Why cash feels safe, but may hold you back

12th February 2026

-

Gavin Jones See profile

Gavin Jones See profile

It’s always a good idea to keep cash for short-term needs, and many of you keep more cash than is strictly necessary. If it is not derailing your long-term plans, then that is probably fine. We know that over long periods of time, there is a risk that cash can lose value against inflation. With inflation increasing over the last few years, you could consider whether the cash you hold is working hard enough for you.

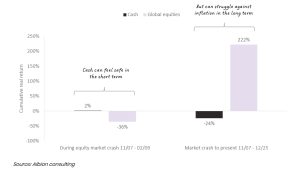

This may involve reviewing the interest rate you receive, as many high street banks have savings accounts with interest rates well below inflation. The long-term impact of this is shown below.

While it can feel reassuring to have an asset that ‘doesn’t fall in value’ in the short term – illustrated above by cash protecting value in the financial crisis from 2007 to 2009, you can see that over the long term, cash can lose value against inflation.

Risk aversion and overreliance on cash

A recent study by JP Morgan identified a number of reasons why people might be reluctant to invest and prefer to keep their savings in cash. One of the main findings was that people are attracted to cash as a means of long-term savings. Holding too much cash means that you are missing out on the higher returns available if you invest and are likely to struggle to keep pace with inflation.

The survey found that some people expect cash to deliver better long-term returns than stocks, despite history evidencing that this is not the case, with some respondents stating they were afraid of losing money if they invested.

The impact of holding cash can be evidenced by looking at the returns on investing in a global portfolio of stocks versus cash since the COVID pandemic.

A global portfolio of stocks would have returned 39% in real terms (after inflation). With cash, you would have lost 9%.

Overreliance on housing

Another factor that emerged strongly from the survey is that experience has caused consumers to place too much reliance on housing wealth and not therefore see the need to invest their cash.

A large proportion of respondents to the survey expected house prices to rise by more in the next 25 years than the 200% they have in the past 25 years.

In theory, house prices should rise broadly in line with average earnings: after all, a house is only worth what someone is able to pay for it. This relationship broke down over the past 25 years for two reasons.

Firstly, deregulation of the banks and lower interest rates allowed people to borrow more for a given level of earnings.

Secondly, very low housebuilding and relatively high migration created a supply-demand imbalance that forced people to devote more of their earnings to buying or renting a home.

The tide has now turned. Regulation has focused on tying lending back to earnings, rather than to the value of the house, while interest rates look set to remain higher, limiting borrowing. Correcting the supply-demand imbalance is a cornerstone of the current government’s growth strategy, with very ambitious homebuilding targets now in place.

People are thinking about retirement too late

The repayment of student loans and buying their first home impacts people’s ability to save for retirement.

Those who do save are leaving their savings in cash because they don’t plan on retiring for a long time and have therefore not considered the benefits of saving now.

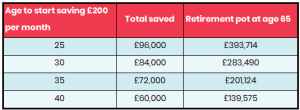

That means they are missing out on one of the best tools available to savers, the long-term benefit from compounding. Based on certain assumptions, an individual who starts investing £200 per month in stocks at age 25 would have almost three times as much upon retirement at 65 as someone starting to save the same amount 15 years later.

Source: Unbiased

Consumers lack the knowledge and confidence to make decisions about deploying their savings

The mood of the JP Morgan survey can be summed up as ‘Saving is good, investing is scary’. Much of this is linked to the fact that people lack confidence about how much to save and where to save it.

This is where Old Mill can help in providing the knowledge and solutions to give people the confidence to invest.

High expectations of the state

The survey highlighted widespread optimism about the role the state will play in supporting people’s retirement, with many believing the state will be equally or more generous when they retire compared to today.

This may well be overly optimistic, with the government finances already under pressure and an ageing population that will only increase the reliance on the state. Those aged over 80 are the biggest beneficiaries of state support, and this cohort is growing fast.

Sole reliance on the state to provide for retirement is therefore a very risky approach to take.

Summary

UK households are saving, but keeping their savings in cash, for many of the above reasons, is not an approach we would recommend.

Please do speak to your financial planner about the benefits of long-term investing over holding your savings in cash.

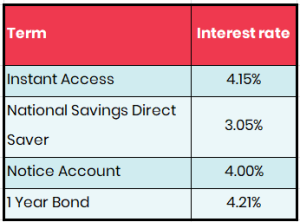

Current interest rates

Looking at rates at the time of writing (on 9 February), an indicative sample of the rates you can secure at present is as follows:

Source: Moneyfacts.co.uk 09.02.26

We have not included institutions in the table above as rates change quickly. If you wish to review the interest rates you are getting currently, please do speak to your financial planner.

Cash management services

For those holding larger amounts on deposit, a cash management service may be worth considering. They offer potentially higher interest rates with deposits fully protected and much simpler administration than where accounts are held directly with institutions.

These are essentially platforms to help manage cash deposits and allow you to easily switch between different deposit accounts without having to go through the arduous account-opening process each time.

For those with a larger short-term deposit or entities such as Trusts, pension funds, and companies where opening accounts is more difficult, using a cash management service can greatly simplify the ongoing administration and make it far easier to ensure the overall rate of interest remains competitive.

When you are dealing with a large sum of money, while the interest rate is important, so too is ensuring the deposit is protected by the Financial Services Compensation Scheme (FSCS) in the event an institution becomes insolvent. For individuals, this is £120,000 (£240,000 for a couple), and for entities like Trusts or some companies, this is £120,000 per institution. Opening multiple accounts to ensure the funds remain fully protected by the FSCS can be extremely onerous, especially for Trusts and companies.

If you would like to review the interest rates you are getting currently or want to know more about our cash management service, please speak to your financial planner.