Long-term goals, short-term emotions

There is always a tension between the sensible, well-thought-out long-term financial goals that investors set in place – often with the help of their financial adviser and the emotions that they are likely to experience in the moment, as markets respond to new information and portfolio values are impacted.

6th October 2023

-

Gavin Jones See profile

Gavin Jones See profile

This tension can sometimes be most acutely felt by both the investor and their adviser in the early stages of their relationship when a portfolio either goes down or sideways in the first year or so. However, as much as one would like to start the investing experience with markets rising, this is not always the reality as newer investors have recently experienced.

From the investor’s point of view, an aversion to loss, the feeling of loss of control and disappointment at seeing hard earned money falling in value can feel unsettling. From the adviser’s perspective, it can also be a challenging time, knowing that however sound the financial plan, however sensible the portfolio asset allocation and however much time they have spent providing insight into the up and down journey a client will experience, emotions often trump logic when a portfolio falls in value.

At such times, it can be useful to keep in mind the following:

- Firstly, cash is the only investment that avoids losses, but only before inflation, and its low, long-term, after-inflation returns are unlikely to allow most investors to meet their financial goals, hence the need to add equities and bonds into the asset allocation. Do not be fooled by today’s high cash rates relative to recent years as they are something of an illusion for long-term investors and are not a substitute for a sensibly structured long-term portfolio designed to meet long-term goals. Do not be tempted by them.

- Secondly, it is the very uncertainty of the shorter-term outcomes of equities and bonds that delivers the longer-term, above-inflation returns that most investors need to meet their goals. The longer-term expected returns from a sensibly structured investment portfolio are far higher than those of cash.

- Finally, falls in portfolio values are not losses and have every likelihood of recovering in time. Patience allows the longer-term expected returns to be realised. Avoid emotionally driven investment decisions that might impact these longer returns.

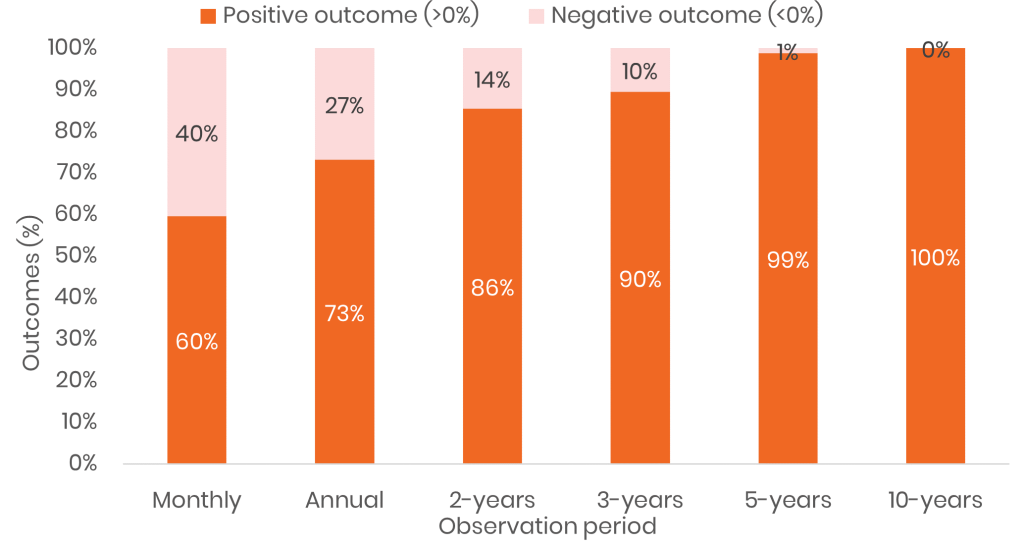

The chart below (Figure 1) provides an insight into the proportion of times that investors in a medium risk portfolio have suffered falls in value over different time horizons. Whilst falls in purchasing power (i.e., after inflation) over two years are not uncommon, over five years – which is only a fraction of the time horizon of most investors – the chances of a fall decreases materially, based on data over the 34-year period reviewed.

Figure 1: The likelihood of gains in purchasing power (July 1989 to August 2023)

Data source: Morningstar Direct ©. All rights reserved. Data: global balanced portfolio from 07-1989 to 08-2023[1]

Looking back on a monthly basis over the last 34 years, you would have observed a positive return 60% of the time, and 40% of the time the portfolio will have fallen in value. If you look once a year, the number of negative experiences reduced to 27% of the time and looking at rolling 10-year periods, the investment outcome will have always been positive.

If you are a new investor, keep faith in your portfolio and remain invested for the long term because that is what is required to give yourself the best chance of achieving a positive investment outcome to meet your long-term goals. If you have been investing for some time and been through one or more cycles of market falls and recoveries, hopefully the tension between longer-term goals and short-term emotions will be greatly tempered.

As Charlie Munger, Vice Chairman of Berkshire Hathaway once said: ‘The big money is…in the waiting’.

[1] Global equity model portfolio with tilts to value and smaller companies and global commercial property, balanced by higher-quality, shorter-dated bonds (full details of market indices used available on request). No costs of any kind have been deducted. For illustration purposes only.