US ‘exceptionalism’ – resilient reality or risky illusion?

4th June 2025

-

Gavin Jones See profile

Gavin Jones See profile

For more than a decade, the U.S. stock market has outperformed nearly every other major equity market. This outperformance has been driven in large part by a handful of dominant technology firms such as Meta, Google, and Microsoft. The so-called ‘Magnificent 7’ accounted for just under 7% of the total value of U.S. stocks at the end of 2014, but by the end of 2024, that figure had risen to 28%[1]. In 2024 alone, the ‘Magnificant 7’ delivered a return of 48%, while the remaining 493 companies in the S&P 500 returned approximately 16%. In contrast, global markets excluding the U.S. returned only about 5% (in USD terms)[2].

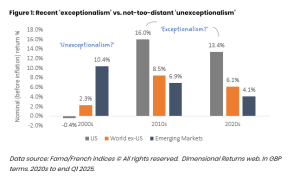

This relatively short time frame, particularly when measured against the long investment horizons of most investors, has led some to proclaim a new era of ‘US exceptionalism.’ This term refers to the belief that U.S. economic and corporate fundamentals are uniquely strong and enduring relative to other markets. However, some observers appear to have short memories. U.S. equity market performance in the 2000s, often referred to as the ‘lost decade,’ was anything but exceptional following the collapse of the dot-com bubble.

In hindsight, many might wish they had allocated more to U.S. stocks in the last 15 years or so. But, without the benefit of foresight, it is impossible to predict whether this period of exceptionalism will continue – and if so, for how long.

Looking ahead, several significant factors could challenge the sustainability of U.S. market dominance. Geopolitical tensions are intensifying. A potential return to American isolationism – particularly under a second Trump administration – raises uncertainties. Ballooning deficits and a national debt now exceeding $37 trillion present additional risks. Competition in AI, chip making, EVs from China and elsewhere are material threats too. Meanwhile, the global financial system’s reliance on the U.S. dollar as its reserve currency could eventually be tested.

At the present time, no credible alternative to the dollar as a reserve currency currently exists and this gives unique benefits that the U.S. enjoys due to the dollar’s dominance. This status helps suppress interest rates, lowers corporate funding costs, and attracts continuous inflows of foreign capital into American financial markets.

The future remains highly uncertain, with many plausible scenarios and a wide range of views about which are most likely. Fortunately, for individual investors who trust that markets are broadly efficient, we can rely on the collective intelligence of the market for guidance. It processes this vast, complex web of scenarios, risks, and probabilities, and distils them into a single figure: the price of each stock and, in aggregate, the market itself.

Rather than trying to predict whether U.S. exceptionalism will continue, we can take a neutral stance, neither moving overweight nor underweight in U.S. equities based on short-term narratives. This neutrality reflects the collective wisdom and aggregate expectations of all market participants.

Ultimately, by avoiding market timing – a strategy with a poor track record according to substantial academic evidence – and remaining diversified through well-structured, low-cost systematic funds, investors increase their odds of achieving strong outcomes.

As always, if you have any questions your Financial Planner will be pleased to hear from you.

[1] https://siblisresearch.com/data/us-stock-market-value/ accessed on 28th May 2025

[2] ‘Mag 7 Gravity’, By Wes Crill, PhD, Kevin Green, PhD 01 April 2025 see www.dimensional.com accessed on 28th May 2025