Wealth Management Insight - Autumn Statement special

The Chancellor of the Exchequer, Jeremy Hunt delivered the 2022 Autumn Statement on Thursday 17 November.

Here we provide some context about the Autumn Statement and details of actions that you may wish to consider.

24th November 2022

Autumn Statement

Given Jeremy Hunt is the fourth chancellor in less than twelve months and with less than two months since the Kwasi Kwarteng / Liz Truss ‘growth plan,’ there was a degree of anticipation. The backdrop to the statement was war in Ukraine, increasing energy prices and cost-of-living challenges. There had been significant speculation of the need for ‘tax rises for all’ and a return to austerity for spending cuts to fill a £50 billion black hole in public finances.

Stock markets and government gilts reacted badly to the unfunded tax cuts in the growth plan in September so the absence of reaction to the autumn statement, with Sterling, stock markets and government gilts seeing little movement, was seen as a positive sign.

With one eye on a general election which will be by the beginning of 2025 at the latest, the statement was carefully managed, with a focus on ‘stealth’ taxes and the further freezing of tax bands for basic and higher rate income tax, as well as for National Insurance and Inheritance Tax. For the last few years with Rishi Sunak as Chancellor and now Prime Minister, stealth taxes have been the way forward. You can see why with no headline increase in the tax rate it is much less politically sensitive for the majority of the general public.

But stealth taxes are not new. There has been talk about the 60% rate of tax in the media this year which occurs for those with income between £100,000 and £125,140 where income tax is 40% but the personal allowance is taken away which means an effective rate of tax of 60%. This was in fact introduced by Alistair Darling in 2009 and the threshold has remained at £100,000 since then. It is estimated that the number of people falling into this income band may have tripled over the subsequent years.

There were other measures aimed at higher earners with a reduction in the additional 45% income tax threshold to £125,140 from £150,000 along with some changes to tax allowances for investments – a reduction in the capital gains tax and dividend tax free allowances from next April.

To help with the rising cost of living, the triple lock for pensioners and state benefits in general will all increase with inflation meaning a 10.1% increase in April 2023.

Spending cuts have largely been scheduled for several years’ time, to allow for changes in some of the external factors to potentially change – the war in Ukraine, a slowing of inflation and the result of the next UK General election.

Fortunately, there have been no immediate tax changes and therefore normal tax year end planning at the beginning of next year will be even more important ahead of increasing levels of taxation from next April.

Actions to consider

We have asked our experts to comment on the statement and specifically any actions they think are appropriate and also their thoughts on how finances can generally be structured tax efficiently. This includes both actions you can take now to maximise your allowances and also actions to mitigate the impact of some of the changes we expect to see in the next few years. We have included planning for all ages, and whilst some of the points may not be relevant for you, they may be of interest to help younger family members so please feel free to share this with them.

The burden of taxation is increasing and in the face of a cost-of-living crisis, any tax saved we are sure will be very welcomed. The list is not exhaustive, and we would urge you take advice before acting on any of the points raised.

Individuals

-

Income taxes

With stealth increases to income tax by freezing the level of personal allowance, the basic and higher rate bands as well as reducing the additional rate threshold we look at some specific areas you might want to consider, as well as utilising any available allowances. Click here for the full article.

-

Investment allowances

Changing allowances, especially for Dividends and Capital Gains next year and the year after, mean that making full use of the investment allowances available to you will become increasingly important and valuable. Click here to read the full article.

-

Dividends

The 1.25% increase to dividend rates from April 2022 was initially driven by the health & social care levy in the same way as the increase for national insurance contributions. While the increase in national insurance was removed on 6 November, the dividend increase remains in place for individuals and trusts.

With the Dividend Allowance reducing from £2,000 to £1,000 then to £500, it becomes more of a nominal allowance just to cover those with small shareholdings. One of the consequences of this will be bringing more people back into Self-Assessment and having to complete a tax return.

HMRC do say that if you aren’t currently on Self-Assessment and the dividends you receive each year are below £10,000 you can opt to have your tax code adjusted rather than complete a tax return. However, this can be quite fiddly and you need to keep a careful eye that the tax code is accurate.

If you would prefer to have a tax return completed for you and have a professional oversee that you are being taxed correctly then we can help with that.

