rather than try to predict what the future will bring.

In light of current market conditions however, we thought we should challenge this hypothesis with the help of our external investment consultants.

Remember that every decision to get out of equities also requires a decision on when to get back in, and vice versa.

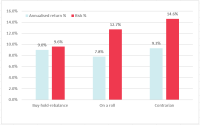

Our investment consultants, Albion provided a quick market timing experiment. They looked at the annual returns of the developed equity markets and cash from 1972 to 2021 and considered three naïve strategies.

Buy-hold-rebalance: this simply takes 50% of the equity return and the cash return every year.

Market timing strategy 1 – ‘On a roll’: if the previous year’s equity return is higher than the median return of all years, allocate 100% equities, if not allocate 100% to cash.

Market timing strategy 2 – ‘Contrarian’: if the previous year’s equity return is lower than the median return of all years, allocate 100% equities, if not allocate 100% to cash.

Figure 3: Results of the market timing experiment – 50 years to 2021

Data source: MSCI World Index (net. Div.) in GBP plus UK 1 month T-Bills (cash), from Dimensional Returns Web © All rights reserved. No costs deducted of any kind. This analysis is for illustrative purposes only.

So, the return from a process similar to ours is an annualized return of 9% per annum over the last 50 years, with a risk of 9.6%. The ‘on a roll’ strategy has provided a lower return and while the ‘contrarian’ strategy gave a slightly higher return, this was achieved at a much higher volatility.

From this limited and somewhat basic experiment, it demonstrated that for this period of capital market history, the timing strategies would have yielded little return benefit, but with materially higher risk, as measured by portfolio volatility. Market timing strategies, in real life, may come with other material risks and costs, such as time out of the market when buying and selling and thereby missing the few days that make a major contribution to positive market returns, incurring the transaction costs of buying and selling and potential tax consequences.

According to Dimensional Fund Advisers, from 1990 to the end of 2020, US$1,000 invested in the US equities (S&P 500 Index) would have grown to around US$20,451. Yet missing the best 15 days throughout this whole period delivered around US$7,080. Missing the next 10 best days reduced the growth to US$4,376. Cash returned US$2,245.

There are no simple ways to time markets. The temptation is to believe that some other professional fund managers have complex models (or intuitive skill) that allow them to do so. Unfortunately, research suggests that these skilled managers are few and far between.

Conclusion

Time in the market is preferable to timing the market for longer-term investors seeking a successful investment experience.

If you want to discuss your own circumstances with your Old Mill Financial Planner do get in touch with them.