Trusts & Inheritance Tax

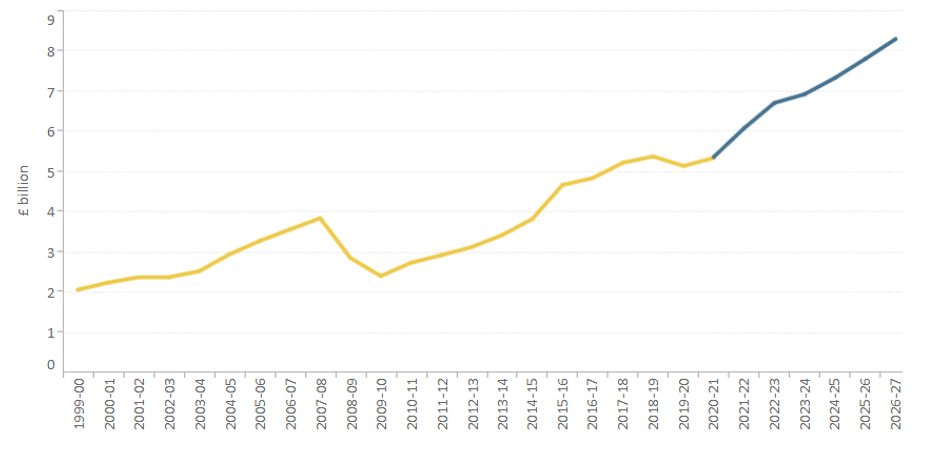

Inheritance Tax (IHT) receipts have been rising for over a decade and the trend is set to continue, according to Government statistics (as shown in Figure 1 below right).

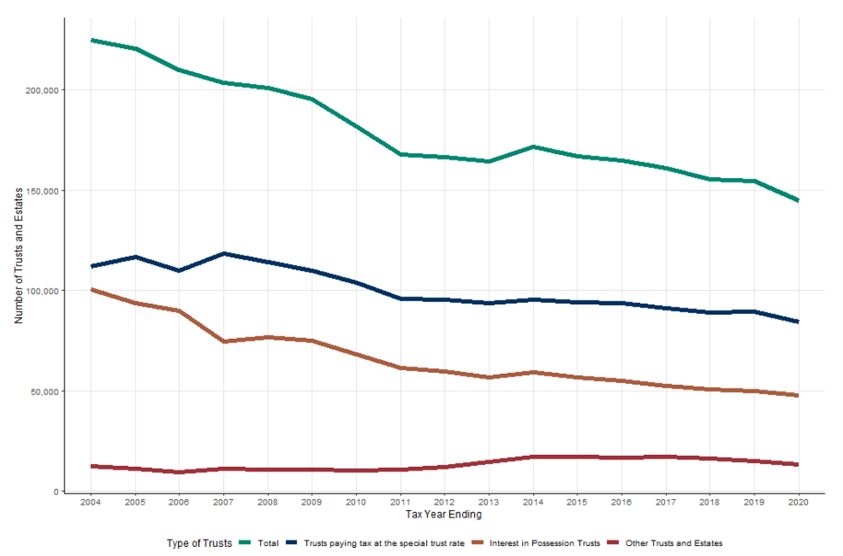

At the same time, the number of trusts being used is falling which is an interesting phenomenon given how effective Trusts can be in tax planning (as shown in Figure 2 below right).

20th July 2022

-

Gavin Jones See profile

Gavin Jones See profile

When speaking to clients about trusts, usually the main barrier is the lack of familiarity and understanding of how they work. A common misconception is that they are seen to be hugely complicated or solely for the very wealthy which is usually not the case.

In November last year, the Treasury, in response to the Office of Tax Simplification (OTS) review of IHT, confirmed that they had decided ‘not to proceed with the recommendations at this time’. Some of these recommendations dealt with gifting and the use of trusts.

This means the IHT planning landscape currently remains unchanged, and lifetime gifting into trusts remains a key part of tax-efficient family wealth preservation.

We discussed the basics of trust planning in our last printed Wealth Management Insight at the beginning of the year.

Figure 1: Inheritance tax receipts and forecast

Source: ONS, OBR March 2022

Figure 2: The number of trusts and estates continues to fall across recent years

Source: HMRC

Having decided how much you wish to gift, the next consideration is whether to simply give the funds outright or whether to take advantage of the protection afforded by the use of a Trust. There may be very good reasons why an outright gift may not be appropriate for example, the person receiving the funds may be very young or perhaps financially naïve or rather than benefiting just one person, the gift is intended to be enjoyed by a group of people, such as grandchildren, or later generations. A Trust can provide a very effective vehicle to hold the gift securely and provide control over how the funds can be used and who will benefit from them.

Different types of trust are available to deal with different situations.

There are broadly three types of underlying trust for anyone looking to make a gift with each giving differing levels of control:

- Absolute trusts – These are very simple trusts that specify an individual who will benefit and when. Typically, these will be used for children to hold assets until they reach the age of 18.

- Flexible trusts – A common type of flexible trust is an Income in Possession trust where the trust has named beneficiaries who will receive the income generated from the trust’s assets for their lifetime. When the beneficiaries die, the trust capital can then be passed to other beneficiaries. An example of this may be for a spouse to leave assets to their surviving spouse for them to receive income while they are alive, but the capital is protected so on their subsequent death the trust assets will then pass to their children.

- Discretionary trusts -These are the most flexible type of Trust, with usually a broad class of people included who can potentially benefit from the trust. An example is a family trust where the assets are initially available to be used for your children for example to help meet educational costs and then perhaps house deposits etc. As and when grandchildren come along, they could also benefit from the Trust as well which helps with passing funds down through the generations. This is a very effective vehicle for helping with inter-generational planning.

If you feel a Trust may have a role to play in your own planning, your Financial Planner will be able to guide you on the best way of setting up the Trust and how to use it to its full effect having regard to the beneficiaries, the control and flexibility you seek and of course tax.

In a later edition we will cover in more detail different types of trust planning, their key points and set out case studies of how these trusts work in practice.