Investing over the last 70 years

The first weekend in June saw the country come together to celebrate Her Majesty Queen Elizabeth’s Platinum Jubilee. During her 70-year reign, the United Kingdom, and indeed the world, has seen many changes. Here we look at some of the key changes in the world of finance, and in particular with investing and pensions since 1952.

24th June 2022

-

Gavin Jones See profile

Gavin Jones See profile

For those that remember the 1950s, the world was a very different place. With the War years only just over and the great depression still fresh in peoples’ minds, habits were built around saving for a rainy day and the belief that you might have to go without.

Most people’s interaction with mainstream finance was with a bank and even then, only to buy a property. Having any other debt was frowned upon, although for many to buy essentials it was necessary to pay the Tally Man – credit for goods that would then be repaid weekly to the man coming to your house.

Credit has seen a big change over the last 70 years with mail order catalogues, hire purchase and then credit cards and loans becoming mainstream over time. Even mortgages became easier to obtain with smaller and smaller deposits necessary, or at least until the financial crash in 2007 – 09.

Banks themselves have changed dramatically with the disappearance over time of the traditional bank manager, the rise of cash machines first introduced in 1967 and then the rise of online banking which started to appear in 1997.

A big part of the change on people’s finances has been the increase in home ownership and the rise of house prices. At the start of the Queen’s reign, less than 40% of houses were owned by their occupiers, rising to over 70% just before the financial crisis in 2007 before falling to the current level of about 65%. With average house prices under £2,000 in 1952 they are now over 100 times higher at £278,000 and even adjusting for inflation have risen over 400% over this time.

As society has changed habits have changed too, with eating out, fast fashion and foreign holidays becoming much more common. Today people are offered credit at every turn, with the latest innovation being the rise of buy now, pay later firms.

As we sit here today with the ability to access real-time valuations on our investments, at any time it is almost impossible to conceive how much the finance and investment landscape has changed over the last 70 years.

The 1950’s

In 1952, before Premium Bonds, cash machines, mobile phones, and real-time pricing for stock trading existed, Nobel Prize winner Harry Markowitz, one of the grandfathers of modern portfolio theory coined the phrase ‘Diversification is the only free lunch in investing’ – a man ahead of his times and still one of our core investment beliefs today.

Far fewer people owned shares at the time when the Queen was crowned. Trading of stocks took a considerable amount of time and the absence of technology limited the ability to easily trade in companies of other countries. Moreover, even in the mid 1960’s investing was still limited to a small percentage of the population – around 3.3%1.

The reality back then was that diversification was much harder to achieve than it is now. For example, the main UK stock market index, the FT30, comprised of only 30 companies, the members of which were selected by journalists at the Financial Times to represent companies that were significant to the UK economy at the time, and was primarily dominated by shipbuilders, carmakers and textile companies.

The 1970s

Innovations in investing accelerated in the 1970s and many of the foundations for today’s environment were laid. Investing in this period was difficult and characterised by ‘Stagflation’ – high inflation and stagnant economic conditions.

1974, saw the introduction of the Market Price Display System for the London Stock Exchange to enable brokers access to real-time prices for more than 700 leading securities. However, it was not until 1984 that the FTSE100 was launched, in partnership with the Financial Times, creating an index of the 100 biggest companies by market capitalisation. Today, 70% of the revenues generated by companies in the FTSE100 are earned outside of the UK.

Through this period, we saw developments in investment funds. Rather than individuals holding individual stocks, fund managers would package together a larger number of companies and would oversee the investment – buying and selling if necessary. In 1976 we saw the first retail index fund launched by Jack Bogle – the Vanguard 500 that bought and held the largest 500 US companies.

Financial advice was largely delivered by Insurance companies, with huge sales forces selling their own products. Unfortunately, the period was marred with scandal, with the launch of a personal pension in 1988 leading to many being misadvised to transfer their company scheme and losing valuable guarantees. This led to a pension review by the regulator in 1994 alongside compulsory exams for advisers.

The 2000’s

Today, the internet dominates investing. With the rise of personal computers and now smartphones, it is easier than ever before to research, buy and monitor investments. While the speed of trading has gone up, the cost has come down and trading fees are considerably lower than in the past. Conversely the volume of trades over the last twenty years have been much larger than in the first part of the Queen’s reign.

The internet has also made it much easier to trade on overseas companies and it is normal now for a diversified portfolio to have a large part of overseas securities.

The advice landscape has also changed dramatically with modern advice firms moving away from insurance company influence to offer a much wider range of services more in tune with the interests of consumers.

The future

The future of investing presents both an opportunity and a challenge to financial professionals who must introduce the value of advice to a new generation of investors.

