We need to speak about pensions

From April 2027, pension funds will be included in estates for inheritance tax (IHT) purposes so potentially subject to tax at 40%, or more on death. It has been widely covered in the media and especially the practicalities of families having to deal with more complex administration while grieving. The new rules will affect everyone differently making it important that advice is taken when considering taking any action in response to the changes.

Now the legislation has now been published, we have a clearer understanding of how inheritance tax will be applied to pension funds. While lots of practical detail still requires clarification, it is sensible to review your circumstances to consider how the new rules may affect you and especially if you are approaching retirement or have a large pension fund that you had earmarked to be left to beneficiaries due to it being IHT free.

11th May 2026

-

Gavin Jones See profile

Gavin Jones See profile

What is changing?

From April 2027, IHT will be payable on the value of your pension fund immediately before death. We have previously covered the technical detail and you can read about this here: Autumn Budget 2025 – Pensions Breakdown – Old Mill

While the current rules remain in place until April 2027, it may be best not to disturb your current arrangements for dealing with your pension fund on death.

As we covered previously, for those who are likely to draw on their funds significantly to support their retirement income requirements, these changes are likely to have less impact.

Changing your plan

Since the existing rules were introduced in 2015, it has been tax efficient to leave pensions undrawn if possible, to maximise the IHT advantage. While there are some tax charges after your 75th birthday, they are typically less than the IHT payable on other assets in your estate.

After April 2027, this will reverse and post age 75 the tax on your pension will likely be significantly higher. Where benefits are transferred to an individual, any funds subsequently withdrawn will suffer Income Tax at the beneficiary’s own marginal rate of Income Tax.

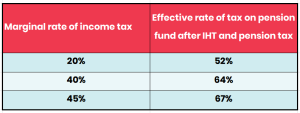

The table below shows the effective tax rate where death benefits are provided via a drawdown plan, having incurred IHT at 40% and Income Tax.

If you are over the age of 55 (rising to 57 from April 2028), you can start drawing on your pension fund, with a tax-free lump sum of usually 25% of the fund value (within limits) and any income received is simply taxed at your marginal rate of Income Tax.

For anyone who is a non-taxpayer or pays tax at the basic rate and, especially those over the age of 75, it may be beneficial to start drawing income ahead of the changes in April 2027 provided the pension income remains taxable at the basic rate. Even where this income is not required, it could potentially be free of IHT if gifted whereas leaving the funds to accumulate in the pension could mean they will become highly taxed if the estate is liable to IHT.

If you have reached the age of 75 and not yet drawn your tax-free cash sum, then it is likely to be sensible to take this before the changes in 2027. Whilst the lump sum may be liable to IHT at 40% in your estate, it will avoid additionally incurring pension charges as well, which would see an overall effective tax rate of 52% or more as shown in the table above. Your financial planner will be able to advise on the merits of doing this in your circumstances.

Pension nominations

All pensions and death benefit nominations should be reviewed in light of the new rules, especially for those who are married and have earmarked their pensions for anyone other than their surviving spouse.

If benefits are passed to anyone else, the fund will then be potentially subject to IHT and could be subject to an immediate tax charge. It is common for pension funds to be nominated for children, or grandchildren and it may be appropriate to review this.

For those with a spouse or civil partner, it is likely to become the default that they are nominated to avoid an IHT charge on the first to die as the inherited pension scheme will be covered by the spousal exemption.

Insurance

Unless action is taken, the inclusion of pensions in estates is very likely to result in an increase in Inheritance Tax and therefore leaving less of the estate to be inherited. Without action, the only winner will be HMRC.

One way to mitigate the impact of the changes, especially if your pension fund has been earmarked to pass down to the next generation is to use some of the pension income to cover the cost of an insurance policy.

Some of this income can be used to pay the premium cost on a Whole of Life (WOL) insurance plan that will pay out a guaranteed lump sum on your death.

The WOL can be written in trust so that the proceeds are paid to your beneficiaries directly and will not be in your estate.

There are things to consider, such as the tax treatment of the premiums going into trust, but if you are interested in finding out more, your Financial Planner can discuss your individual circumstances and advise on the suitability of this option.

Should I still make contributions to my pension?

While the changes are unwelcome, pensions remain an important tool in most people’s financial plan. While IHT on pensions has made their use as an estate planning vehicle much less attractive, they are still a tax efficient way to save for retirement income.

For those still working, pensions offer the prospect of high levels of tax relief which can make pension contributions very cost effective.

While the rules remain unchanged, you can currently pay up to the level of your earned income subject to a maximum of £60,000 into a pension each tax year. There is also the ability to carry forward unused pension allowances from previous years, which could potentially permit contributions to be paid of up to £240,000 and receive full tax relief worth up to £108,000.

Retaining personal allowances

There are instances when the level of tax relief can be as high as 60%.

When your income is greater than £100,000, your personal Income Tax allowance is reduced by £1 for every £2 above this limit until there’s no personal allowance at all once income is over £125,140. A pension contribution can help bring income back down below £100,000 to retain the personal Income Tax allowance.

As an example, someone with a total income of £125,140 could make a pension contribution of £20,112 which will have 20% tax relief added making a Gross contribution of £25,140. This would be just enough to reinstate in full their personal allowance so will get effective tax relief of 60%. That’s 40% tax relief on the £25,140 going into their pension and a further 20% by getting their personal allowance back.

Avoiding the High Income Child Benefit Charge

For those with younger children and a salary above £60,000 and in receipt of Child Benefit, there is the High Income Child Benefit (HICB) charge which starts to offset the benefit. The tax charge is at the rate of 1% of the benefit for every £200 over this threshold equalling the benefit once income reaches £80,000.

By making personal pension contributions, it is possible to effectively reduce your income for child benefit purposes and so reduce the charge. If your income is £80,000 in this tax year, there will be a tax charge of £2,337 to offset the child benefit. Making a net pension contribution of £16,000 (equivalent to Gross £20,000 with tax relief added), will remove the charge completely and result in effective tax relief of over 51%. That’s 40% tax relief on the Gross pension contribution of £20,000 and the remainder from removing the HICB.

This is, however, a complex area and dependent upon your level of income, there are set rules as to how much you can contribute during a tax year and obtain tax relief, so do be careful and seek advice before making a pension contribution.

Summary

There has long been an argument for a set of consistent rules for pension schemes to give people confidence to plan for the future. While some of the proposed changes are understandable from a tax point of view, the cliff-edge implementation in 2027 will have serious consequences for some who had planned under the existing rules.

The inclusion of pension funds within estates for IHT purposes is potentially very complex, and as a consequence, it also seems that the job of personal representatives will get more onerous with the need to deal with pension companies and arrange for them to settle tax liabilities.

It will be important for people to review their financial position to understand the impact of these changes on their own circumstances. They are a potential minefield, making it more important than ever for people to take advice on how best to navigate the changes to reduce the potential impact.

If you have family or friends with pensions who may be impacted by these changes, we have an enquiry service: the financial health check, which can give an initial indication of whether advice should be sought. You can find details of this service here financial healthcheck.

If you have any questions or would like to discuss your individual circumstances with an Old Mill financial expert, please do get in touch.