Market commentary

Last week, the latest release of the UK Consumer Price Indices showed the rate staying at the same rate in May as it was in April at 8.7%. The core inflation rate, which strips out the impact of Energy and Food, rose to 7.1% prompting concerns that inflation could become persistent. This caused the Bank of England to raise the Base Rate by 0.5% to 5% (most economist expected an increase of 0.25%) and indicated that there are more increases to come.

7th July 2023

-

Gavin Jones See profile

Gavin Jones See profile

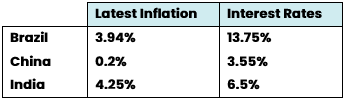

- Latest inflation: 8.7%

- Interest rates: 5%

Inflation in the UK appears to be more persistent. The significant increases in inflation have prompted higher wage demands, which, in turn, encourage companies to sustain price increases. Consequently, the Bank of England (BoE) is expected to continue raising rates in the short term. The Prime Minister set out one of his key five priorities in 2023 which was to halve inflation and this was expected to happen quite easily as the impact of rising energy prices in 2022 were considered. However, the figures are proving stronger than expected.

Higher interest rates continued to weigh on bank lending in May 2023, particularly in the housing market. This is only likely to get worse as the Bank of England raises rates even higher. Although mortgage lending remained steady in May, there has been a surge in mortgage rates, which have climbed above 6% for the first time since 2007. Mortgage lending and housing activity are expected to slow down because of this going forward and economists are expecting for house prices to fall this year.

- Latest inflation: 6.1%

- Interest rates: 4%

The latest inflation figures for the eurozone exceed 6% and are also coming down more slowly than expected, with services inflation being a significant factor and food and core goods continuing to grow strongly.

There are some signs that the rate hikes implemented by the European Central Bank (ECB) are beginning to impact economic activity and cool down inflationary pressures. The German economy has contracted for two consecutive quarters, and eurozone bank lending has stagnated for six months. If inflation continues to moderate in the coming months, the ECB hiking cycle may come to a halt by autumn.

- Latest inflation: 4%

- Interest rates: 5 to 5.25%

US Consumer Price Index inflation, currently 4.0% for May, has significantly decreased from the 9.1% peak observed in Q2 2022, but it is still some way from the Federal Reserve’s long-term target of 2%.

Interest rates paused in June at 5 to 5.25%, (the US gives a range of interest rates rather than a single figure) 0.5% below the US Federal Reserve’s expected peak, with 5.5-5.75% being the median forecast for 2023 in the latest Summary of Economic Projections (you may have heard the term ‘dot plot’ on the news).

While the Fed hasn’t indicated how long they may pause rates, waiting to see how economic indicators respond but market bond prices are expecting that the end of this rate hike cycle is in sight. Bond markets are now pricing in peak interest rate in autumn and rate cuts by the end of this year, reflecting the traditional recession playbook where central banks cut rates on signs of economic and financial damages. However, this is not the first time that the market has misjudged the Fed’s intentions to ease interest rates and should inflation prove persistent, this could mean rates could stay higher for longer.

In contrast to much of the world, the latest round of data from China largely disappointed expectations, with many areas of economic activity reversing in annual terms. Retail sales were higher compared to last year’s lockdown period, but the reopening boost has been disappointing relative to expectations. The post-COVID rebound quickly fizzled out as it appears Chinese consumers didn’t have hugely increased savings rates (unlike in developed markets).

Given the weakening economic data, some form of increased economic stimulus from Beijing is expected and interest rate cuts are widely expected.

Other emerging countries have been similar to developed countries with high inflation and rising interest rates to balance this.

Higher for longer inflation, in the UK in particular, has impacted the expected path of interest rates. At the start of the year, predictions for the UK base rate showed a peak at around 4.75% and at the end of May a peak of 5.5% was expected.

After the inflation figures in June, those expectations now lie at 6.25%. That’s effectively an extra 0.75% interest rate rises priced in. Remember that the base rate itself was no higher than 0.75% from February 2009 until May 2022.

The world is having to learn to live with higher interest rates but one of the impacts of this will be higher yields which will benefit you as an investor.

Please speak to your financial planner if you want to discuss your portfolio.