-

Capital Gains Tax (CGT)

A significant change was announced to CGT with a reduction in the annual exempt amount from £12,300 to £6,000 next tax year and £3,000 the year after.

This recommendation was made by the Office of Tax Simplification several years ago, along with the recommendation to align CGT rates of tax to be the same as income tax. So far, the rate of tax has not been changed.

With non-property gains taxed at half the equivalent Income Tax rate at present, it is still good planning to have assets that can create gains. Additional rate taxpayers will pay 45% tax on income but only 20% on gains.

It may be appropriate to review your assets now to consider crystallising gains in assets that have gone up in value or to ‘capture’ losses in assets that have fallen. Losses can then be offset against gains in the future to reduce tax paid.

Assets can also be transferred between spouses before sale to ensure that both can use their allowance, however advice should always be taken if you are thinking about doing this.

-

Gifts and Inheritance Tax (IHT)

There were no new changes to IHT in the autumn statement, other than the £325,000 nil rate band and up to £175,000 residence nil rate band remaining frozen until 2028.

With a Government that may need to raise additional funds in the next few years here is a timely reminder of the key exemptions that are currently available which you may like to take advantage of. Click here to read the full article.

Property

-

Property and CGT

With changes to mortgage interest tax relief for investment properties over the last few years and a raft of new legislation it has prompted some property investors to consider selling up. With significant Capital Gains Tax (CGT) built up for these properties, the tax implications of selling can make this a difficult decision.

With the annual exempt amount falling, if you are thinking of selling trying to do it in the remainder of this tax year may save some tax. A husband and wife who own a rental property could have £24,600 (2 x £12,300) of exempt capital gains in this tax year but this will fall to £12,000 after April. If both are higher rate taxpayers and will incur the 28% residential property tax the saving, provided the sale completes in this tax year before 6 April 2023 will be £3,528 (£12,600 x 28%).

Remember that the disposal of a UK residential property that gives rise to a tax liability needs to be reported to HMRC (via a property return) and the tax due paid within 60 days of completion. This could be a sale to a third party but a gift to a family member or transfer to trust are also chargeable events where tax may be due.

This separate property return has to be completed even if you already complete a Self-Assessment tax return.

We have produced a handy guide to what you need to consider when selling an investment property which you can download here: Property Returns & Capital Gains Tax.

-

Stamp Duty Land Tax (SDLT)

At the September ‘mini budget’ the Stamp Duty Land Tax nil rate band was increased from £125,000 to £250,000 and from £300,000 to £425,000 for first time buyers. These were some of the only measures not to be immediately rolled back once Jeremy Hunt became Chancellor. It was announced at the Autumn Statement that these increases will only be temporary and will revert back to the previous level from 1 April 2025.

-

Structure & taxation review

While some investors are looking to sell up, many more continue to hold investment properties as part of their overall wealth. With changes to taxation, interest rates and legislation over the last few years it may be a good time to review your property. Our experts can consider your overall structure, tax efficiency and strategy for both residential and commercial property to see if any changes can be made to save tax, reduce administration and consider the investments in light of your future plans.

Speak to your usual Old Mill contact if you want to know more.

Trusts

-

Trust taxation

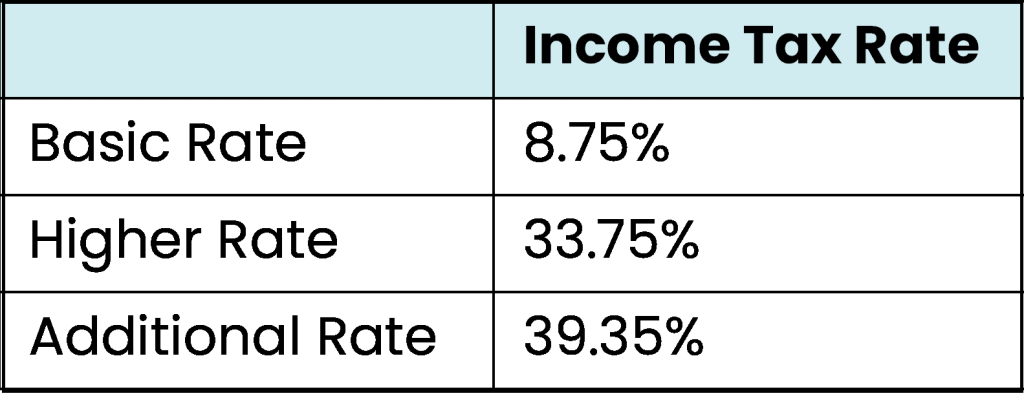

With the roll back of tax cuts in September’s ‘mini budget,’ trust tax rates remain at 20% standard rate band and 45% above this for income and 8.75% and 39.35% for dividend income received by trustees.

