Getting the best from your savings

Last week, the Bank of England increased UK base rates to 1%. This was the fourth consecutive increase and brought interest rates back to a level last seen in March 2009.

In the Monetary Policy Committee meeting minutes, it was interesting to see predictions that CPI inflation is expected to rise further over the remainder of 2022, to just over 9% in 2022 Q2 and is expected in peak at just over 10% at the end of this year. The Bank attributes most of the increase to higher household energy prices following the big rise in the Ofgem price cap in April and a projected additional large increase in October.

12th May 2022

Cash is the cornerstone of financial planning

While interest rates remain significantly below inflation, Banks or building societies remain a safe place to keep your cash in the short term. Keeping enough money easily accessible on deposit should always be one of the foundations of your personal financial plan.

Although you should be holding adequate reserves of cash to meet expenditure requirements to avoid having to sell investment funds, historically over longer periods of time, the return on deposits struggle to keep pace with inflation and this is starkly seen at the moment.

Deposit rates

One of the benefits, if it can be called that, of the increase in interest rates is a rise in the rates being offered currently on savings accounts. The table below provides indicative maximum rates you can get as of Monday 9 May.

| Term | Interest rate |

| Instant Access | 1.5% |

| National Savings Direct Saver | 0.5% |

| Notice Account | 1.2% |

| 1 year bond | 2.05% |

Source: Moneyfacts.co.uk 09.05.22

We have not included institutions in the table above as rates change quickly. If you wish to review the interest rates you are getting currently then do speak to your Old Mill Financial Planner

Safety of your money

Banks have been under intense scrutiny since the credit crisis in 2008 and The Financial Services Compensation Scheme (FSCS) was established to provide you with a level of protection up to £85,000 worth of cash savings covered per individual or business, per financial institution.

The FSCS only applies to funds that are saved within a financial institution with a banking authorisation. If you have savings of £85,000 or more with two different banks who are owned by the same institution with just one authorisation, for example if you had savings with Halifax and Birmingham Midshires, you are only covered for a total of £85,000. If you are with two banks under the same banking authorisation and your savings with those banks exceeds £85,000, it might be worth transferring the excess to an account with another bank or use National Savings and Investments which have 100% protection as they are backed by the UK Government. You can check your individual position for your deposits online on the FSCS website – Bank & savings protection checker | Check your money is protected | FSCS

There is a measure in place to protect temporary high balances for up to £1m for six months for some funds. There are a limited number of situations whereby you would have a qualifying temporary high balance, the most frequent of which would be money deposited to buy – or money received from selling – a main residence.

General savings for a property do not qualify, nor do transactions for property that is not your main home.

Making sure your money is working hard for you

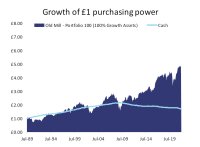

One of the key results we want to achieve for our clients is to at least maintain the real value of their wealth, i.e., after the impact of inflation. While cash sometimes has the ability to do that, there are long periods in history when it has lagged behind inflation. You can see in the graph below that since the financial crisis in 2007-09 the purchasing power of cash has fallen while growth assets – equities have risen.

The return after inflation for cash will only get worse as this year goes on, with inflation predicted to reach 10% by December when you can see above that even the best interest rates are significantly below that.

Make sure you have enough in cash that you are comfortable with and to deal with unexpected emergencies. But if you are holding more cash than you need then do speak to your Old Mill Financial Planner about the options open to you.