Market commentary

In a reminder that no one has a crystal ball, the ‘most anticipated global recession in history’ has not arrived yet. Thinking back to the beginning of the year, economists, including the Bank of England were almost unanimous in their forecasts for a recession in the US, UK, and Europe early in 2023. To date only Germany, of the major countries, has recorded two consecutive quarters of negative growth and therefore is technically in a recession.

In the UK and Europe, winter turned out to be warmer relative to long-term averages and expectations. This reduced the demand for energy for heating and punctured the price of natural gas that had been squeezed up aggressively in response to supply reductions from Ukraine and Russia.

Consumer spending on both sides of the Atlantic was also underestimated. Extra savings that were accumulated during COVID lockdowns and through wage increases are being spent on services and experiences for longer than anticipated. The demand for goods however has dropped and looks set to continue with the cost-of-living crisis including weak housing markets which are having to cope with much higher interest rates for new mortgages.

16th June 2023

-

Gavin Jones See profile

Gavin Jones See profile

The FTSE 100 Index continues to lag other developed equity markets and is just about clinging onto gains for the year so far. Its fortunes have not been helped by weak commodity prices. The oil price, a key determinant of the fortunes of companies such as Shell and BP, has fallen from a high of $120 last year to $75. Other commodities have also fallen impacting on the large mining companies BHP, Rio Tinto, Glencore and Anglo American. The pound’s recovery against the dollar and the euro has reduced the sterling value of overseas profits. These are factors out of the control of the companies themselves.

Germany drifted into a recession in the first quarter of 2023, weighed down by a tough domestic property market and a global manufacturing slowdown. This is only part of the story as eurozone unemployment as a whole, hit a new record low in April and May’s inflation data for several of the large countries was lower than forecast pointing to a more resilient economy for the euro area.

The US stock market as measured by the biggest 500 companies (S&P 500) is higher since the beginning of the year, thanks largely to the contributions of potential artificial intelligence winners including Nvidia in particular as well as Microsoft, Alphabet, Meta, Amazon and Apple. The technology heavy NASDAQ Composite Index has risen by 24%.

One of the greatest disappointments of this year has been the lacklustre nature of China’s recovery. The abrupt ending of its zero-Covid policy was expected by many to lead to faster growth, but structural issues including the highly indebted real estate sector and stagnant population growth have been strong headwinds.

The stock market as measured by the MSCI China Index is down 9% year-to-date and has fallen 22% from its January peak. Investors will be torn between the potential opportunity of a huge and growing middle class in China and the potential disruption by the ongoing tensions with the US in particular.

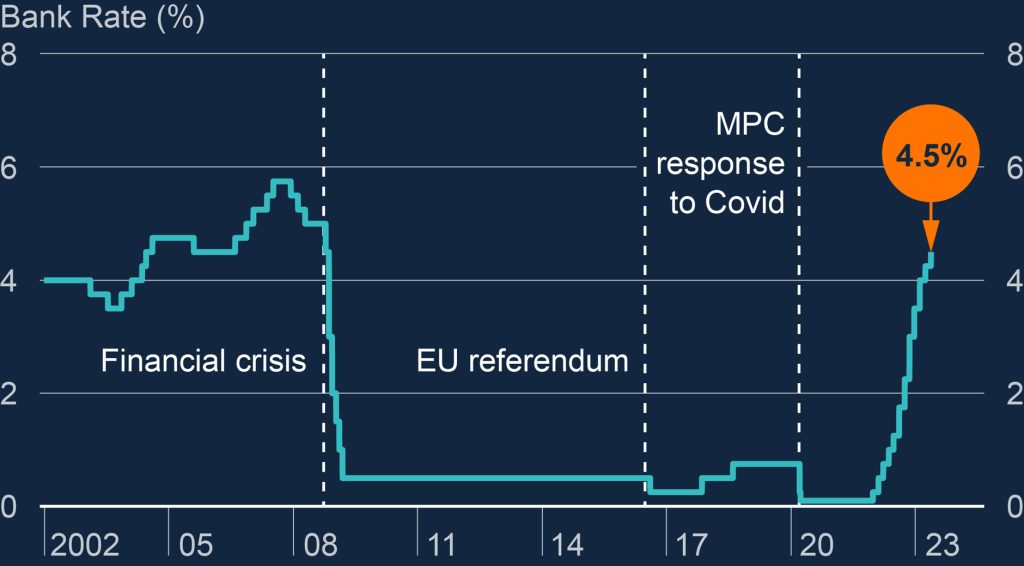

Higher for longer inflation, in the UK in particular, has impacted the expected path of interest rates. At the start of the year, predictions for the UK base rate showed a peak at around 4.7%. Since then, expectations have increased for the peak to be above 5% later this year.

Base rates have increased rapidly since December 2021, as shown in the graph below.

Source: Bank of England Monetary Policy Summary, May 2023

In the US, it is thought we are nearer the peak in interest rates, if not there already but that the forecasted rapid rate reductions in the second half of the year are no longer on the radar.

The world is having to learn to live with higher interest rates but one of the impacts of this will be higher bond yields which will benefit you as an investor. The yield on the Global short dated bond fund we use is now 4.7%.

Please speak to your financial planner if you want to discuss your portfolio.