What do the changes to the R&D regime mean for your company?

Briefing – Research & Development (R&D) changes

You have probably seen a lot of coverage in the news and on social media regarding changes to R&D tax relief in recent years. If your company claims R&D tax relief already or is planning to make its first claim, you might be wondering how all these changes and new rules impact you.

Below, we have outlined the changes according to the year-end that the R&D claim relates to. Still, firstly, it is important to note that an additional information form (AIF) must be submitted to HMRC for all claims filed now, irrespective of the year-end. This form provides specific details to HMRC to enable them to assess the validity of the R&D claim more easily and consistently. This must be filed before the R&D claim is filed in the company’s tax return, otherwise the claim will be rejected.

It is also worth noting that in some circumstances it might be possible to minimise the impact that some of the changes may have on your company by changing the company’s year-end.

1st March 2025

-

Aisha Perrott See profile

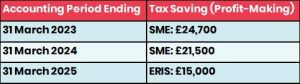

Accounting period ending on or before 31 March 2023

Applicable schemes

Small Medium Enterprise Scheme (SME)

R&D Expenditure Credit Scheme (RDEC)

Tax saving

Claims for these year-ends are prepared under the ‘old’ rules.

- SME: For profit-making companies, under the more generous SME scheme, this equates to an additional tax saving of 24.7%. Loss-making companies do not pay tax and receive a tax credit of up to 33.4% of their qualifying spend back.

- RDEC: If the company must instead claim under the less generous RDEC scheme, the net tax saving (or tax credit for loss-making companies) is approximately 10.5%.

Administration

The company has two years from the year-end to file a claim. This means that, for a 31 March 2023 year-end, the claim must be filed by 31 March 2025.

Accounting period ending on or after 1 April 2023 but beginning before 1 April 2024

Main changes

- The introduction of the new R&D intensive SME scheme, seeing a reduction in tax saving rate for the SME scheme but an increase for the RDEC scheme, and

- The introduction of the advanced notification requirement.

Applicable schemes

Small Medium Enterprise Scheme (SME)

R&D intensive SME scheme

R&D Expenditure Credit Scheme (RDEC)

Tax saving

- SME scheme: For profit making SME’s, the tax saving relating to expenditure incurred prior to 1 April 2023 is up to 24.7%. For expenditure incurred on or after 1 April 2023, the tax saving is between 16.34% – 21.5% depending on the company’s tax rate.

- For loss-making SME’s, for expenditure incurred before 1 April 2023, the tax credit is up to 33.4%. For post 1 April 2023 incurred expenditure, the tax credit is up to 18.6% if the company is not ‘R&D intensive’ and could therefore claim under the R&D Intensive SME regime.

- For expenditure incurred on or after 1 April 2023. If the company was loss-making and ‘R&D intensive’ (broadly meaning that at least 40% of the company’s expenditure is related to qualifying R&D expenditure), the company can claim relief at a higher rate under the R&D intensive SME scheme, resulting in a tax credit of up to circa 27%.

- RDEC: For expenditure incurred up to 1 April 2023, the net tax saving (or tax credit for loss making companies) equates to circa 10.5%. For expenditure incurred post 1 April 2023, the net tax saving equates to circa 15% for a company paying tax at 25%, and up to 16.2% based on a company paying tax at 19%.

Administration

There has been no change to the filing window, meaning the company has two years from the year-end to file a claim. For accounting periods beginning on or after 1 April 2023, an advanced notification form (ANF) may need to be filed within 6 months of the period end. See here for detailed guidance: Research & Development (R&D) rule change for Claims – Old Mill (om.uk) or get in touch with one of the team who would be happy to talk you through the rules.

Other

For accounting periods beginning on or after 1 April 2023, R&D in pure maths can also qualify for tax relief. In addition, for the same accounting period, data and cloud computing costs can form part of qualifying R&D expenditure.

Accounting period beginning on or after 1 April 2024

Main changes

- Firstly, the introduction of the new merged scheme replacing the previous SME and RDEC schemes applies to these periods. In terms of tax saving, this is bad news for those previously claiming under the SME scheme, but a welcome benefit for those previously claiming under RDEC.

- Changes to subcontracting and subsidising rules, providing welcomed clarity, and

- The introduction of the new Enhanced R&D Intensive Support Scheme (ERIS) (previously the R&D intensive SME scheme) including a reduction in the R&D intensity percentage.

Applicable schemes

The merged scheme

Enhanced R&D intensive support (ERIS) for loss-making SME’s that meet the R&D intensity test (previously R&D intensive SME scheme).

Tax saving

- Under the new merged scheme, the tax saving is 15% for companies paying tax at 25%, and 16.2% for companies paying tax at 19%, with a sliding scale between.

- For loss-making SME’s there is the option to claim under the ERIS scheme, meaning the tax credit could be up to 26.97%.

Note that the R&D-intensive SME threshold reduces to 30% in these periods which is a positive change for loss-making companies.

Administration

There have been no changes, meaning:

- the company has two years from the year-end to file a claim;.

- an advanced notification form (ANF) may need to be filed within 6 months of the period end. (See here for detailed guidance: Research & Development (R&D) rule change for Claims – Old Mill (om.uk) or get in touch with one of the team who would be happy to talk you through the rules.)

Overseas subcontracting restrictions:

New rules that prohibit companies from claiming costs relating to R&D sub-contracted abroad, except for a limited set of circumstances, come into effect.

Subsidised expenditure:

Where expenditure is subsidised, the claim no longer has to be done under a different (and less generous) scheme. For accounting periods beginning on or after 1 April 2024, companies can claim for all expenditure, whether subsidised or not.

Contracted out R&D:

Where the company is undertaking R&D as a sub-contractor, it is necessary to consider which company is undertaking the R&D to avoid a double claim. Under the new rules, consideration must be given to whether the customer or the company intended or contemplated the R&D. Contracts for provisions for goods or services are unlikely to amount to contracted-out R&D.

It is also worth noting that if the contractor is a non-UK company or government body, the company can still make a claim. This is because the contractor cannot, in this instance, make a claim.

Examples

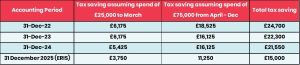

By way of an example, the following table shows the impact of the changes for two companies spending £100,000 on qualifying R&D a year under the SME scheme, the first with a March year-end, the second with a December year-end:

March year-end – SME scheme claim, profit-making, paying Corporation Tax at 25%, R&D spend £100,000

December year-end – SME scheme claim, profit-making, paying Corporation Tax at 25%, R&D spend £100,000

For both companies above, compared with their 2023 year-end, the company receives a tax saving of nearly £10,000 less for the 2025 year-end.

Get in touch

If you would like to discuss how the various changes impact your company in more detail, contact one of the Research & Development Team or click here…