Younger affluent investors have grown up with a more self-directed approach. It is easy to opt for any number of digital platforms that offer convenient access to trading and an expanding range of alternative investments, from cryptocurrency to business start-ups.

Making sense of the vast landscape of options is crucial to pursuing a good investment outcome and experience. In a future of expanding product choices and rising complexity, we believe that qualified, trusted financial planning will prove more valuable than ever before.

Long term returns

While the landscape has changed dramatically from a return’s perspective, since the beginning of 1952 until 30 May 2022, UK equities have returned 11.7% a year.

The recent stock market volatility we are experiencing is nothing new. When we look at UK equities in isolation over the last 70 years, they fell in value in 18 of those years and underperformed cash in 26 years, perhaps demonstrating something we talk about often – investing with a long-time horizon is a key part of your planning.

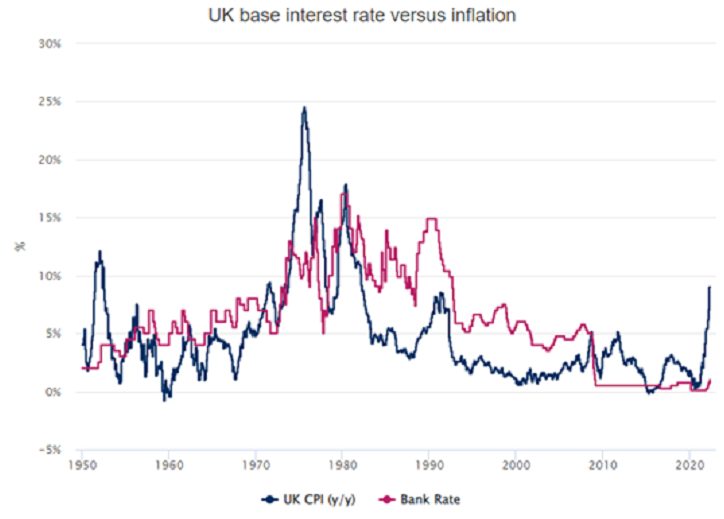

Interest rates and inflation

The graph below shows interest rates and inflation over the last 70 years and whilst the circumstances and reasons for today’s relatively high inflation rate of 9.1% (May 2022) differ from the post-war environment of 1952, it’s interesting that in June 1952, inflation was 10.5% and interest rates were then 4%, compared to the current Bank Rate of 1.25%.

Note: The base interest rate is the Bank of England’s main policy rate, or ‘Bank Rate’. CPI, or the Consumer Price Index, is a measure of consumer inflation in the UK. This measure has been published since 1989 and the figures between 1950 and 1988 are based on a ‘historical modelled series’ published by the Office for National Statistics. (Source: Refinitiv, Office for National Statistics, Schroders as at 5 May 2022)

State pensions

In 1952, the basic rate state pension was £1.63 a week for a single person and £2.70 a week for married couples. Today a single person receives £141.85 a week and married couples get £226.85. Whether you are single or married that is an increase over the last 70 years of more than 8,000%! Moreover, the state pension has more than kept pace with inflation. If it had only kept pace with inflation, the weekly amounts would now be £32.12 and £52.92.

However, it is also worth considering that back in 1952 most people did not make it to the state pension age – life expectancy of a man was 44 and for a woman it was 47, whilst the state pension age was 65 for men and 60 for women. Today significantly more of us live to claim our state pension.

At the same time, the state pension of today does not represent as much of the average wage as it did back in 1952. This means that pensioners today tend to have to rely more on other sources of income, such as their workplace pensions or investments to maintain the same standard of living they have enjoyed during their working lives.

Workplace pensions

The world of pension schemes has seen seismic changes since the 1950s in conjunction with changes in working practices. Pensions were introduced around this time to reward workers who would often work for the same company for 40 years or more. Larger companies were involved in the rise and subsequent fall of Defined Benefit (DB) / Final Salary plans which pay a secure income for life based on salary and years of service. But increasing regulation and costs after the Robert Maxwell pension scandal in the early 1990s, alongside greater mobility in the workforce and the end of jobs for life started the move to Defined Contribution (DC) pensions. The income you receive is less certain and dependent on the pension scheme value which is determined by the value of contributions and the investment returns made. Increasingly in the future we think working with a financial planner will give the best chance of a successful retirement.

Automatic enrolment in workplace pensions was introduced in 2008 and as a result it is estimated that 79% of employees now participate in a workplace pension – also by default increasing the number of people who in some way are invested in stocks and shares.

As recently as 2015, we saw the introduction of Pensions Freedoms – allowing people more choice in how they access and draw money from their pensions.

1 Cited in Vernon, Middleton and Harper, ‘Who owns’ London Stock Exchange Fact Books, 1965