Employer Class 1 National Insurance update

The 2024 Autumn Budget announcement brought significant changes to Employer Class 1 National Insurance (NIC) and other related contributions, effective from April 6, 2025. These changes have a profound impact on small businesses, and understanding their implications is crucial for effective financial planning.

Here we look at the details of the changes and offer insights for employers and self-employed individuals.

8th July 2025

-

Matthew Jackson See profile

Matthew Jackson See profile

Employer Class 1 National Insurance (NIC)

As an employer, you previously paid 13.8% Employer Class 1 National Insurance (NIC) for employees earning over £9,100 annually. Since April 6, 2025, the following changes have taken effect:

Increase in contribution rate:

From 13.8% to 15%.

Lower secondary threshold:

The threshold for paying Class 1 NIC has reduced from £9,100 to £5,000.

Impact on small businesses

Small businesses, which enjoyed a £5,000 employment allowance against their NIC liability, have seen this allowance increase to £10,500. Moreover, the existing £100,000 liability threshold for claiming this allowance has been removed, making it accessible to more businesses.

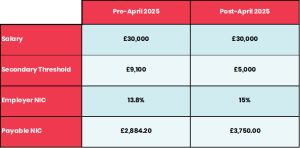

To understand the financial impact of these changes, let’s consider a practical example:

To understand the financial impact of these changes, let’s consider a practical example:

Result: An additional NIC cost of £865.80 per employee earning £30,000.

However, businesses with fewer than six employees earning similar salaries may offset these costs due to the increased employment allowance, potentially benefiting smaller organisations.

Changes for the self-employed: Class 2 and Class 4 NIC

Self-employed individuals have also experienced adjustments to their NICs:

Profits under £6,725:

– No obligation to pay NIC.

– Class 2 contributions can be made voluntarily to qualify for a State Pension year.

Profits between £6,725 and £12,570:

– No Class 4 NIC is payable.

– Class 2 is treated as paid, ensuring a qualifying year for State Pension.

Profits between £12,570 and £50,270:

– No Class 2 NIC is payable, but treated as paid.

– Class 4 NIC of 6% applies to profits over £12,570.

Profits over £50,270:

– Class 4 NIC of 6% on profits up to £50,270 and 2% on profits exceeding this amount

For the 2024/25 tax year, the Class 2 NIC rate is set at £179.40 annually.

Exemptions to note

- Employees under 21: No employer NIC for salaries up to £50,270

- Apprentices under 25: NIC exemption applies up to £50,270

- Veterans: Employers hiring veterans can benefit from a similar exemption

- Freeports and Investment Zones: Employers in these areas maintain a higher salary threshold of £25,000 for NICs, subject to specific criteria such as location and employment start dates

What this means for your business

The changes aim to balance contributions with allowances, benefiting small businesses while imposing higher costs for larger workforces. Employers with fewer employees may find the increased employment allowance advantageous. Meanwhile, self-employed individuals must consider the revised thresholds and rates when planning their finances.

We’re here to help

These changes can be complex. If you’re unsure how the new regulations will affect your business, consulting a financial adviser or tax expert is highly recommended. Get in touch here