With the trustees’ capital gains annual exempt amount being half the individual rate then this will fall to £3,000 in April 2023 and £1,500 the year after. Trustees should consider whether gains need to be incurred in this tax year to maximise the use of their allowance and whether any changes need to be made to assets in the trusts or the products used. With the tax differential between income at a maximum of 45% and gains at a maximum of 20%, it may not be obvious if changes are needed without considering the long-term plans for the trust and the potential tax charges on trustees or the potential beneficiaries in the future.

Depending on the terms of the trust and assets held it may be possible to use tax structures like single premium investment bonds to control the timing of tax paid by the trustees.

-

Trust reporting

As part of European wide anti-money laundering regulations, HMRC now require most Trusts to be registered on their online Trust Registration Service (TRS). Previously, only Trusts that had to pay tax had to register but from the beginning of September the requirement now extends to most Trusts, regardless of their tax status.

If you have received a reporting request but have not completed the registration do get in touch, there are fines for those who do not comply.

Business owners / Businesses

-

Planning

With the rate of Corporation Tax going up to 25% for companies with over £250,000 in profit next year, as well as changes to Income Tax and National Insurance, businesses and their owners should be reviewing their remuneration and benefits planning.

In addition to the increases in Corporation Tax, the Dividend Allowance reducing over the next two years will also result in an increase in tax. It is therefore important to understand the implications both of these have on profit extraction from a business.

-

Pension contributions

Increases in the rate of Corporation Tax will increase the attractiveness of making employer pension contributions to extract money from a company. As long as any contributions meet the ‘wholly and exclusively’ for the purpose of the business rules which are reasonably wide ranging they will benefit from Corporation Tax relief saving on employee and employer National Insurance, with no benefit in kind charge.

-

Salary Exchange

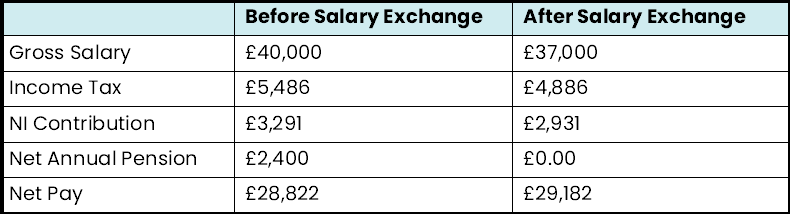

Progressive employers could start to consider their employees tax positions when agreeing benefit package increases. For employees who may see a change to their tax band or impacts on child benefit for instance they may like to consider increasing their pension contributions using a salary sacrifice arrangement which will have an added bonus of a national insurance saving both for the employee and employer. Taking an example of an employee with a gross salary of £40,000 and employer and employee pension contributions of £250 per month. After the salary exchange the employee gives up £3,000 of salary for the employer to make a pension contribution of £3,000. In both cases the employee will receive £6,000 in their pension.

The net pay for the employee is increased by using salary exchange:

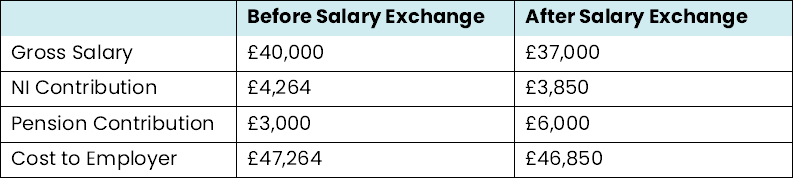

There is also a benefit for the employer, which they can keep, or share some or all of the saving with the employee:

For more senior employees there could be wider access to other salary exchange arrangements e.g., private healthcare or electric cars etc.

If you wish to discuss salary exchange in your business, then speak to your usual Old Mill contact in the first instance, as you will need advice.

If you would like to discuss your individual circumstances, please contact your Old Mill financial planner or contact us by clicking here.